- United States

- /

- Food and Staples Retail

- /

- NasdaqGS:WBA

After Leaping 26% Walgreens Boots Alliance, Inc. (NASDAQ:WBA) Shares Are Not Flying Under The Radar

Walgreens Boots Alliance, Inc. (NASDAQ:WBA) shareholders have had their patience rewarded with a 26% share price jump in the last month. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 32% over that time.

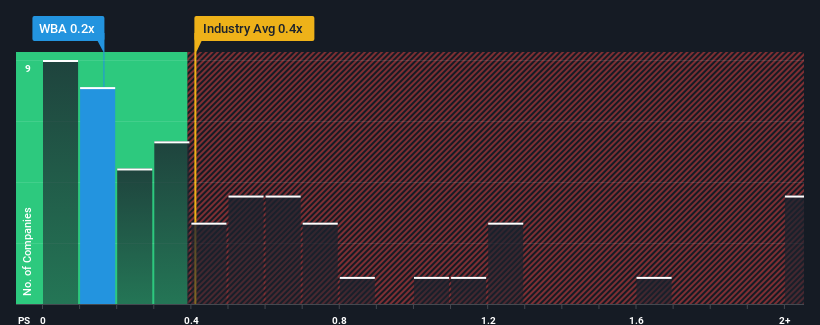

Although its price has surged higher, there still wouldn't be many who think Walgreens Boots Alliance's price-to-sales (or "P/S") ratio of 0.2x is worth a mention when the median P/S in the United States' Consumer Retailing industry is similar at about 0.4x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

View our latest analysis for Walgreens Boots Alliance

What Does Walgreens Boots Alliance's P/S Mean For Shareholders?

There hasn't been much to differentiate Walgreens Boots Alliance's and the industry's revenue growth lately. The P/S ratio is probably moderate because investors think this modest revenue performance will continue. Those who are bullish on Walgreens Boots Alliance will be hoping that revenue performance can pick up, so that they can pick up the stock at a slightly lower valuation.

Want the full picture on analyst estimates for the company? Then our free report on Walgreens Boots Alliance will help you uncover what's on the horizon.Do Revenue Forecasts Match The P/S Ratio?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Walgreens Boots Alliance's to be considered reasonable.

Taking a look back first, we see that the company managed to grow revenues by a handy 4.8% last year. The solid recent performance means it was also able to grow revenue by 14% in total over the last three years. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

Turning to the outlook, the next three years should generate growth of 4.0% per year as estimated by the analysts watching the company. With the industry predicted to deliver 4.4% growth per annum, the company is positioned for a comparable revenue result.

With this in mind, it makes sense that Walgreens Boots Alliance's P/S is closely matching its industry peers. It seems most investors are expecting to see average future growth and are only willing to pay a moderate amount for the stock.

What We Can Learn From Walgreens Boots Alliance's P/S?

Its shares have lifted substantially and now Walgreens Boots Alliance's P/S is back within range of the industry median. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

A Walgreens Boots Alliance's P/S seems about right to us given the knowledge that analysts are forecasting a revenue outlook that is similar to the Consumer Retailing industry. Right now shareholders are comfortable with the P/S as they are quite confident future revenue won't throw up any surprises. Unless these conditions change, they will continue to support the share price at these levels.

You should always think about risks. Case in point, we've spotted 1 warning sign for Walgreens Boots Alliance you should be aware of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Walgreens Boots Alliance might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:WBA

Walgreens Boots Alliance

Operates as a healthcare, pharmacy, and retail company in the United States, Germany, the United Kingdom, and internationally.

Undervalued with moderate growth potential.