Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:SHBI

Discovering US Undiscovered Gems in November 2025

Simply Wall St

Reviewed by Simply Wall St

In recent weeks, the U.S. stock market has experienced heightened volatility, with significant pressure on tech stocks leading to notable declines in major indices like the Nasdaq and S&P 500. Amid these fluctuations, small-cap stocks often present unique opportunities for investors seeking growth potential outside of heavily scrutinized sectors. Identifying promising small-cap stocks involves looking beyond immediate market trends to find companies with strong fundamentals and innovative business models that may thrive despite broader economic uncertainties.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Tri-County Financial Group | 102.20% | -2.69% | -15.63% | ★★★★★★ |

| Morris State Bancshares | 1.99% | 3.81% | 3.17% | ★★★★★★ |

| Oakworth Capital | 40.91% | 15.96% | 11.47% | ★★★★★★ |

| Franklin Financial Services | 142.38% | 5.48% | -4.56% | ★★★★★★ |

| Senstar Technologies | NA | -18.50% | 29.50% | ★★★★★★ |

| First Northern Community Bancorp | NA | 7.79% | 11.96% | ★★★★★★ |

| Valhi | 44.30% | 1.10% | -1.40% | ★★★★★☆ |

| ASA Gold and Precious Metals | NA | 13.18% | 16.77% | ★★★★★☆ |

| Pure Cycle | 5.02% | 4.35% | -2.25% | ★★★★★☆ |

| Gulf Island Fabrication | 20.48% | 3.25% | 43.31% | ★★★★★☆ |

Let's explore several standout options from the results in the screener.

Great Southern Bancorp (GSBC)

Simply Wall St Value Rating: ★★★★★★

Overview: Great Southern Bancorp, Inc. is a bank holding company for Great Southern Bank, offering a variety of financial services in the United States with a market cap of $648.69 million.

Operations: Great Southern Bancorp generates revenue primarily from its banking operations, totaling $225.98 million.

Great Southern Bancorp, with total assets of US$5.7 billion and equity of US$632.9 million, stands out for its conservative risk management and high-quality earnings despite facing increased competition from fintechs. It holds a net interest margin of 3.4% and maintains a robust allowance for bad loans at 0.04% of total loans, ensuring stability against potential credit losses. The company recently repurchased shares worth US$54.2 million, indicating confidence in its valuation while trading at a slight premium to the current share price of US$63.28 suggests fair valuation amid projected revenue pressures over the next few years.

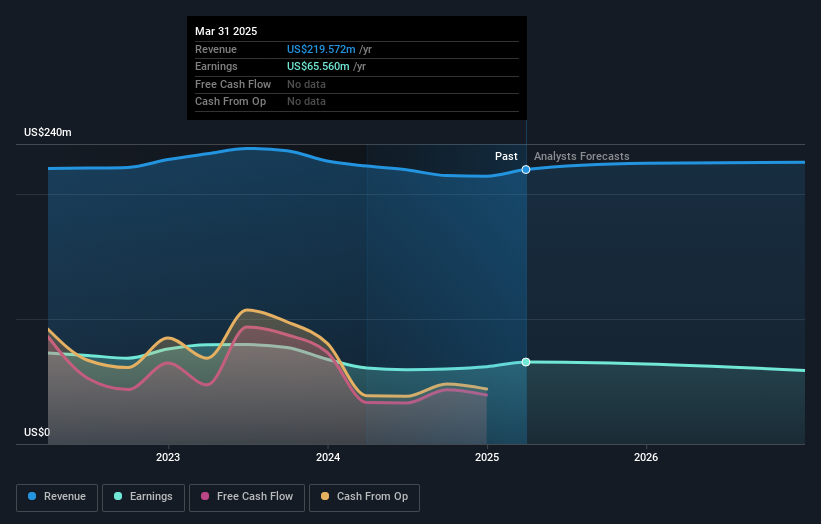

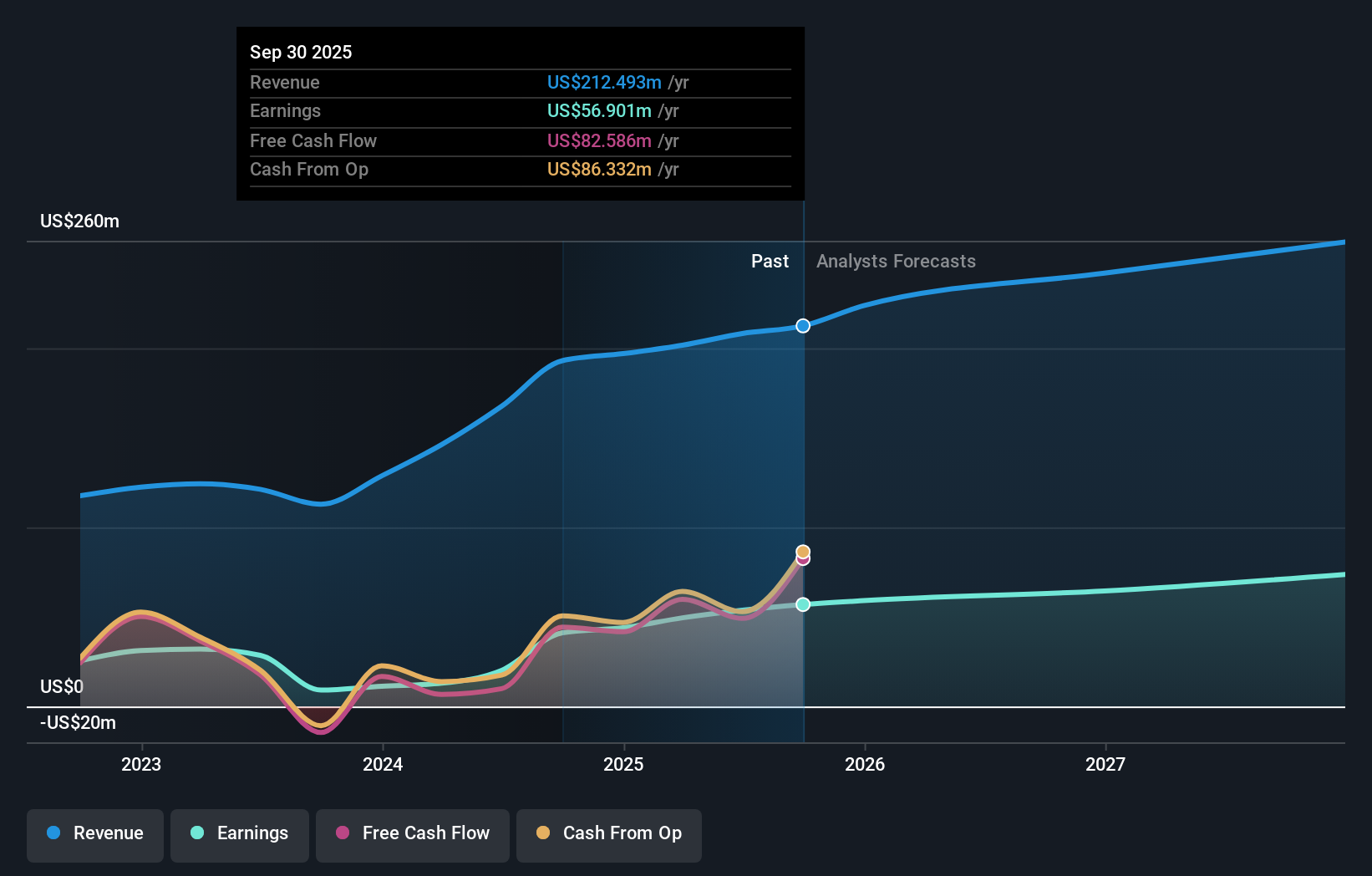

Shore Bancshares (SHBI)

Simply Wall St Value Rating: ★★★★★★

Overview: Shore Bancshares, Inc. is a bank holding company for Shore United Bank, N.A., with a market capitalization of $541.51 million.

Operations: Shore Bancshares generates revenue primarily through its community banking segment, which accounts for $212.49 million. The company has a market capitalization of $541.51 million.

With total assets of US$6.3 billion and equity of US$577.2 million, Shore Bancshares showcases a robust financial position. Total deposits stand at US$5.5 billion against loans totaling US$4.8 billion, reflecting a sound balance sheet structure with a net interest margin of 3.1%. The company boasts an impressive earnings growth rate of 38.5% over the past year, outpacing the industry average of 17.9%. Trading at a price-to-earnings ratio of 9.4x, it offers attractive value compared to the broader market's 18.2x multiple, while maintaining sufficient allowance for bad loans at just 0.5% of total loans.

- Click here to discover the nuances of Shore Bancshares with our detailed analytical health report.

Understand Shore Bancshares' track record by examining our Past report.

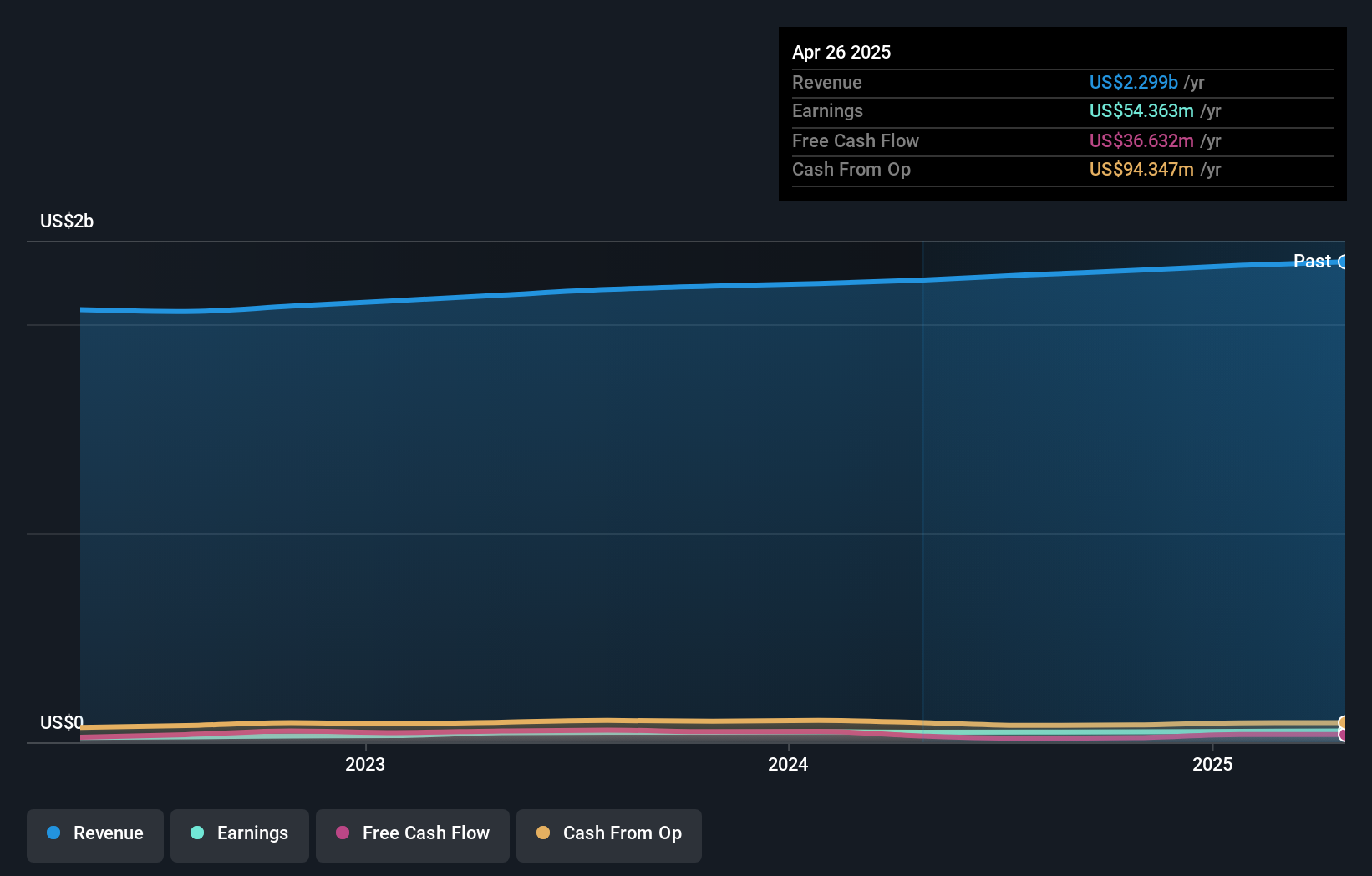

Village Super Market (VLGE.A)

Simply Wall St Value Rating: ★★★★★☆

Overview: Village Super Market, Inc. operates a chain of supermarkets in the United States and has a market cap of approximately $487.93 million.

Operations: Village Super Market generates revenue primarily through the retail sale of food and nonfood products, amounting to $2.32 billion.

Village Super Market has been making strides with a notable 12.2% earnings growth over the past year, outpacing the Consumer Retailing industry's 7.4%. The company’s debt to equity ratio improved from 24.9% to 12% over five years, indicating prudent financial management. Its price-to-earnings ratio of 8.8x is attractive compared to the US market's average of 18.2x, suggesting potential value for investors. Recent earnings showed sales at US$599 million and net income at US$15 million for Q4, slightly up from last year’s figures, while cash dividends were affirmed at $0.25 per Class A share and $0.1625 per Class B share.

Key Takeaways

- Embark on your investment journey to our 303 US Undiscovered Gems With Strong Fundamentals selection here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:SHBI

Shore Bancshares

Operates as a bank holding company for the Shore United Bank, N.A.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor