Advertisement

- United States

- /

- Capital Markets

- /

- NasdaqGS:MORN

Morningstar (MORN): Exploring Valuation After AI Strategy Shift and $1 Billion Buyback Announcement

Simply Wall St

Reviewed by Simply Wall St

Morningstar (MORN) just announced a $1 billion share repurchase program over the next three years, along with new plans to ramp up operational efficiency and data delivery using AI. Both moves signal management’s intent to strengthen long-term value for investors.

See our latest analysis for Morningstar.

Morningstar’s latest moves come after a stretch of declining momentum, with the share price down 18.1% in the last quarter and the one-year total shareholder return sitting at -38.9%. Despite the new buyback and AI-driven efficiency push, recent insider selling and a dip in short interest have kept investors cautious about a quick turnaround. Long-term earnings growth shows some foundation for optimism.

If you’re weighing opportunities beyond the headlines, now’s a smart time to broaden your search and discover fast growing stocks with high insider ownership

With the stock trading nearly 30% below analyst price targets despite steady earnings growth and new initiatives, investors must decide whether Morningstar presents a hidden bargain or if the market is accurately considering its future prospects.

Price-to-Earnings of 23.5x: Is it justified?

Morningstar's price-to-earnings ratio currently stands at 23.5x, slightly below the Capital Markets industry average of 23.6x but significantly above its estimated fair ratio of 14x. At its last close price of $214.86, the stock looks expensive on this metric when compared with what might be justified by fundamentals.

The price-to-earnings ratio tells investors how much they are paying for each dollar of the company's earnings. For Morningstar, this ratio helps frame whether expectations for future profits are already factored into the share price, particularly in a sector known for steady but not explosive growth.

Despite steady earnings growth and seasoned management, the premium multiple suggests the market could be pricing in improved earnings quality or long-term strategic value. However, compared to the fair ratio of 14x, there is a considerable gap, indicating the market may need more convincing on future growth potential. If investor sentiment shifts or earnings growth fails to accelerate, the multiple could revert closer to that fair level.

Explore the SWS fair ratio for Morningstar

Result: Price-to-Earnings of 23.5x (OVERVALUED)

However, slowing revenue and net income growth, along with persistent market skepticism, could challenge the case for a sustained recovery in Morningstar shares.

Find out about the key risks to this Morningstar narrative.

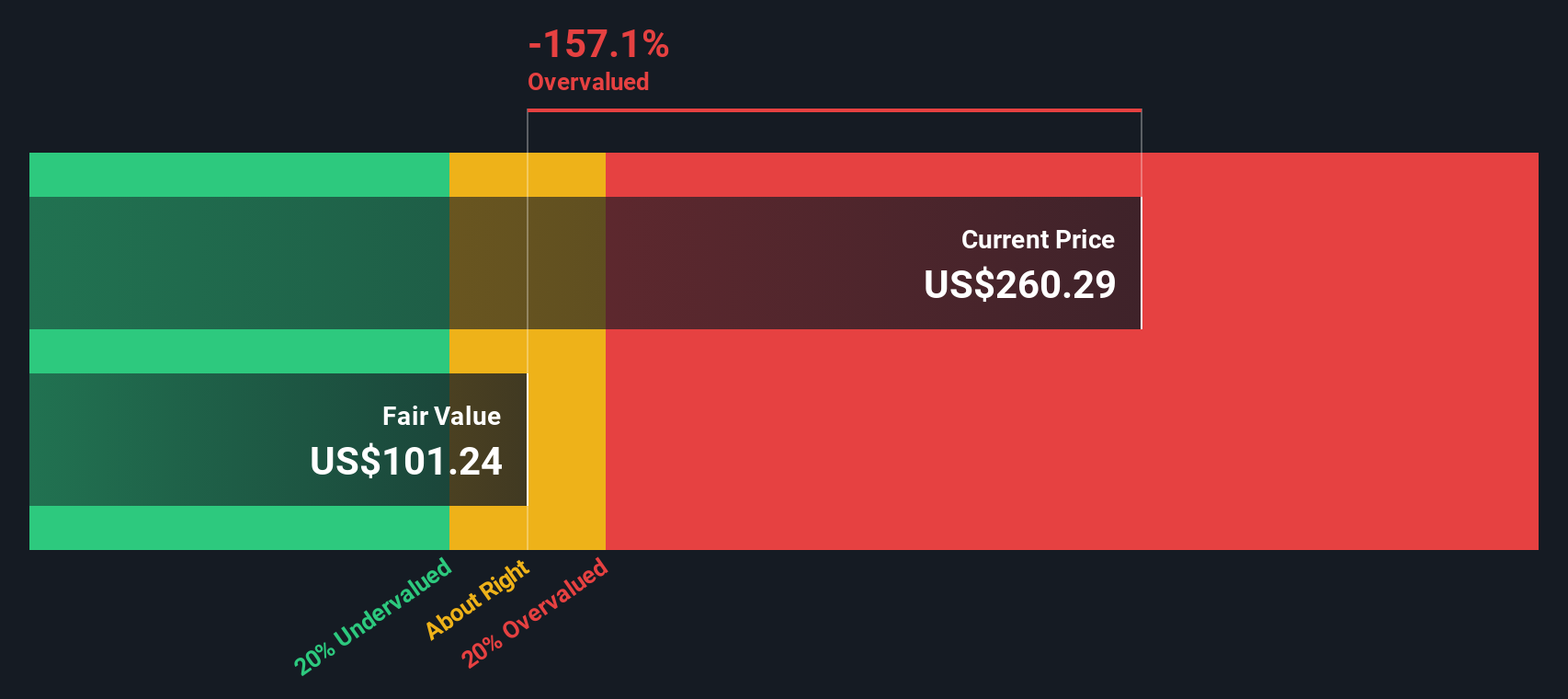

Another View: Our DCF Model Tells a Different Story

Taking a look at the SWS DCF model, Morningstar appears significantly overvalued, with shares trading well above our calculated fair value of $94.02. This sharp contrast with the price-to-earnings view challenges whether the market is factoring in too much future growth or simply not enough risk. Which view will turn out to be right?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Morningstar for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 920 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Morningstar Narrative

If you see Morningstar’s story differently or want to dig into the numbers yourself, you can quickly build your own view in just a few minutes. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Morningstar.

Looking for more investment ideas?

Level up your portfolio and avoid missing out on opportunities. Let Simply Wall Street’s unique screeners surface smart new ideas you might have missed.

- Boost your income by scanning for reliable yields with these 15 dividend stocks with yields > 3% that consistently pay out more than 3%.

- Spot cutting-edge leaders in medicine and tech by targeting these 30 healthcare AI stocks as they transform the future of healthcare with artificial intelligence.

- Ride the next wave of technology by finding these 25 AI penny stocks positioned for growth in areas such as automation and advanced analytics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:MORN

Morningstar

Provides independent investment insights in the United States, Asia, Australia, Canada, Continental Europe, the United Kingdom, and internationally.

Proven track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

930 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative