Advertisement

- United States

- /

- Luxury

- /

- NYSE:TPR

Is Tapestry’s (TPR) $800M Buyback a Signal of Stronger Brand Momentum or Cautious Optimism?

Simply Wall St

Reviewed by Sasha Jovanovic

- On September 16, 2025, Tapestry, Inc. board member John P. (JP) Bilbrey informed the company that he would not stand for re-election at the upcoming November annual meeting, with no disagreements involved, and will continue serving until then.

- This development coincided with Tapestry reporting record fiscal 2025 results, highlighting both robust growth at Coach and increased adoption among Gen Z and millennial consumers, while the company announced plans for an US$800-million share repurchase and a 14% dividend increase.

- We'll explore how Tapestry's record results and enhanced shareholder returns shape its current investment narrative and future outlook.

We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Tapestry Investment Narrative Recap

To see value in Tapestry as a shareholder, you need conviction in Coach’s staying power, the company’s ability to capture younger customers globally, and confidence that recent one-off setbacks at Kate Spade and ongoing tariff headwinds won’t outweigh the momentum elsewhere in the portfolio. The announcement that board member John P. (JP) Bilbrey will not stand for re-election is not expected to influence key short-term catalysts, such as Coach’s growth and international expansion, or meaningfully affect the most pressing risk, which remains the underperformance and margin drag at Kate Spade.

Of several recent company actions, the US$800 million share repurchase stands out as particularly relevant. While board transitions typically have little direct effect on capital allocation, this buyback program reinforces management’s confidence in the business’s outlook and underpins current efforts to boost shareholder returns despite ongoing brand turnaround challenges at Kate Spade and persistent headwinds from tariffs.

Yet in contrast to recent dividend and buyback announcements, investors should be aware of the potential long tail of impairment charges and losses at Kate Spade if turnaround efforts...

Read the full narrative on Tapestry (it's free!)

Tapestry's narrative projects $7.8 billion revenue and $1.4 billion earnings by 2028. This requires 3.6% yearly revenue growth and a $1.2 billion increase in earnings from $183.2 million currently.

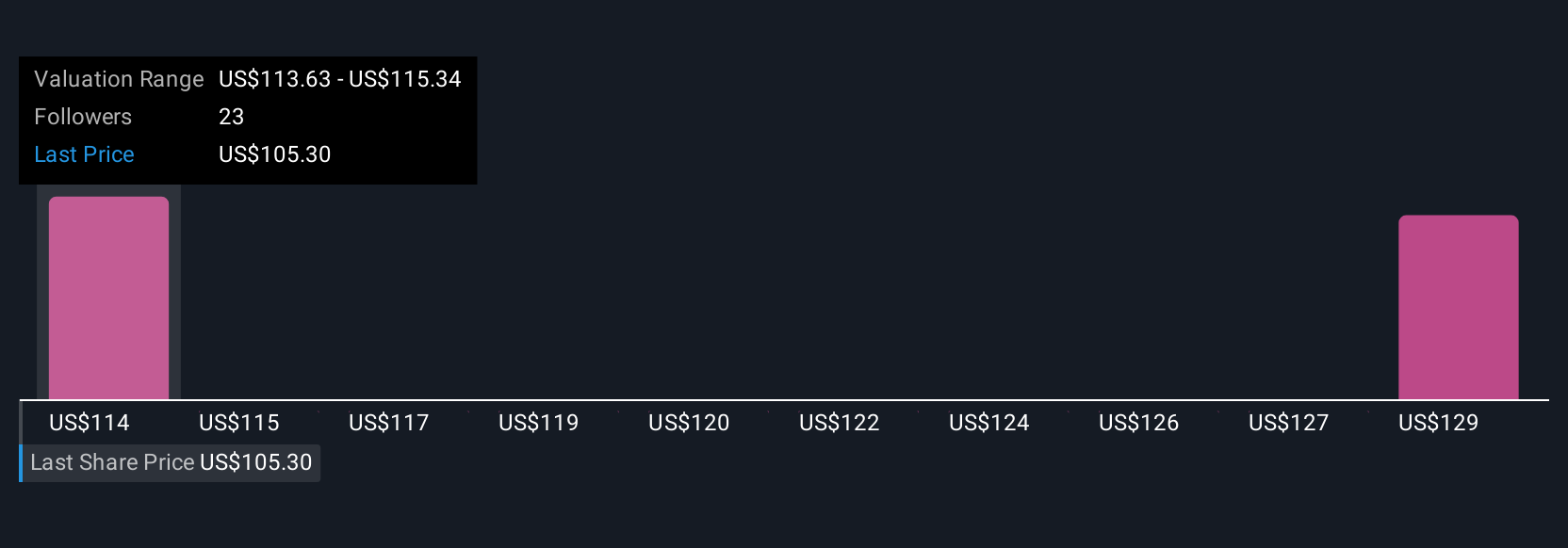

Uncover how Tapestry's forecasts yield a $116.44 fair value, in line with its current price.

Exploring Other Perspectives

Three fair value estimates from the Simply Wall St Community range between US$113.63 and US$128.93 per share. Many see upside potential, but sluggish revenue growth and risks at Kate Spade continue to spark debate on the company’s long-term performance.

Explore 3 other fair value estimates on Tapestry - why the stock might be worth as much as 12% more than the current price!

Build Your Own Tapestry Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Tapestry research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Tapestry research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Tapestry's overall financial health at a glance.

Interested In Other Possibilities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Rare earth metals are the new gold rush. Find out which 33 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Tapestry might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TPR

Tapestry

Provides accessories and lifestyle brand products in North America, Greater China, rest of Asia, and internationally.

Reasonable growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor