Advertisement

- United States

- /

- Diversified Financial

- /

- NasdaqGM:NMIH

How Investors May Respond To NMI Holdings (NMIH) Book Value Growth and Operational Profitability Gains

Simply Wall St

Reviewed by Sasha Jovanovic

- In recent days, NMI Holdings reported robust net premium growth, stronger combined ratios, and steady increases in book value, highlighting ongoing improvements to operational profitability and financial strength.

- This set of positive results suggests the company is efficiently scaling its core business and building equity, signaling growing confidence in its ability to manage risk and expand market presence.

- We'll explore how the company's book value growth and operational gains might further shape its investment narrative and future prospects.

Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

NMI Holdings Investment Narrative Recap

To own NMI Holdings, you need to believe that the company can keep scaling its mortgage insurance business while managing credit risks from shifting housing conditions and regulatory changes. The recent report of strong net premium growth and higher book value signals operational momentum but may not meaningfully alter near-term catalysts or ease the principal risk: adverse moves in housing markets or regulation that could pressure claims and margins.

Among recent announcements, the ongoing share repurchase program, most recently adding 627,911 shares bought back for US$23.17 million, stands out as aligning with the company’s positive financial results. This buyback supports book value accretion but, given the unchanged industry headwinds, does not substantially shift the core risk investors should track regarding housing market resets and regulatory shifts.

Yet, in contrast to the growth story, investors should not overlook the concentration of risk in key real estate markets and how this...

Read the full narrative on NMI Holdings (it's free!)

NMI Holdings' narrative projects $812.2 million revenue and $410.6 million earnings by 2028. This requires 6.1% yearly revenue growth and a $32.9 million earnings increase from $377.7 million.

Uncover how NMI Holdings' forecasts yield a $44.14 fair value, a 20% upside to its current price.

Exploring Other Perspectives

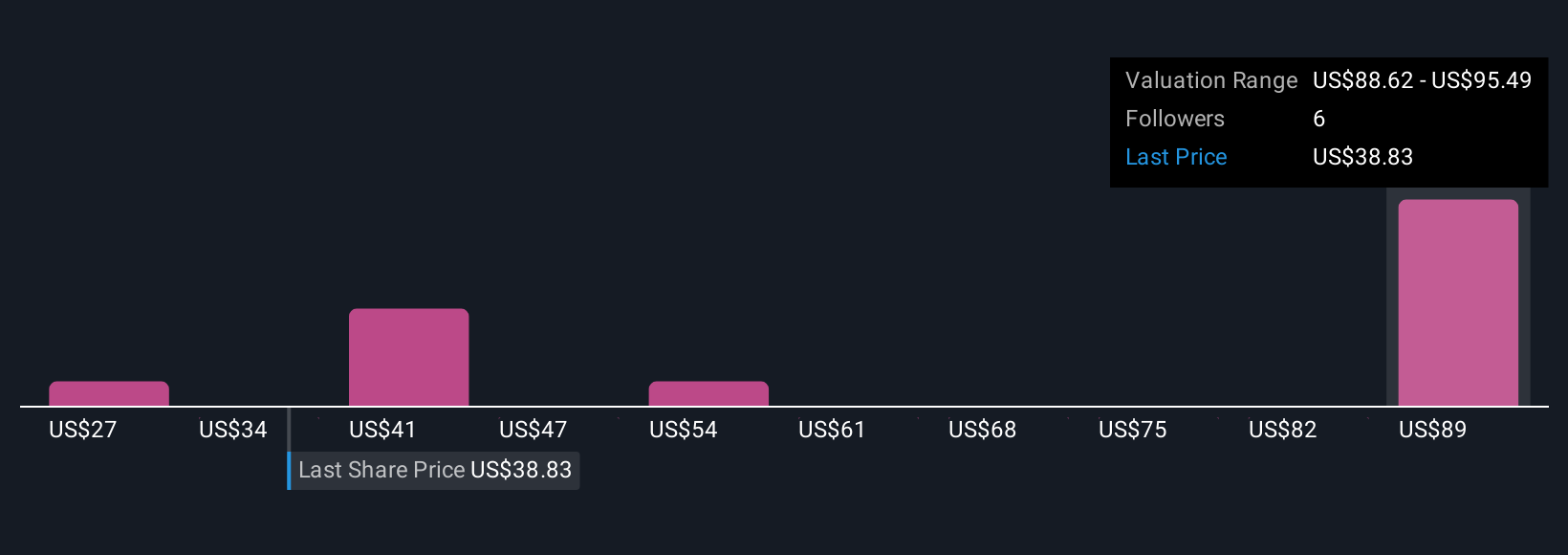

Fair value estimates from four Simply Wall St Community members span US$26.80 to US$96.58 per share, capturing a wide spectrum of investor outlooks. While many see ongoing earnings and book value gains, you should also be mindful of elevated claims exposure tied to regional housing volatility.

Explore 4 other fair value estimates on NMI Holdings - why the stock might be worth over 2x more than the current price!

Build Your Own NMI Holdings Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your NMI Holdings research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free NMI Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NMI Holdings' overall financial health at a glance.

No Opportunity In NMI Holdings?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Find companies with promising cash flow potential yet trading below their fair value.

- The end of cancer? These 27 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if NMI Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:NMIH

NMI Holdings

Provides private mortgage guaranty insurance services in the United States.

Very undervalued with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.6% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.6% undervalued

GM

Community Contributor