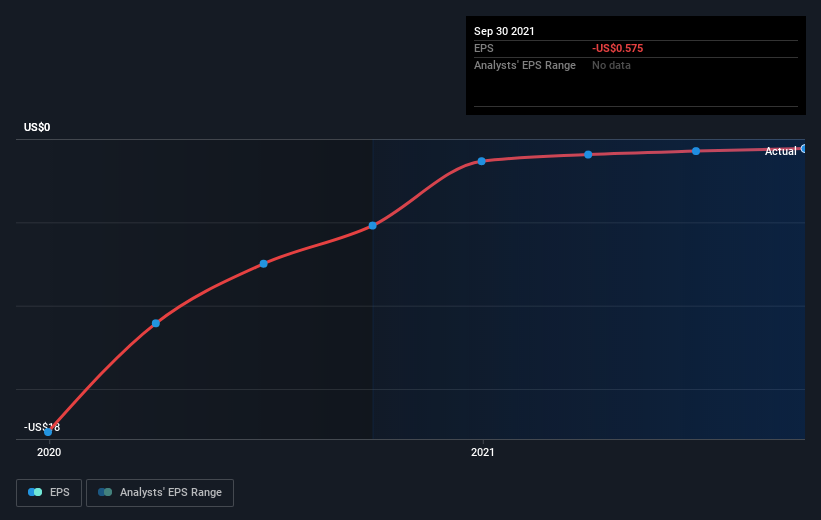

With the business potentially at an important milestone, we thought we'd take a closer look at Muscle Maker, Inc.'s (NASDAQ:GRIL) future prospects. Muscle Maker, Inc. owns, operates, and franchises Muscle Maker Grill and Healthy Joe’s restaurants under the Muscle Maker Grill name. The US$12m market-cap company posted a loss in its most recent financial year of US$10m and a latest trailing-twelve-month loss of US$7.7m shrinking the gap between loss and breakeven. As path to profitability is the topic on Muscle Maker's investors mind, we've decided to gauge market sentiment. In this article, we will touch on the expectations for the company's growth and when analysts expect it to become profitable.

Check out our latest analysis for Muscle Maker

Expectations from some of the American Hospitality analysts is that Muscle Maker is on the verge of breakeven. They expect the company to post a final loss in 2022, before turning a profit of US$3.0m in 2023. The company is therefore projected to breakeven just over a year from now. How fast will the company have to grow each year in order to reach the breakeven point by 2023? Working backwards from analyst estimates, it turns out that they expect the company to grow 86% year-on-year, on average, which signals high confidence from analysts. Should the business grow at a slower rate, it will become profitable at a later date than expected.

We're not going to go through company-specific developments for Muscle Maker given that this is a high-level summary, though, bear in mind that generally a high growth rate is not out of the ordinary, particularly when a company is in a period of investment.

Before we wrap up, there’s one aspect worth mentioning. The company has managed its capital prudently, with debt making up 12% of equity. This means that it has predominantly funded its operations from equity capital, and its low debt obligation reduces the risk around investing in the loss-making company.

Next Steps:

There are too many aspects of Muscle Maker to cover in one brief article, but the key fundamentals for the company can all be found in one place – Muscle Maker's company page on Simply Wall St. We've also compiled a list of relevant factors you should look at:

- Valuation: What is Muscle Maker worth today? Has the future growth potential already been factored into the price? The intrinsic value infographic in our free research report helps visualize whether Muscle Maker is currently mispriced by the market.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Muscle Maker’s board and the CEO’s background.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:SDOT

Sadot Group

Provides supply chain solutions that address growing food security challenges worldwide.

High growth potential and fair value.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)