Advertisement

- United States

- /

- Hospitality

- /

- NYSE:CHH

Choice Hotels International (CHH) Is Up 6.0% After Canadian Consolidation Drives Profit Guidance Raise Has the Bull Case Changed?

Simply Wall St

Reviewed by Sasha Jovanovic

- On November 5, 2025, Choice Hotels International reported third-quarter results, delivering improved revenue of US$447.34 million and net income of US$180 million, reflecting strong profitability and the consolidation of its Canadian operations.

- The company raised its full-year profit guidance after recognizing a significant gain from acquiring full ownership in Choice Hotels Canada, highlighting international expansion as a major driver of recent performance.

- We’ll examine how Choice Hotels’ upward earnings revision, driven by Canadian consolidation, influences its investment case and future growth outlook.

AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Choice Hotels International Investment Narrative Recap

To be a shareholder in Choice Hotels International, you need to believe in its ability to drive sustained growth through global expansion, resilient brand positioning across price segments, and effective franchise operations. The recent announcement of strong Q3 results and an upward earnings revision, primarily driven by the consolidation of Choice Hotels Canada, appears to reinforce the company’s short-term growth catalyst, international expansion. However, it does not fully offset the biggest risk currently facing the business: ongoing softness in government and international inbound travel affecting RevPAR and near-term revenue momentum.

Among the company’s recent announcements, the full-year profit guidance increase after recognizing a US$100 million gain from the Canada acquisition is most pertinent. This development highlights that international consolidation and new market entries have given the business a meaningful earnings boost in the short term, and may provide a partial buffer against lingering demand risks in the U.S. and certain global segments.

Yet, in contrast to rising profit forecasts, investors should be aware that persistent weakness in government and international travel could continue to pressure...

Read the full narrative on Choice Hotels International (it's free!)

Choice Hotels International's outlook anticipates $1.8 billion in revenue and $354.2 million in earnings by 2028. This is based on a forecasted annual revenue growth rate of 30.6% and a $48 million increase in earnings from the current $306.2 million.

Uncover how Choice Hotels International's forecasts yield a $117.50 fair value, a 19% upside to its current price.

Exploring Other Perspectives

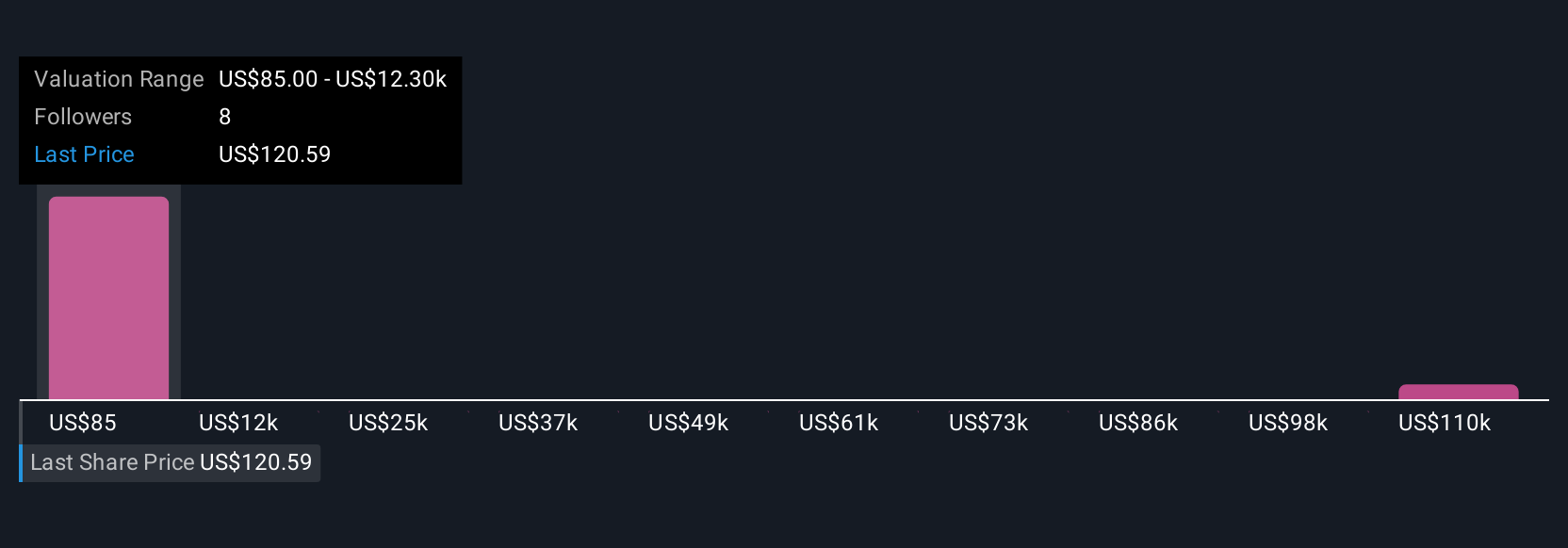

Four market participants in the Simply Wall St Community have set fair value estimates for Choice Hotels International ranging from US$117.50 to an outlier of US$122,273.07. While views differ greatly, the persistent risk to RevPAR growth and earnings from softer international and government demand remains critical in assessing future performance.

Explore 4 other fair value estimates on Choice Hotels International - why the stock might be worth just $117.50!

Build Your Own Choice Hotels International Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Choice Hotels International research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Choice Hotels International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Choice Hotels International's overall financial health at a glance.

Want Some Alternatives?

Our top stock finds are flying under the radar-for now. Get in early:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 35 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CHH

Choice Hotels International

Operates as a hotel franchisor in the United States and internationally.

Undervalued with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor