Costco Wholesale (COST) caught investor attention this week as its stock moved slightly lower, closing at $922.98. While the shift is modest, some are watching for longer-term trends following mild recent declines.

Costco’s slight dip this week follows a broader trend of cooling momentum, as its 30-day share price return is down 3.35% and gains year-to-date are now just 1.45%. Still, the company’s long-term performance remains impressive, with a 2.28% total shareholder return over the past year and a remarkable 162.66% gain over five years. This reminds investors why it is often viewed as a reliable name through market cycles.

With Costco’s latest pullback and robust long-term track record, the big question now is whether the recent drop leaves shares undervalued, or if expectations for future growth are already reflected in the current price?

Advertisement

Most Popular Narrative: 12.9% Undervalued

Costco’s most widely followed narrative puts fair value well above its last close, hinting that the market may still be underestimating future upside. This perspective contrasts strong operational execution with a premium price tag and draws from a broad analyst consensus.

Costco plans to continue expanding its warehouse locations, with 28 new openings planned for fiscal year 2025. This expansion is likely to increase membership and sales volume, driving revenue growth.

Want to know the growth blueprint behind this high valuation? The key element of this narrative is record-breaking earnings and a future profit multiple usually associated with tech leaders. Interested in which bold financial projections support that price target? Dive deeper to see the surprising numbers that drive this fair value calculation.

However, rising labor costs or unfavorable currency movements could squeeze Costco’s margins and challenge the prevailing bullish narrative in the future.

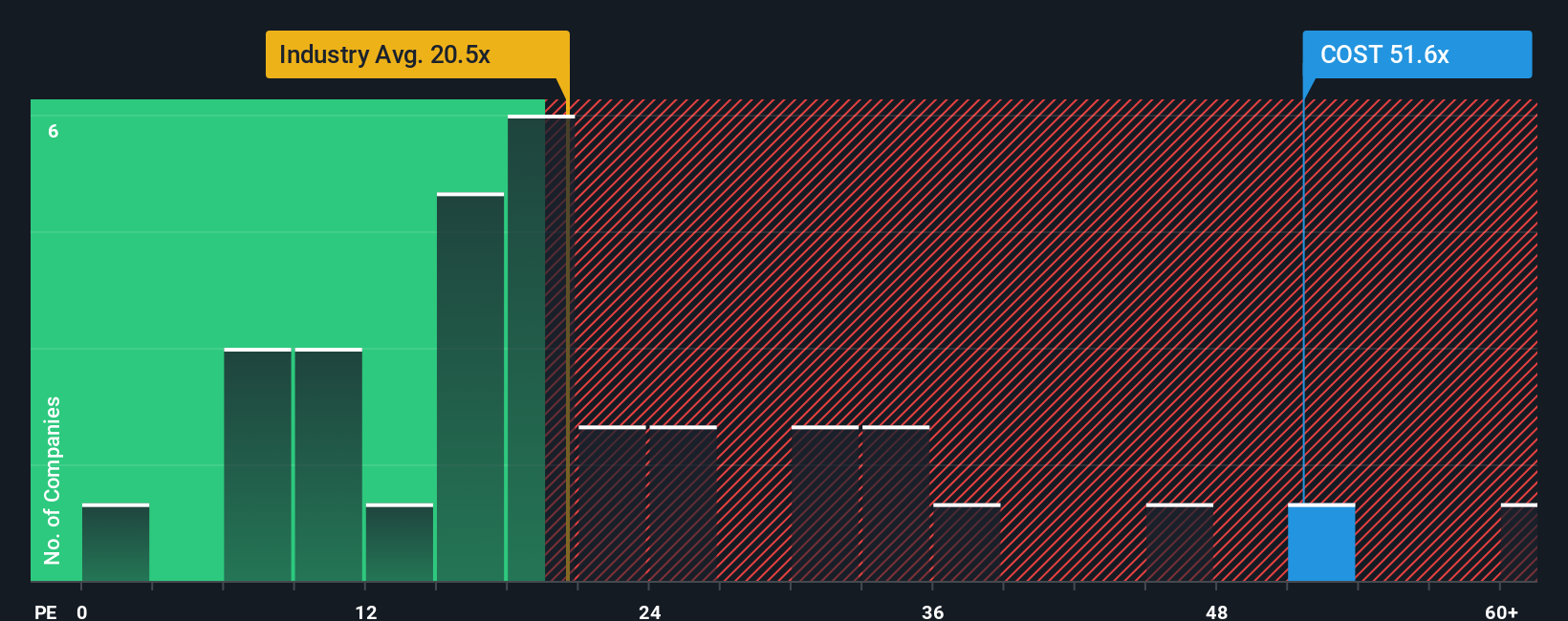

Looking at Costco’s price-to-earnings ratio offers a different angle. Shares trade at 50.5 times earnings, which is much higher than both the consumer retail industry average of 19.8x and the peer average of 22.4x. The fair ratio, calculated at 33.3x, suggests Costco is currently expensive by this metric. This large gap hints at increased valuation risk if market sentiment cools. Can these premium expectations truly last?

Prefer to see things for yourself or have a different perspective? You can dig into the figures and shape your own narrative in under three minutes. Just Do it your way.

A great starting point for your Costco Wholesale research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for Your Next Great Investment?

Don’t let opportunity pass you by. Tap into powerful, tailored stock ideas beyond Costco. With these smart screens, you could uncover tomorrow’s outperformers today.

Spot hidden gems gaining momentum and strong backing by exploring these 3592 penny stocks with strong financials for businesses with impressive financial strength in a fast-moving market.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies

Engages in the operation of membership warehouses in the United States, Puerto Rico, Canada, Mexico, Japan, the United Kingdom, Korea, Australia, Taiwan, China, Spain, France, Iceland, New Zealand, and Sweden.