Advertisement

- United States

- /

- Hospitality

- /

- NasdaqGS:WYNN

Why Wynn Resorts (WYNN) Is Up 9.4% After UAE Casino Plans Gain Analyst Praise and Investor Interest

Simply Wall St

Reviewed by Sasha Jovanovic

- Wynn Resorts recently received significant attention following upgrades from leading financial institutions amid major property projects in the United Arab Emirates and continued enhancements to its Las Vegas flagship resorts.

- Analysts and investors are highlighting the company's ambitious international expansion, particularly the development of what will be the UAE’s first casino, as a potential game-changer for the global luxury hospitality and gaming market.

- We’ll explore how optimism surrounding Wynn’s landmark UAE resort projects could influence the company’s investment narrative going forward.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Wynn Resorts Investment Narrative Recap

To be a shareholder in Wynn Resorts today, you need to believe in the company’s ability to capture premium demand across global luxury hospitality and gaming, with near-term focus on successful execution and returns from key international projects like Wynn Al Marjan Island. With attention from recent analyst upgrades and increased price targets, the most important catalyst remains clear and visible progress in the UAE; however, the scale of capital outlays means that underperformance or cost overruns could weigh on investor sentiment. This news does not materially diminish the main risks linked to capital allocation and exposure to regulatory shifts in Macau, which still require close monitoring.

Among recent announcements, Citigroup’s upgrade of Wynn Resorts, raising its price target from US$124.50 to US$160 following the latest updates on Wynn Al Marjan Island, stands out as highly relevant. Anticipation around the project’s early 2027 opening, paired with plans for a second luxury resort with Aman Group, has underpinned renewed confidence in the company’s international growth prospects and its pivotal role in establishing gaming in the UAE.

In contrast, investors should also be aware of the risks if ambitious capital expenditure in multiple regions fails to translate into strong returns...

Read the full narrative on Wynn Resorts (it's free!)

Wynn Resorts is expected to reach $8.0 billion in revenue and $624.0 million in earnings by 2028. This outlook is based on an annual revenue growth rate of 4.6% and an earnings increase of $240.1 million from current earnings of $383.9 million.

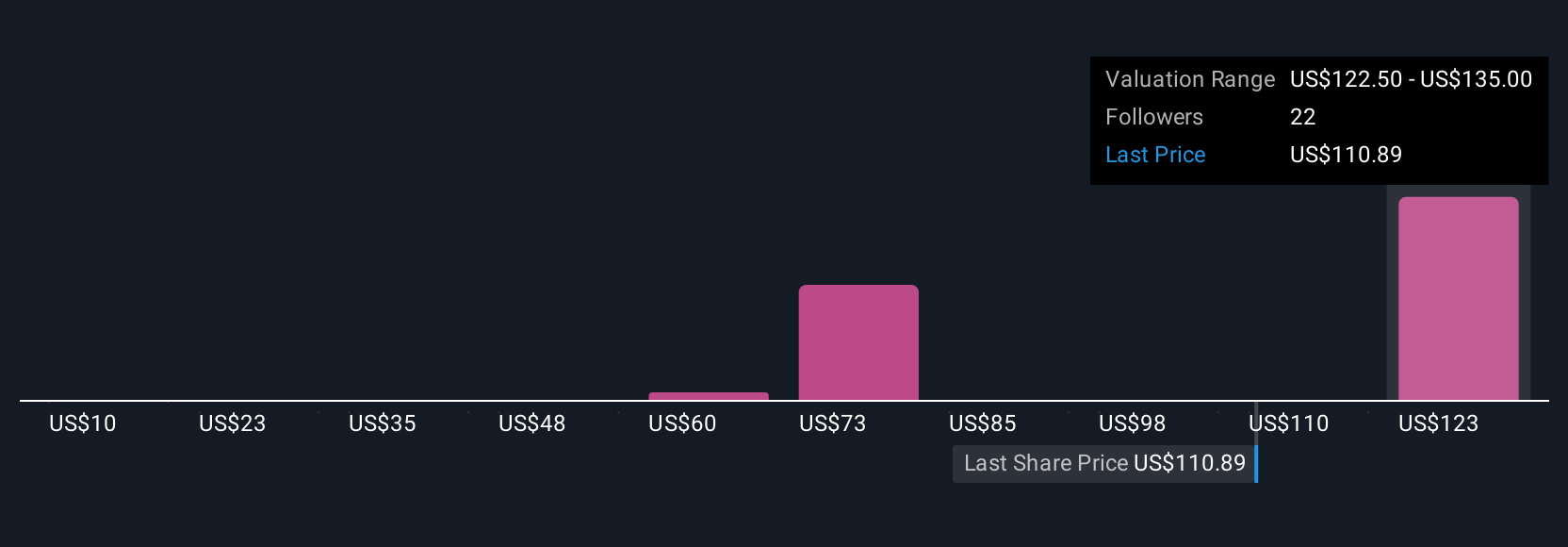

Uncover how Wynn Resorts' forecasts yield a $137.91 fair value, a 7% upside to its current price.

Exploring Other Perspectives

Nine members of the Simply Wall St Community placed fair value estimates on Wynn Resorts ranging from just US$10 up to US$137.91 per share. While optimism about the UAE catalyst builds, keep in mind that exposure to regulatory change in Macau could shift future trajectories, so you may want to review a range of community perspectives before making up your mind.

Explore 9 other fair value estimates on Wynn Resorts - why the stock might be worth less than half the current price!

Build Your Own Wynn Resorts Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Wynn Resorts research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Wynn Resorts research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Wynn Resorts' overall financial health at a glance.

Searching For A Fresh Perspective?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Wynn Resorts might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:WYNN

Low risk with limited growth.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

JO

JohnJ on Worldline ·

No miracle in sight

Fair Value:€7.0178.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

79 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

90 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

928 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative