Advertisement

- United States

- /

- Diversified Financial

- /

- NYSE:CODI

Could Compass Diversified's (CODI) Consistent Payouts Reflect a Mature Capital Allocation Strategy Amid Rare Earth Uncertainty?

Reviewed by Sasha Jovanovic

- On October 2, 2025, Compass Diversified announced that its Board of Directors declared quarterly cash distributions on all three of its preferred share series, with payments scheduled for October 30, 2025, to holders of record as of October 15, 2025.

- This announcement comes as investor attention intensifies around Compass Diversified’s subsidiary, Arnold Magnetic Technologies, following recent Chinese export controls on critical rare earth minerals.

- We'll assess how increased focus on rare-earth supply alternatives could influence Compass Diversified's investment thesis going forward.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Compass Diversified Investment Narrative Recap

To own Compass Diversified, investors need to believe in the company’s ability to capitalize on supply chain realignment and specialty industrial demand, while managing ongoing governance issues. The recent preferred share distributions reflect ongoing capital discipline, but do not directly address the most important short-term catalyst, a potential earnings boost for subsidiary Arnold Magnetic Technologies following Chinese rare-earth export controls. The biggest risk remains unresolved: financial irregularities and restatements at Lugano Holding, which could impact CODI’s credit, access to capital, and operational stability, regardless of broader industry trends.

Among recent announcements, the ongoing forbearance agreements and restatement of financials tied to Lugano stand out. These issues weigh more heavily on near-term prospects than the subsidiary tailwinds from rare-earth disruptions. Until the company resolves its accounting concerns and lender negotiations, investor focus will likely remain on these internal challenges, regardless of portfolio momentum elsewhere. In contrast, investors should be aware that restated financials and lender forbearance agreements may limit CODI’s...

Read the full narrative on Compass Diversified (it's free!)

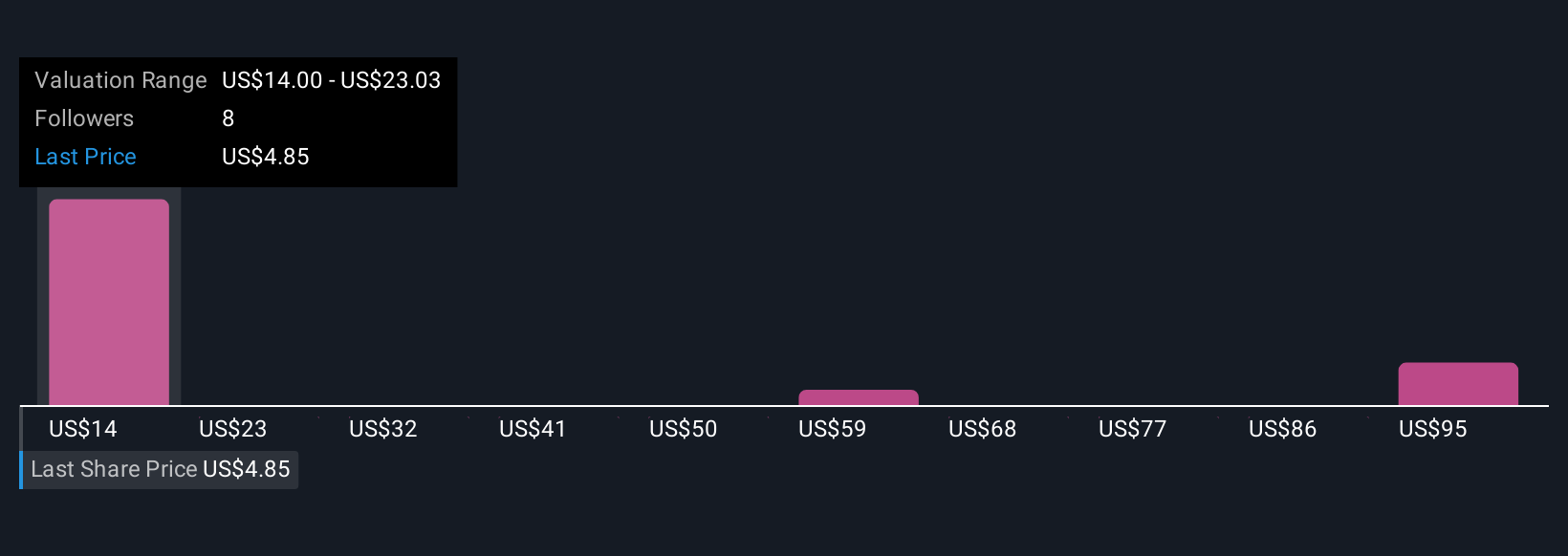

Compass Diversified's narrative projects $2.9 billion revenue and $282.6 million earnings by 2028. This requires 10.0% yearly revenue growth and an earnings increase of $377.3 million from -$94.7 million today.

Uncover how Compass Diversified's forecasts yield a $16.00 fair value, a 92% upside to its current price.

Exploring Other Perspectives

Four Simply Wall St Community estimates place CODI’s fair value between US$16 and US$104.25, reflecting substantial disagreement. With accounting and credit risks still front of mind, consider these varied viewpoints as you assess CODI’s future direction.

Explore 4 other fair value estimates on Compass Diversified - why the stock might be worth just $16.00!

Build Your Own Compass Diversified Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Compass Diversified research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Compass Diversified research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Compass Diversified's overall financial health at a glance.

Curious About Other Options?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Find companies with promising cash flow potential yet trading below their fair value.

- The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CODI

Compass Diversified

A private equity firm specializing in add on acquisitions, buyouts, industry consolidation, recapitalization, late stage, and middle market investments.

Good value with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2550.7% undervalued

116 followersusers have followed this narrative

0 commentsusers have commented on this narrative

25 likesusers have liked this narrative

BL

BlackGoat on IREN ·

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value:US$71.4846.5% undervalued

218 followersusers have followed this narrative

8 commentsusers have commented on this narrative

33 likesusers have liked this narrative

HE

HedgeY on Arm Holdings ·

The Architecture Layer of AI Computing - But Priced Like the Future Already Arrived?

Fair Value:US$43043.8% undervalued

22 followersusers have followed this narrative

1 commentusers have commented on this narrative

6 likesusers have liked this narrative

HI

Hidden_Rock_Capital on Fiserv ·

Temporary "perfect storm" leads to opportunity to buy financial services leader for less than 5x long-term earnings

Fair Value:US$119.9954.9% undervalued

30 followersusers have followed this narrative

1 commentusers have commented on this narrative

10 likesusers have liked this narrative

Recently Updated Narratives

JO

John_Eric on Meta Platforms ·

META: The Tide Just Went Out. Let's See Who's Dressed.

Fair Value:US$778.9330.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

John_Eric on Microsoft ·

Microsoft (MSFT): The AI Bull Case Everyone Sees, Trading at a Multiple Nobody's Willing to Pay

Fair Value:US$60024.8% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TR

TripleS on Dong A Eltek ·

Dong-A Eltek (088130 on the KOSDAQ) trades at ₩4,325 and owns about ₩17,780 per share of assets

Fair Value:₩6.31k31.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28030.3% undervalued

217 followersusers have followed this narrative

9 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.917.4% overvalued

101 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6511.3% undervalued

75 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

GR

greg_xasak on Fiserv ·

As someone who has dealt directly with them as a CTO for a credit union, I have 8 years of horror stories about doing business with them. If there was any other competitor than could deliver 80% of Fiserv services, there would be a mad rush to migrate to them. They should thank their lucky stars they are a near monopoly. this industry is so ripe for a well funded competitor. Their integration of technology is awful, their ability to fix their own implementation screwups is sadly tragic. Sometimes they just silently kill support tickets without resolution and you never find out until you do a follow up inquiry. Why, because sometimes no one you are dealing with knows how to fix it and knows no one to ask for help. They can not meet their own implementation deadlines and sometimes there is no one on a technical team dealing with you that has any banking or credit union experience. The is an industry insider phrase when you meet other Fiserv customers called being "Fiserved". It means telling others of your worst stories of dealing with them. Ask around, all CTO's have some doozies.

1

|0

BL

Blegells on Terra Balcanica Resources ·

⏫42X THE AVERAGE DAILY TRADING VOLUME TODAY, JULY 28 🐂🐂🐂 FORTY-TWO!

1

|0