Advertisement

- United States

- /

- Consumer Finance

- /

- NYSE:AXP

Assessing American Express (AXP) Valuation After Recent Dip and Strong Multi-Year Returns

Simply Wall St

Reviewed by Simply Wall St

American Express (AXP) shares have been relatively steady over the past week, while investors consider its consistent revenue and net income growth. With its latest quarterly results already digested, the stock’s momentum now depends on broader market sentiment and spending trends.

See our latest analysis for American Express.

The share price of American Express has cooled off from recent highs, dipping nearly 8% over the last week as investors weigh up the impact of volatile consumer spending and shifting market sentiment. Still, the company’s strong year-to-date share price return of 14.15%, along with an impressive 20.58% total shareholder return over the past twelve months and 128.75% total return over three years, shows that momentum remains firmly on its side.

If you’re in the mood to broaden your search beyond the usual names, discover fast growing stocks with high insider ownership for other fast-moving companies with compelling owner alignment.

But with shares now trading just below analyst targets and robust growth already reflected in its recent results, the real question is whether American Express is trading at a bargain or if the market has already accounted for future gains.

Most Popular Narrative: 2.9% Undervalued

American Express closed at $340.66, sitting modestly below the prevailing fair value of $350.87 set by the most popular analyst narrative. The latest consensus reflects rising expectations for persistent revenue gains, but only selective assumptions justify this higher price point.

Double-digit international growth, ongoing investments in global product innovation, and expanding merchant acceptance tap into the expanding global middle class and increased digital payment adoption. These factors are expected to raise transaction volumes and support both top-line growth and long-term earnings diversification.

Curious what bold financial assumptions could propel American Express beyond its current price? The narrative’s fair value rests on a forecast of top-tier international growth, stable profit margins, and a future earnings ratio that turns heads on Wall Street. Uncover the real numbers that drive this rare valuation and discover which assumptions make analysts believe there’s still upside.

Result: Fair Value of $350.87 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, intensifying competition in premium cards and younger consumers favoring alternative payment methods could dampen American Express’s growth story from this point forward.

Find out about the key risks to this American Express narrative.

Another View: What Do the Numbers Say?

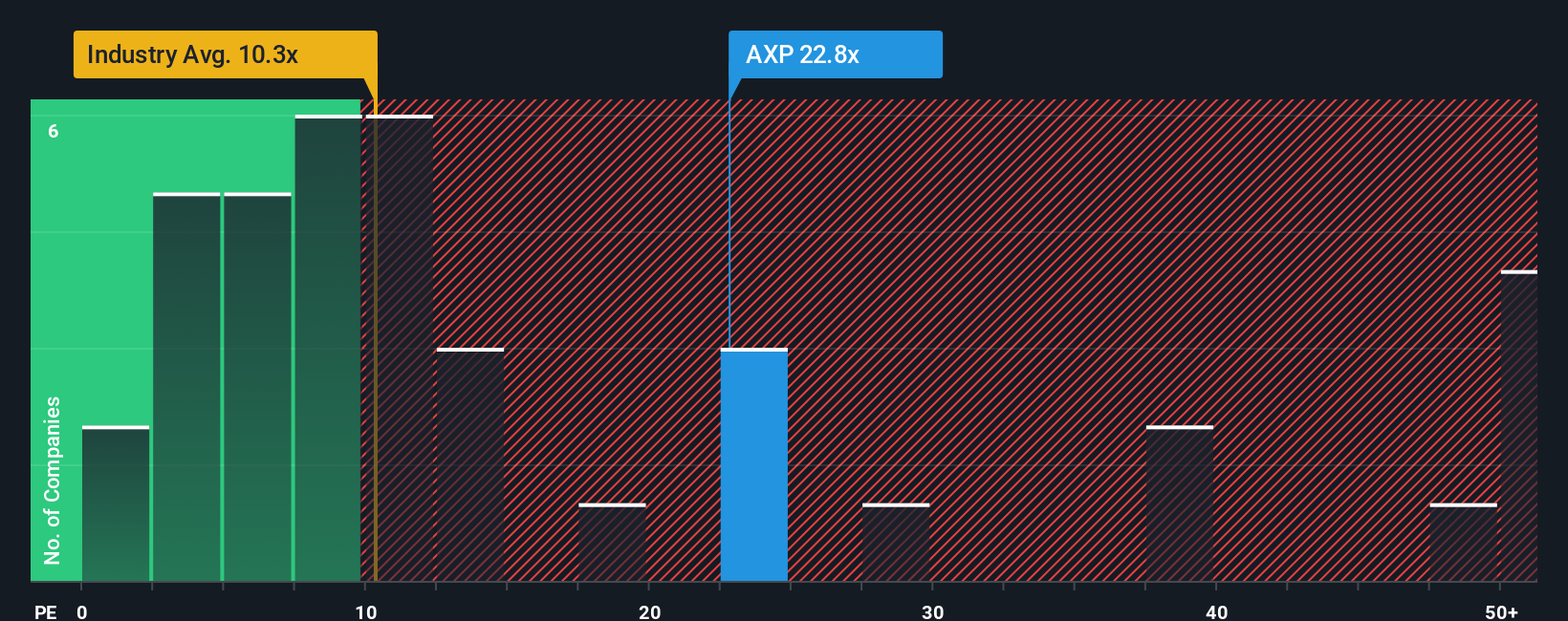

Looking at valuation through the lens of the price-to-earnings ratio, American Express trades at 22.5x, which is noticeably higher than the US Consumer Finance sector’s average of 9.9x and its fair ratio of 19.8x. This gap signals the market is pricing in notable optimism, but does it also raise the bar for future expectations?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own American Express Narrative

If you have a different take on American Express or want to put your own perspective to the test, you can craft your own narrative in just a few minutes. Do it your way

A great starting point for your American Express research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Opportunities?

Don’t let the best opportunities pass you by. Level up your strategy with investment ideas designed to help you uncover hidden value, future trends, and reliable income streams.

- Access tomorrow’s industry leaders with these 27 AI penny stocks. Be part of the AI-driven transformation shaping global markets.

- Find companies offering steady, above-average payouts by exploring these 18 dividend stocks with yields > 3%. This could boost your portfolio’s income starting now.

- Tap into the next wave of growth stories by checking out these 905 undervalued stocks based on cash flows and spot businesses that the market may be underestimating.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:AXP

American Express

Operates as integrated payments company in the United States, Europe, the Middle East and Africa, the Asia Pacific, Australia, New Zealand, Latin America, Canada, the Caribbean, and Internationally.

Excellent balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor