- United States

- /

- Diversified Financial

- /

- NasdaqGS:PYPL

The Bull Case for PayPal (PYPL) Could Change Following Exclusive BigCommerce Payments Launch Announcement

Reviewed by Sasha Jovanovic

- On October 20, Commerce announced a new embedded payment processing solution, BigCommerce Payments, powered by PayPal and available exclusively to BigCommerce merchants in the US beginning in 2026, with plans for international rollout.

- This co-branded integration enhances merchant access to advanced payment tools, including buy now, pay later with PayPal's Pay Later, and streamlines management through the BigCommerce Control Panel, further cementing the partnership's progress in digital commerce enablement.

- We'll examine how PayPal's deeper integration with BigCommerce could influence its investment narrative and future merchant engagement outlook.

These 16 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

PayPal Holdings Investment Narrative Recap

The big picture for PayPal shareholders centers on its evolution into a full-service commerce platform, leveraging embedded payments, data, and value-added services to deepen merchant and consumer relationships. While the exclusive BigCommerce Payments launch reinforces this strategic direction, it is unlikely to substantially alter the near-term focus, which remains on improving transaction margins and maintaining a competitive edge against rivals like Apple Pay and Amazon Pay. The most pressing risk is still competitive intensity in core checkout markets, which could impact revenue growth and merchant retention. Of PayPal’s recent announcements, the launch of PayPal Ads Manager on October 7 stands out as especially relevant. This solution expands PayPal’s platform utility for merchants, aligning with the broader push seen in the BigCommerce deal to embed PayPal deeper into core e-commerce workflows, potentially supporting future margin and engagement catalysts. But before getting too comfortable with the growth story, investors should note ongoing risks in key markets, especially as...

Read the full narrative on PayPal Holdings (it's free!)

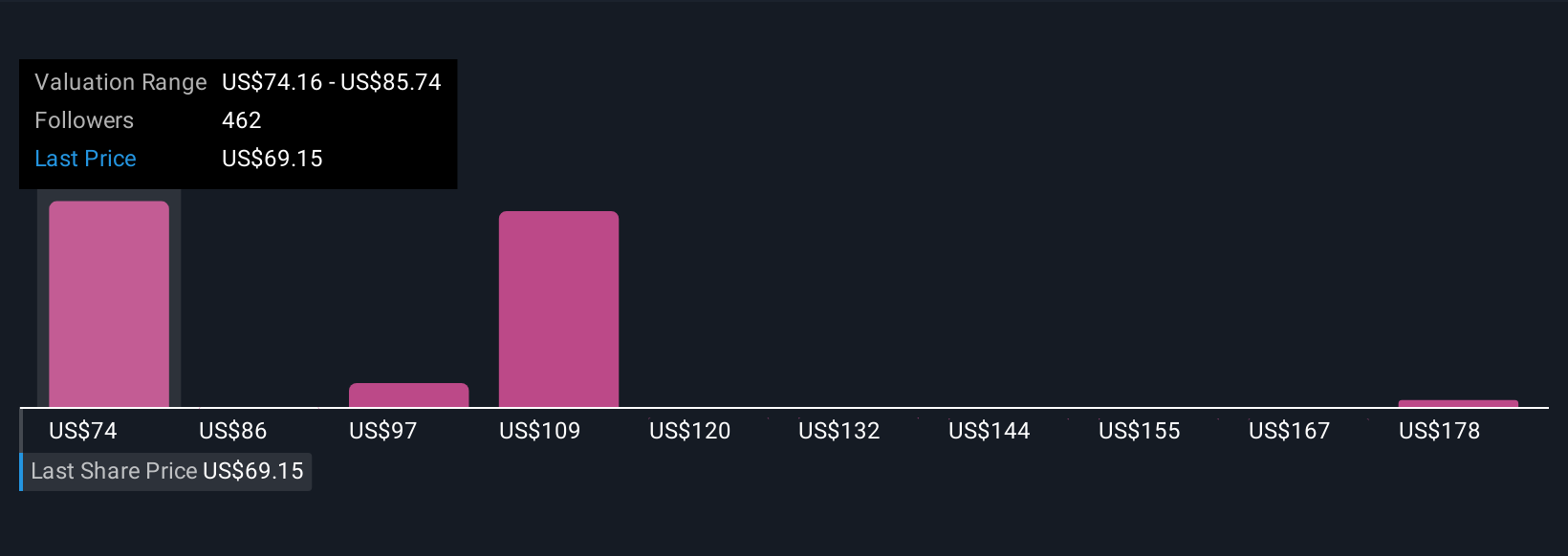

PayPal Holdings' outlook anticipates $38.1 billion in revenue and $5.4 billion in earnings by 2028. This scenario assumes a 5.6% annual revenue growth and a $0.7 billion increase in earnings from the current $4.7 billion level.

Uncover how PayPal Holdings' forecasts yield a $82.22 fair value, a 18% upside to its current price.

Exploring Other Perspectives

Forty-nine private investors in the Simply Wall St Community pegged PayPal’s fair value between US$75 and US$116 per share. Amid starkly varied outlooks, many are weighing competition from tech giants as a critical driver of PayPal’s performance. Explore more viewpoints to see how differently the risks and opportunities can be weighed.

Explore 49 other fair value estimates on PayPal Holdings - why the stock might be worth as much as 66% more than the current price!

Build Your Own PayPal Holdings Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your PayPal Holdings research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free PayPal Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate PayPal Holdings' overall financial health at a glance.

Contemplating Other Strategies?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- The end of cancer? These 27 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:PYPL

PayPal Holdings

Operates a technology platform that enables digital payments for merchants and consumers worldwide.

Outstanding track record and undervalued.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion