Lucky Strike Entertainment (LUCK) shares moved 3% higher today, catching some attention from investors. While there wasn’t a high-profile catalyst, moves like this often have traders checking for clues about shifting sentiment or potential upcoming announcements.

While Lucky Strike Entertainment’s latest 3% jump puts some spark back in the share price, longer-term momentum has been mixed. The 7-day share price return of 8.3% suggests renewed optimism among traders, but this sits against a one-year total shareholder return of -36.8% as the stock continues to struggle for sustainable traction.

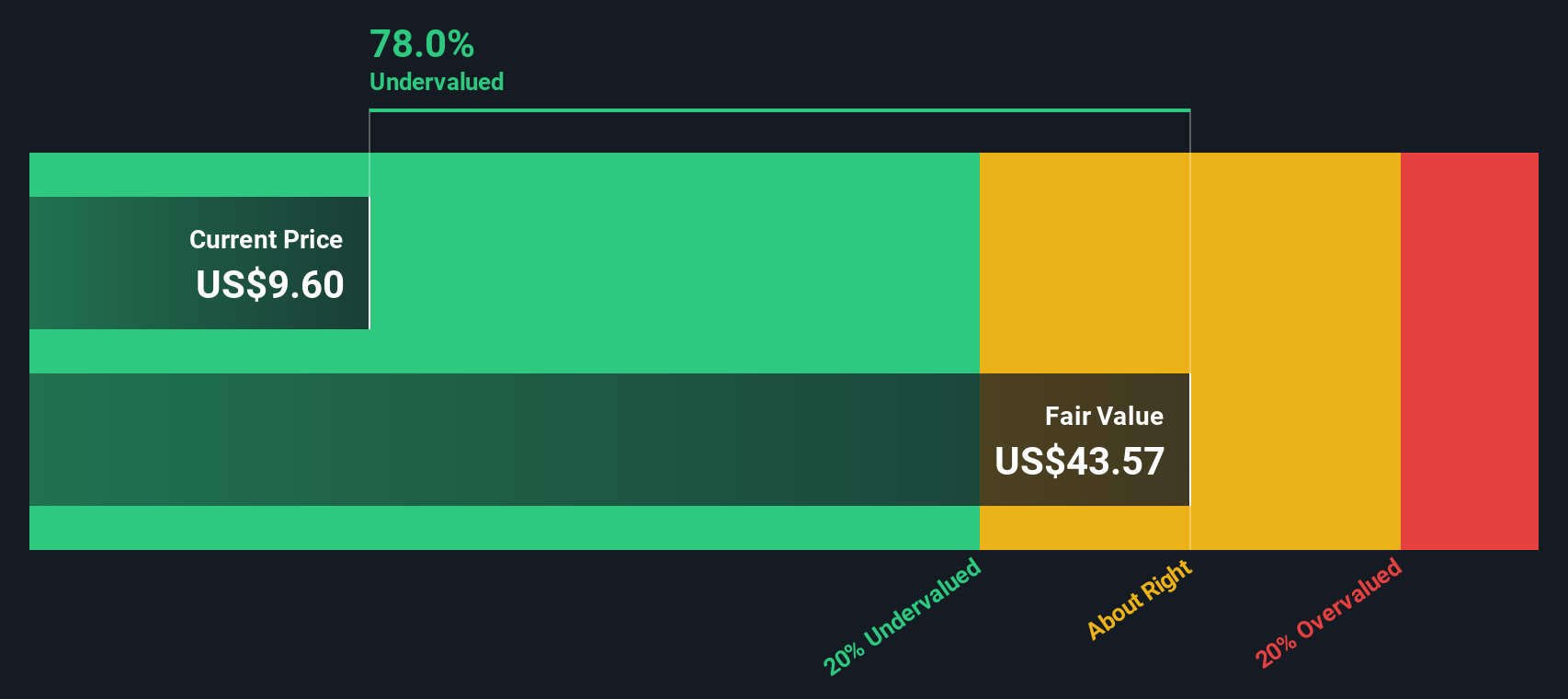

With Lucky Strike Entertainment’s price still well below analyst targets even after today’s pop, investors are left to wonder if the stock is undervalued or if the market is already factoring in any hopes for a rebound.

Advertisement

Most Popular Narrative: 43.2% Undervalued

The prevailing narrative puts Lucky Strike Entertainment’s fair value well above its last close, indicating a deep disconnect between analyst targets and market pricing. A significant uplift is required for the stock to meet consensus assumptions, setting high expectations for future performance.

The conversion of Bowlero locations to Lucky Strike, alongside targeted, higher-return marketing spend and refreshed branding, is already showing early signs of comp improvement in key markets and is expected to meaningfully accelerate same-store sales and operating leverage as the transition scales system-wide.

Curious why analysts are betting on a major turnaround? Their valuation hinges on projections of sustained revenue gains and a future profit multiple more often seen in high-growth sectors. What growth levers and bold margin assumptions are shaping this sky-high target? Read the full narrative to uncover the data fueling these expectations.

However, persistent labor cost inflation or growing consumer preference for at-home entertainment could quickly diminish the current optimism around Lucky Strike’s rebound.

While the market sees room for upside based on revenue and earnings projections, the SWS DCF model offers a reality check. It suggests Lucky Strike Entertainment could be overvalued at current prices and raises questions about whether analyst optimism is already reflected in the share price. Could growth fall short of the lofty expectations?

Build Your Own Lucky Strike Entertainment Narrative

If you see things differently or want to dive deeper into the numbers, you can shape your own Lucky Strike Entertainment story in just a few minutes. Do it your way.

A great starting point for your Lucky Strike Entertainment research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Smart investors know the real edge comes from spotting opportunities before the crowd. Broaden your game plan and see what’s on the radar right now:

Capitalize on the AI revolution by selecting these 25 AI penny stocks with breakthrough potential in automation, machine learning, and digital transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies