Luckin Coffee (OTCPK:LKNC.Y) shares slipped after a dip of roughly 1% as investors reacted to the latest trading session. The stock's modest movement comes amid consistent annual revenue and net income growth for the company.

Luckin Coffee's share price has cooled off a bit in the past month, but the bigger story is its momentum. With a 47.1% share price return so far this year and an impressive 61.3% total shareholder return for the past 12 months, Luckin continues building on strong long-term gains seen over three- and five-year periods as well.

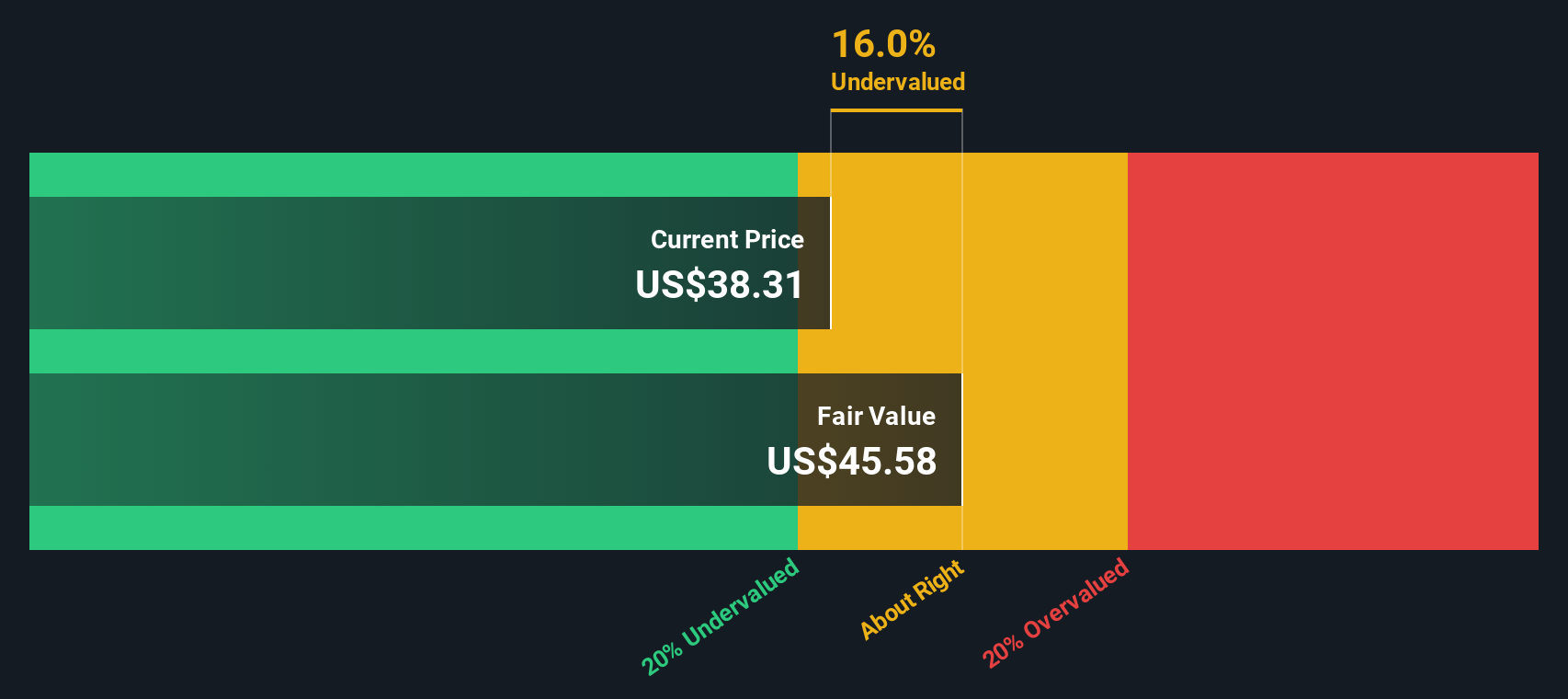

With shares trading roughly 18% below analyst price targets and showing years of durable growth, investors must decide whether Luckin Coffee is undervalued right now or if the company's future potential is already fully accounted for.

Advertisement

Most Popular Narrative: 15.5% Undervalued

Luckin Coffee's narrative-driven fair value sits well above the latest close, hinting the share price still trails underlying business potential. This gap sets the stage for what could be a pivotal driver.

Ongoing investments in proprietary supply chain infrastructure, such as the commissioning of the new Xiamen roasting facility and integration of existing plants, are expected to enhance vertical integration, lower cost of materials as a percent of revenues, and drive expansion of gross and net margins over the long term.

Curious how a relentless push into operational efficiency and digital strategy transforms into a bold valuation? The narrative hinges on aggressive expansion, innovative customer engagement, and carefully modeled margin shifts, all driven by long-term growth assumptions that could surprise even seasoned investors. Unpack the bigger financial picture behind Luckin’s premium pricing and see what data really underpins this view.

However, rising competition and the risk of overexpansion could challenge Luckin's growth story. These factors may put pressure on margins and test the durability of its current momentum.

Another View: Our DCF Model Challenges the Narrative

While narrative-led valuation signals Luckin Coffee is still below its potential, our DCF model tells a different story. It estimates a fair value of $36.34, which is below the current share price. Could market optimism be running ahead of fundamentals?

If you have a different perspective, or want to dig into the numbers yourself, you can craft your own Luckin Coffee story in just minutes. Do it your way

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Luckin Coffee.

Looking for More Smart Investment Ideas?

Don’t let your next opportunity slip past you. Leverage the Simply Wall Street Screener to spot stocks on the move in today’s market.

Tap into high-growth trends in artificial intelligence by checking out these 26 AI penny stocks, which are at the front line of technological change, automation, and efficiency gains.

Accelerate your income strategy and see what sets apart these 18 dividend stocks with yields > 3%, which consistently reward shareholders with strong yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies