Advertisement

- United States

- /

- Luxury

- /

- NYSE:KTB

How Upgraded Revenue Guidance and Helly Hansen Boost at Kontoor Brands (KTB) Has Changed Its Investment Story

Simply Wall St

Reviewed by Sasha Jovanovic

- Kontoor Brands recently announced its third quarter results, reporting sales of US$853.22 million and raising its full-year 2025 revenue guidance to the high end of its previous outlook, with a strong contribution from the Helly Hansen acquisition.

- Despite a decrease in net income compared to the prior year, the company has highlighted continuing momentum in revenue, particularly with an upgraded fourth quarter outlook and targeted growth in key segments such as direct-to-consumer and international channels.

- We'll examine how Kontoor Brands' upgraded full-year revenue guidance and strong Q4 outlook interact with its longer-term investment narrative.

Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

Kontoor Brands Investment Narrative Recap

To own Kontoor Brands, investors need to be confident that legacy brands like Wrangler and Lee can maintain relevance while Helly Hansen’s integration unlocks new growth, despite recent Q3 earnings showing higher revenue but lower net income, the upgraded guidance suggests a focus on topline expansion as the short-term catalyst. For now, the raised revenue outlook meaningfully improves visibility into fourth quarter strength, but input cost pressures and Helly Hansen execution remain the largest risks; this news does not materially reduce those threats.

Of the recent announcements, the update to full-year and fourth quarter guidance stands out, providing investors with a better sense of near-term revenue momentum, especially when excluding Helly Hansen, where underlying growth remains modest. This links closely to the current investment thesis that hinges on successful brand diversification and channel expansion, making continued revenue momentum critical to offsetting risks from fashion cycles and cost pressures.

Yet the potential impact from rising input costs and persistent margin pressures is an important area investors should not overlook, especially as...

Read the full narrative on Kontoor Brands (it's free!)

Kontoor Brands' narrative projects $3.9 billion revenue and $364.9 million earnings by 2028. This requires 13.5% yearly revenue growth and a $113.6 million earnings increase from $251.3 million.

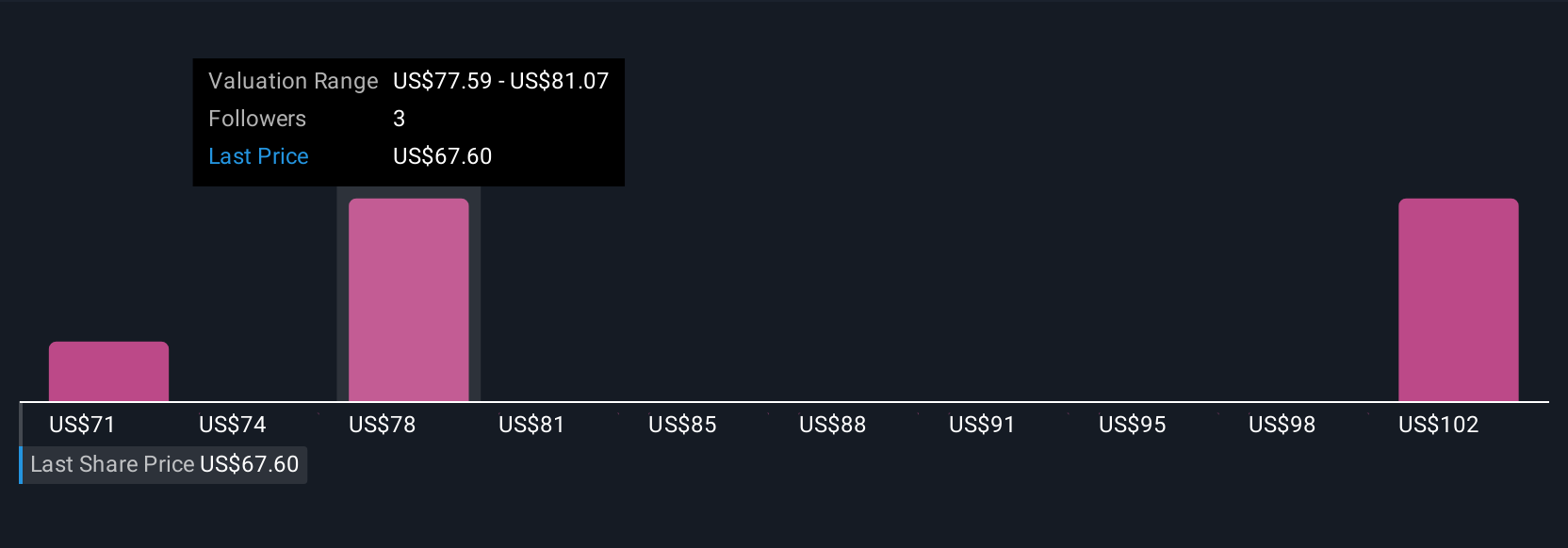

Uncover how Kontoor Brands' forecasts yield a $91.50 fair value, a 27% upside to its current price.

Exploring Other Perspectives

Four fair value estimates from the Simply Wall St Community span a wide US$49 to US$93, reflecting diverse outlooks on Kontoor Brands' prospects. Opinions differ, particularly as integration and cost management stay central to future performance.

Explore 4 other fair value estimates on Kontoor Brands - why the stock might be worth as much as 30% more than the current price!

Build Your Own Kontoor Brands Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Kontoor Brands research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Kontoor Brands research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Kontoor Brands' overall financial health at a glance.

Looking For Alternative Opportunities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kontoor Brands might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:KTB

Kontoor Brands

A lifestyle apparel company, designs, produces, procures, markets, distributes, and licenses denim, apparel, footwear, and accessories, primarily under the Wrangler and Lee brands.

Undervalued with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor