- United States

- /

- Mortgage REITs

- /

- NYSE:BRMK

Is Now The Time To Put Broadmark Realty Capital (NYSE:BRMK) On Your Watchlist?

Like a puppy chasing its tail, some new investors often chase 'the next big thing', even if that means buying 'story stocks' without revenue, let alone profit. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses.

In the age of tech-stock blue-sky investing, my choice may seem old fashioned; I still prefer profitable companies like Broadmark Realty Capital (NYSE:BRMK). Now, I'm not saying that the stock is necessarily undervalued today; but I can't shake an appreciation for the profitability of the business itself. Conversely, a loss-making company is yet to prove itself with profit, and eventually the sweet milk of external capital may run sour.

See our latest analysis for Broadmark Realty Capital

Broadmark Realty Capital's Improving Profits

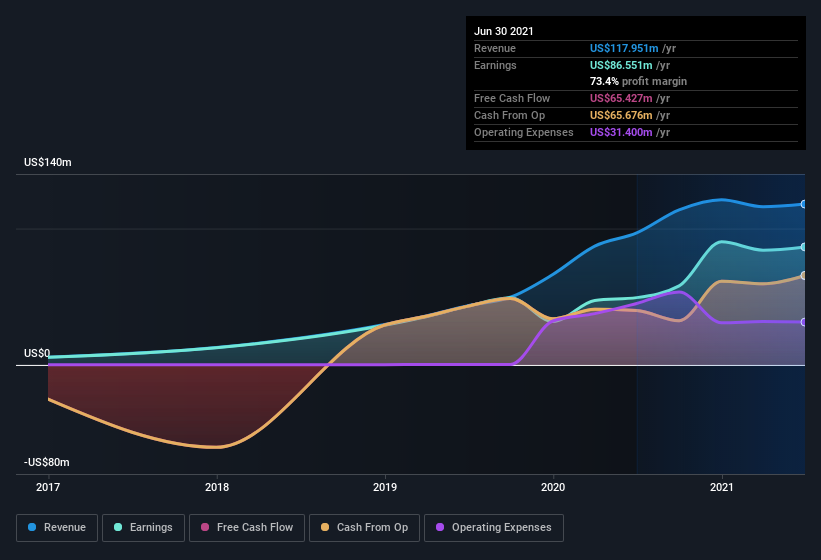

Even with very modest growth rates, a company will usually do well if it improves earnings per share (EPS) year after year. So it's no surprise that some investors are more inclined to invest in profitable businesses. Like a firecracker arcing through the night sky, Broadmark Realty Capital's EPS shot from US$0.37 to US$0.65, over the last year. You don't see 75% year-on-year growth like that, very often.

I like to take a look at earnings before interest and (EBIT) tax margins, as well as revenue growth, to get another take on the quality of the company's growth. I note that Broadmark Realty Capital's revenue from operations was lower than its revenue in the last twelve months, so that could distort my analysis of its margins. While we note Broadmark Realty Capital's EBIT margins were flat over the last year, revenue grew by a solid 22% to US$118m. That's progress.

In the chart below, you can see how the company has grown earnings, and revenue, over time. To see the actual numbers, click on the chart.

Fortunately, we've got access to analyst forecasts of Broadmark Realty Capital's future profits. You can do your own forecasts without looking, or you can take a peek at what the professionals are predicting.

Are Broadmark Realty Capital Insiders Aligned With All Shareholders?

It makes me feel more secure owning shares in a company if insiders also own shares, thusly more closely aligning our interests. As a result, I'm encouraged by the fact that insiders own Broadmark Realty Capital shares worth a considerable sum. Indeed, they hold US$45m worth of its stock. That's a lot of money, and no small incentive to work hard. Despite being just 3.3% of the company, the value of that investment is enough to show insiders have plenty riding on the venture.

It's good to see that insiders are invested in the company, but are remuneration levels reasonable? Well, based on the CEO pay, I'd say they are indeed. I discovered that the median total compensation for the CEOs of companies like Broadmark Realty Capital with market caps between US$1.0b and US$3.2b is about US$3.5m.

The CEO of Broadmark Realty Capital only received US$1.2m in total compensation for the year ending . That's clearly well below average, so at a glance, that arrangement seems generous to shareholders, and points to a modest remuneration culture. While the level of CEO compensation isn't a huge factor in my view of the company, modest remuneration is a positive, because it suggests that the board keeps shareholder interests in mind. It can also be a sign of a culture of integrity, in a broader sense.

Is Broadmark Realty Capital Worth Keeping An Eye On?

Broadmark Realty Capital's earnings per share have taken off like a rocket aimed right at the moon. The sweetener is that insiders have a mountain of stock, and the CEO remuneration is quite reasonable. The strong EPS improvement suggests the businesses is humming along. Broadmark Realty Capital certainly ticks a few of my boxes, so I think it's probably well worth further consideration. You still need to take note of risks, for example - Broadmark Realty Capital has 1 warning sign we think you should be aware of.

Of course, you can do well (sometimes) buying stocks that are not growing earnings and do not have insiders buying shares. But as a growth investor I always like to check out companies that do have those features. You can access a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if Broadmark Realty Capital might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NYSE:BRMK

Broadmark Realty Capital

Broadmark Realty Capital Inc. operates as a commercial real estate finance company in the United States.

High growth potential with adequate balance sheet.

Similar Companies

Market Insights

Community Narratives