Stock Analysis

- United States

- /

- Hospitality

- /

- NasdaqGS:SBUX

Many Would Be Envious Of Starbucks' (NASDAQ:SBUX) Excellent Returns On Capital

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. That's why when we briefly looked at Starbucks' (NASDAQ:SBUX) ROCE trend, we were very happy with what we saw.

What Is Return On Capital Employed (ROCE)?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. Analysts use this formula to calculate it for Starbucks:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

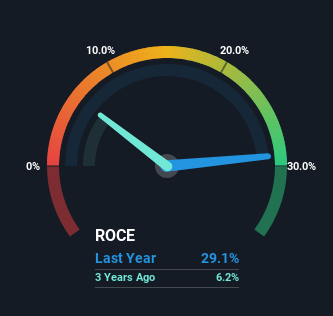

0.29 = US$5.8b ÷ (US$29b - US$9.4b) (Based on the trailing twelve months to December 2023).

So, Starbucks has an ROCE of 29%. In absolute terms that's a great return and it's even better than the Hospitality industry average of 9.5%.

Check out our latest analysis for Starbucks

In the above chart we have measured Starbucks' prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering Starbucks for free.

So How Is Starbucks' ROCE Trending?

In terms of Starbucks' history of ROCE, it's quite impressive. The company has employed 36% more capital in the last five years, and the returns on that capital have remained stable at 29%. With returns that high, it's great that the business can continually reinvest its money at such appealing rates of return. If Starbucks can keep this up, we'd be very optimistic about its future.

Our Take On Starbucks' ROCE

In summary, we're delighted to see that Starbucks has been compounding returns by reinvesting at consistently high rates of return, as these are common traits of a multi-bagger. And given the stock has only risen 35% over the last five years, we'd suspect the market is beginning to recognize these trends. That's why it could be worth your time looking into this stock further to discover if it has more traits of a multi-bagger.

If you want to know some of the risks facing Starbucks we've found 2 warning signs (1 is significant!) that you should be aware of before investing here.

High returns are a key ingredient to strong performance, so check out our free list ofstocks earning high returns on equity with solid balance sheets.

Valuation is complex, but we're helping make it simple.

Find out whether Starbucks is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:SBUX

Starbucks

Starbucks Corporation, together with its subsidiaries, operates as a roaster, marketer, and retailer of coffee worldwide.

Undervalued with solid track record and pays a dividend.