Advertisement

- United States

- /

- Diversified Financial

- /

- NasdaqGS:FLYW

Flywire (FLYW): Assessing Valuation After Rebounding Financials and Recent Share Price Recovery

Simply Wall St

Reviewed by Kshitija Bhandaru

Flywire (FLYW) has delivered a strong year in terms of net income growth, with its most recent financial results showing a noticeable uptick. The company’s ability to boost annual revenue growth by 14% points to a business that is gaining traction in its core markets.

See our latest analysis for Flywire.

Flywire’s share price has bounced back with a 19.5% return over the past 90 days, helping reverse some of the sharp declines seen earlier in the year. However, its one-year total shareholder return still sits at -25.9%. Momentum looks to be rebuilding as investors respond to the recent financial results and steady revenue gains.

If you’re watching how fintech favorites can quickly recover lost ground, the next step is to broaden your search and discover fast growing stocks with high insider ownership

With shares still trading below analyst price targets and recent financial momentum on its side, investors are left wondering: Does Flywire have more upside ahead, or is the current valuation already reflecting its future prospects?

Most Popular Narrative: 11% Undervalued

With Flywire’s narrative fair value at $14.55 compared to a last close of $12.95, analysts see room for shares to catch up. The story behind this valuation is rooted in expectations of accelerating financial performance as global markets drive growth and margins improve.

Ongoing investment in proprietary technology, AI-driven automation, and integration capabilities is yielding significant platform efficiencies (for example, 25% operational cost improvements, 90% automated payment matching, and 40% automated customer service), supporting Flywire's ability to maintain or increase net margins and deliver stronger earnings leverage as scale increases.

The underlying factor behind this price target is bold projections for future margins and rapid growth outside Flywire's traditional strongholds. Want to uncover the crucial numbers and assumptions powering this bullish narrative? Find out what justifies Flywire’s premium positioning in the full story.

Result: Fair Value of $14.55 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent margin pressure in new verticals and regulatory risks in key international markets could threaten Flywire’s projected revenue and earnings growth.

Find out about the key risks to this Flywire narrative.

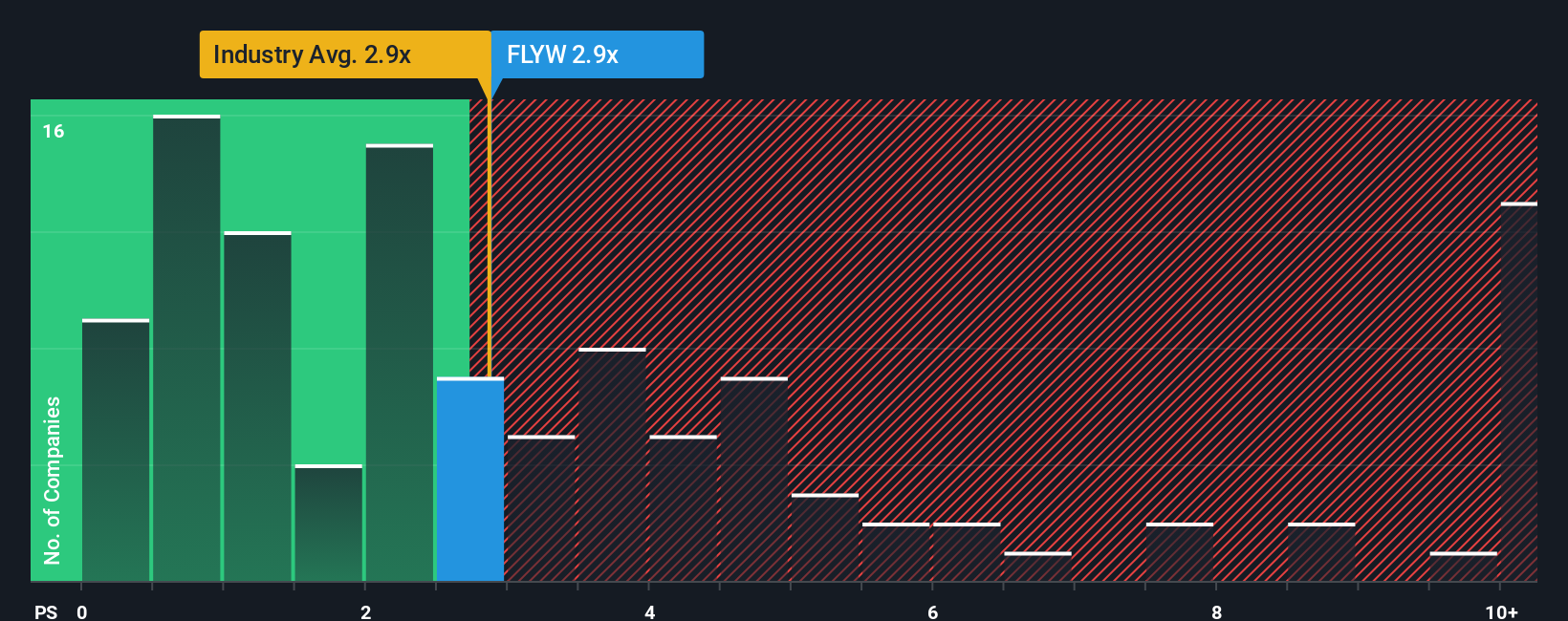

Another View: Market Ratios Signal a Premium

Looking at Flywire through the lens of price-to-sales, the stock trades at 2.9 times sales, which is noticeably higher than both the US industry average of 2.5x and its peer group at 2.4x. This premium carries valuation risk. If expectations falter, the market could reprice closer to a fair ratio of 2.5x. Are investors too optimistic, or does Flywire justify the added cost?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Flywire Narrative

Whether you want a different perspective or would rather trust your own analysis, you can easily shape your personal Flywire narrative in just a few minutes: Do it your way

A great starting point for your Flywire research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Expand your investment horizons and spot new opportunities before others do. Use Simply Wall Street’s powerful screener to pinpoint stocks that fit your strategy.

- Boost your portfolio’s potential by targeting value with these 877 undervalued stocks based on cash flows, which stand out for their strong fundamentals and favorable cash flow metrics.

- Capitalize on the surge in artificial intelligence innovation by scanning for up-and-coming leaders with these 24 AI penny stocks.

- Maximize your passive income with steady-yielding picks found among these 18 dividend stocks with yields > 3%, offering attractive payouts and resilient earning profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:FLYW

Flywire

Operates as a payments enablement and software company in the United States and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|20.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.1% undervalued

LI

Community Contributor