Yum! Brands (YUM) shares have dipped slightly over the past week, falling by 3% and slipping nearly 6% for the month. The stock’s longer-term trend, however, remains broadly positive for investors.

Despite this pullback, Yum! Brands' momentum over the past year remains solid, with a 1-year total shareholder return of 8.4% and an impressive 65% return over five years. This recent dip follows a period of steady growth, suggesting that investors are reassessing risk and value in light of the company’s longer-term track record.

If you’re interested in finding more companies with the potential for standout performance and strong ownership backing, now is a perfect time to discover fast growing stocks with high insider ownership

With shares trading below analyst price targets and recent growth in both revenue and net income, investors are left wondering whether Yum! Brands' current slump represents an undervalued entry point or if the market has already accounted for the gains ahead.

Advertisement

Most Popular Narrative: 11% Undervalued

Yum! Brands' most widely tracked narrative sees fair value well above the latest close, attracting attention as consensus views diverge.

The rapid acceleration and global rollout of Yum!'s Byte digital platform, including AI-driven marketing, operational automation, and proprietary ordering/delivery solutions, positions the company to capture higher transaction volumes, expand check sizes, and enhance customer loyalty. This drives both top-line revenue growth and improves net margins over the long term.

What hidden drivers merit this higher valuation? There is a bold assumption tied directly to new technology, global scale, and ambitious profitability gains. Don’t miss seeing what powers this outcome. Numbers and strategies you aren’t expecting could be the linchpin for these projections.

However, persistent underperformance in key brands or lagging tech adoption could challenge these upbeat projections and potentially pressure revenue and future earnings growth.

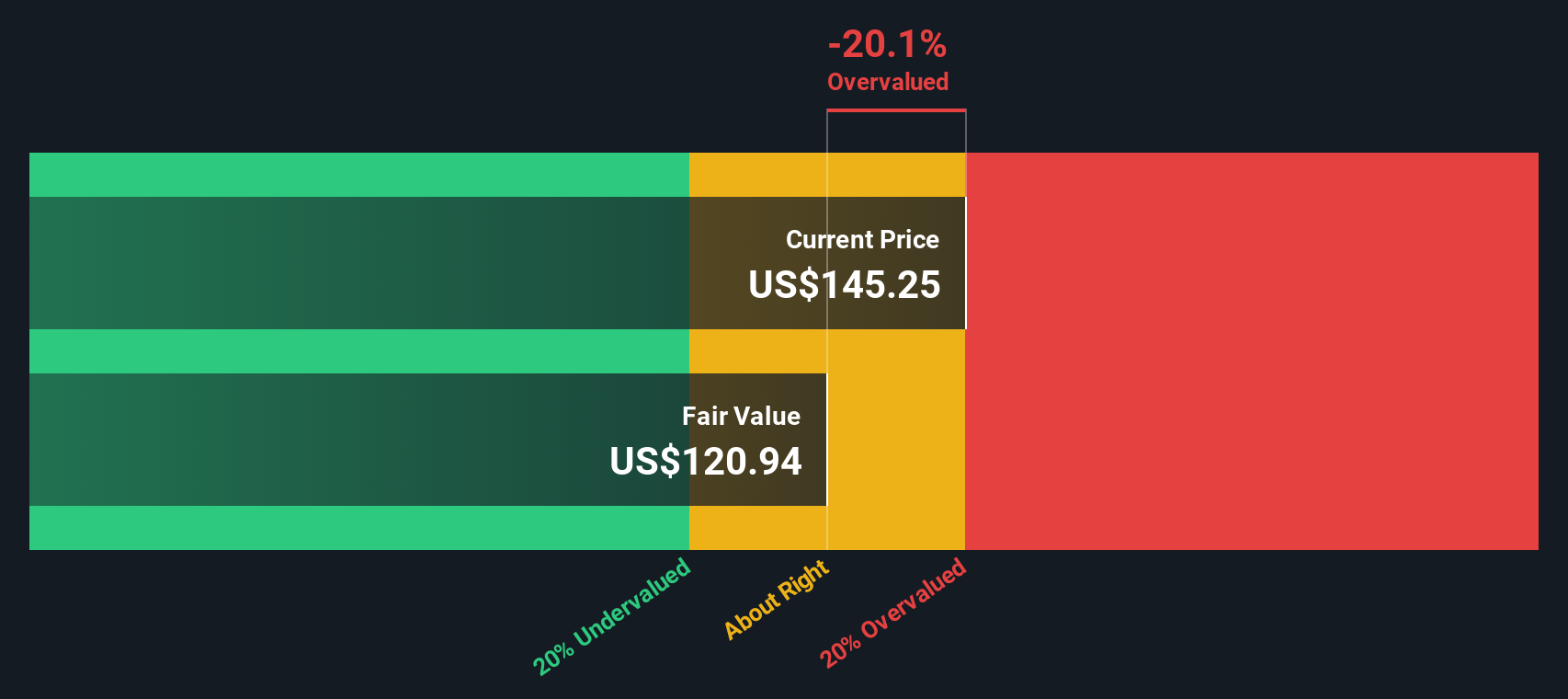

Looking at Yum! Brands from the perspective of our DCF model leads to a different conclusion. The stock appears overvalued, with a fair value estimate of $120.81 per share, which is well below its current price. If this view proves correct, today's entry point could actually be riskier than it first looks. Could the DCF be catching something the market is missing?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Yum! Brands for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Yum! Brands Narrative

If you want a different perspective or prefer to investigate the numbers your own way, you can easily craft your own take in just a few minutes. Do it your way

A great starting point for your Yum! Brands research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Don’t let opportunities pass you by while others position themselves for tomorrow’s winners. You can spot your next smart move with a few minutes on the Simply Wall Street Screener.

Secure consistent cash flow by checking out companies with attractive payouts via these 17 dividend stocks with yields > 3%, and see which stocks are rewarding investors with yields over 3%.

Get ahead of the curve in health innovation and tap into breakthroughs transforming medicine by browsing these 33 healthcare AI stocks.

Maximize value by targeting companies currently priced below their intrinsic worth using these 872 undervalued stocks based on cash flows. This approach helps you act before the market catches up.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks