Advertisement

- United States

- /

- Consumer Durables

- /

- NYSE:ETD

US$24.00 - That's What Analysts Think Ethan Allen Interiors Inc. (NYSE:ETH) Is Worth After These Results

Shareholders might have noticed that Ethan Allen Interiors Inc. (NYSE:ETH) filed its quarterly result this time last week. The early response was not positive, with shares down 2.5% to US$23.65 in the past week. Ethan Allen Interiors reported in line with analyst predictions, delivering revenues of US$179m and statutory earnings per share of US$0.67, suggesting the business is executing well and in line with its plan. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

See our latest analysis for Ethan Allen Interiors

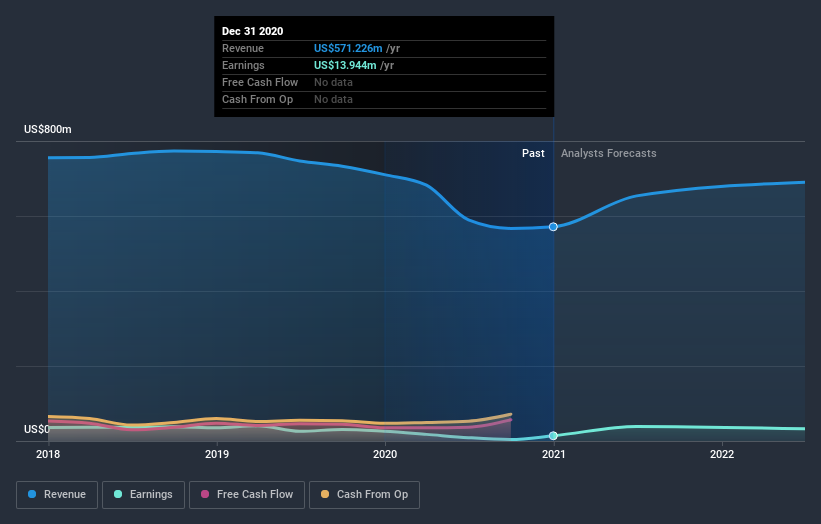

Taking into account the latest results, the consensus forecast from Ethan Allen Interiors' twin analysts is for revenues of US$653.7m in 2021, which would reflect a decent 14% improvement in sales compared to the last 12 months. Statutory earnings per share are predicted to soar 180% to US$1.56. Before this earnings report, the analysts had been forecasting revenues of US$653.7m and earnings per share (EPS) of US$1.56 in 2021. The consensus analysts don't seem to have seen anything in these results that would have changed their view on the business, given there's been no major change to their estimates.

The consensus price target rose 26% to US$24.00despite there being no meaningful change to earnings estimates. It could be that the analystsare reflecting the predictability of Ethan Allen Interiors' earnings by assigning a price premium.

Of course, another way to look at these forecasts is to place them into context against the industry itself. For example, we noticed that Ethan Allen Interiors' rate of growth is expected to accelerate meaningfully, with revenues forecast to grow 14%, well above its historical decline of 4.9% a year over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in the industry are forecast to see their revenue grow 8.9% per year. Not only are Ethan Allen Interiors' revenues expected to improve, it seems that the analysts are also expecting it to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with the analysts reconfirming that the business is performing in line with their previous earnings per share estimates. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

With that in mind, we wouldn't be too quick to come to a conclusion on Ethan Allen Interiors. Long-term earnings power is much more important than next year's profits. At least one analyst has provided forecasts out to 2022, which can be seen for free on our platform here.

Don't forget that there may still be risks. For instance, we've identified 4 warning signs for Ethan Allen Interiors that you should be aware of.

If you decide to trade Ethan Allen Interiors, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Ethan Allen Interiors might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NYSE:ETD

Ethan Allen Interiors

Operates as an interior design company, and manufacturer and retailer of home furnishings in the United States and internationally.

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|40.2% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|62.7% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.1% undervalued

UN

Community Contributor