Advertisement

- United States

- /

- Consumer Durables

- /

- NYSE:BLD

Examining TopBuild’s 47% Surge in 2025 Amid Acquisition Activity and Analyst Valuations

Simply Wall St

Reviewed by Bailey Pemberton

- Curious if TopBuild is a hidden gem or just riding the wave? Let’s dig into what is really behind its current share price.

- This year has been impressive so far, with the stock up 46.7% year-to-date and gaining 16.5% over the past year. Investors are clearly paying attention.

- Sentiment has been fueled by sector-wide interest in building and home improvement, especially following policy changes that have highlighted the importance of strong supply chains and reliable contractors. TopBuild’s acquisition activity and growing footprint have also made headlines, helping to keep the stock in the news and shaping its recent moves.

- If you are looking for a straightforward metric, TopBuild’s current valuation score is 0 out of 6, meaning it is not undervalued on any of our six major checks. However, there is more to valuation than checklists, and we will be diving into a few approaches before sharing an even smarter way to gauge the real opportunity here.

TopBuild scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: TopBuild Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by forecasting its future cash flows and discounting them to their present value. This approach attempts to capture the earning power of the business by projecting Free Cash Flow (FCF) over time and adjusting for the value of money today.

TopBuild currently generates Free Cash Flow of approximately $780.6 million. According to analyst estimates and subsequent extrapolation, its FCF is expected to grow gradually, reaching around $907 million by 2035. For context, analyst consensus covers up to 2027, after which these projections are extended based on current growth rates.

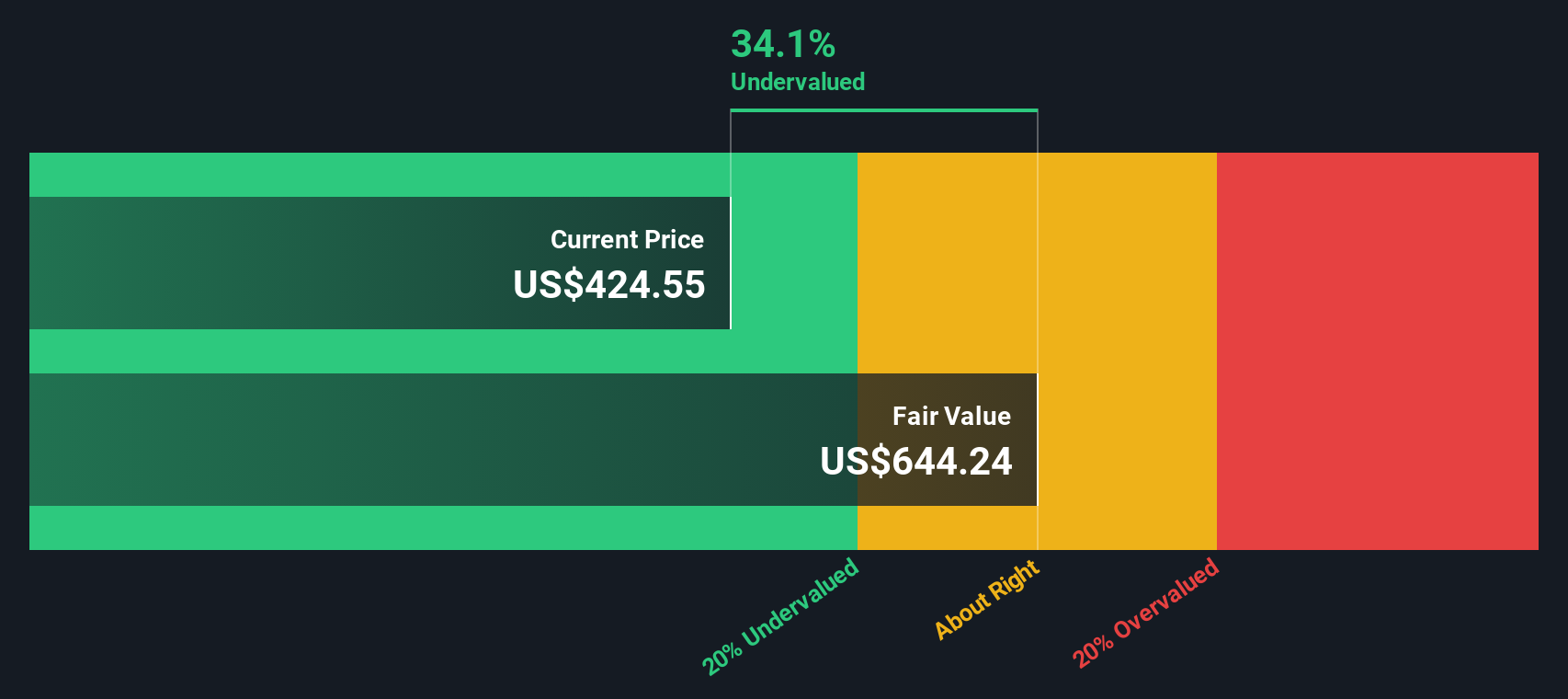

Using the DCF method with these projections, the model estimates that TopBuild's intrinsic fair value is $422.21 per share. With the stock trading at about 7.8% above this estimated intrinsic value, TopBuild appears slightly overvalued by this metric. However, the difference is not extreme and the market price is fairly close to what can be justified by projected cash flows.

Result: ABOUT RIGHT

TopBuild is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: TopBuild Price vs Earnings (PE Ratio Analysis)

The Price-to-Earnings (PE) ratio is a widely trusted metric for valuing profitable, established companies like TopBuild. It allows investors to quickly gauge how much they are paying for each dollar of reported earnings, making it an effective tool for comparing companies within the same sector or across the market.

What is considered a “normal” or “fair” PE ratio, however, is not set in stone. Factors such as a company’s projected growth, profitability, and risk profile all play a part. A company with higher growth prospects or lower perceived risk typically commands a higher PE, while cyclical risk or slower growth can mean a lower deserved multiple.

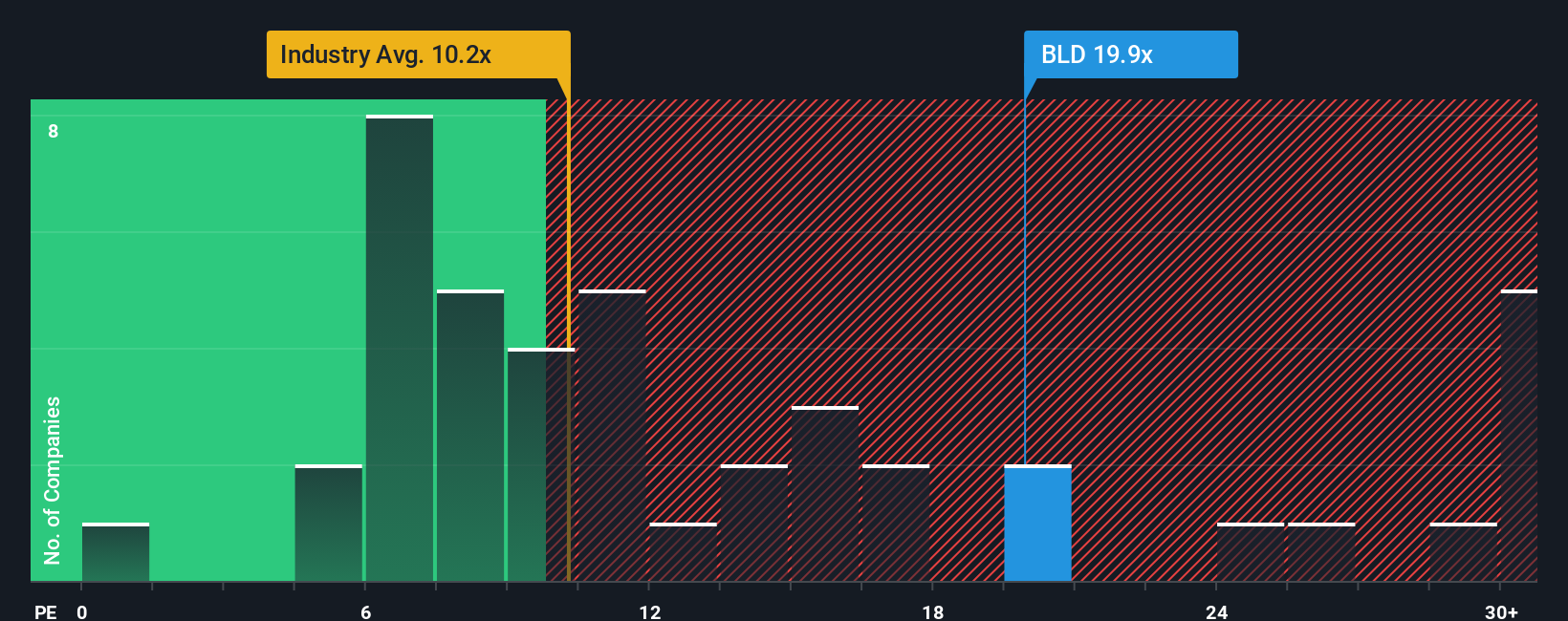

TopBuild is currently trading on a PE ratio of 22.4x. This stands well above the Consumer Durables industry average of 11.8x and also above the peer average of 15.7x. However, Simply Wall St’s proprietary “Fair Ratio,” which reflects adjusted expectations based on TopBuild’s earnings growth, profit margins, risk, industry, and size, sits at 16.0x. This tailored benchmark is a more insightful guide than simple peer or industry comparisons as it better captures the nuance of the company’s unique fundamentals.

Comparing TopBuild’s current PE ratio of 22.4x to its Fair Ratio of 16.0x, there is a notable premium. This suggests that based on the best available data and a well-rounded adjustment for growth and risk, TopBuild shares look somewhat overvalued by this approach.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1441 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your TopBuild Narrative

Earlier we mentioned there's an even better way to understand valuation. Let's introduce you to Narratives. A Narrative is your personal story or perspective on a company, providing a way to link your understanding of TopBuild’s business, industry tailwinds, and risks directly to a financial forecast and a calculated fair value. On Simply Wall St’s Community page, Narratives let you quickly turn your own assumptions about future revenue, profit margins, and market trends into a visual forecast and see how your belief compares to other investors and the current market price.

Narratives are designed to be accessible and are used by millions of investors on our platform. They simplify the process of fair value estimation and help you act confidently. When news breaks or earnings reports are released, Narratives update automatically, reflecting the latest facts and market reactions right away. This allows you or anyone following TopBuild to adjust your buy or sell decision based on a live comparison between Fair Value and the actual share price.

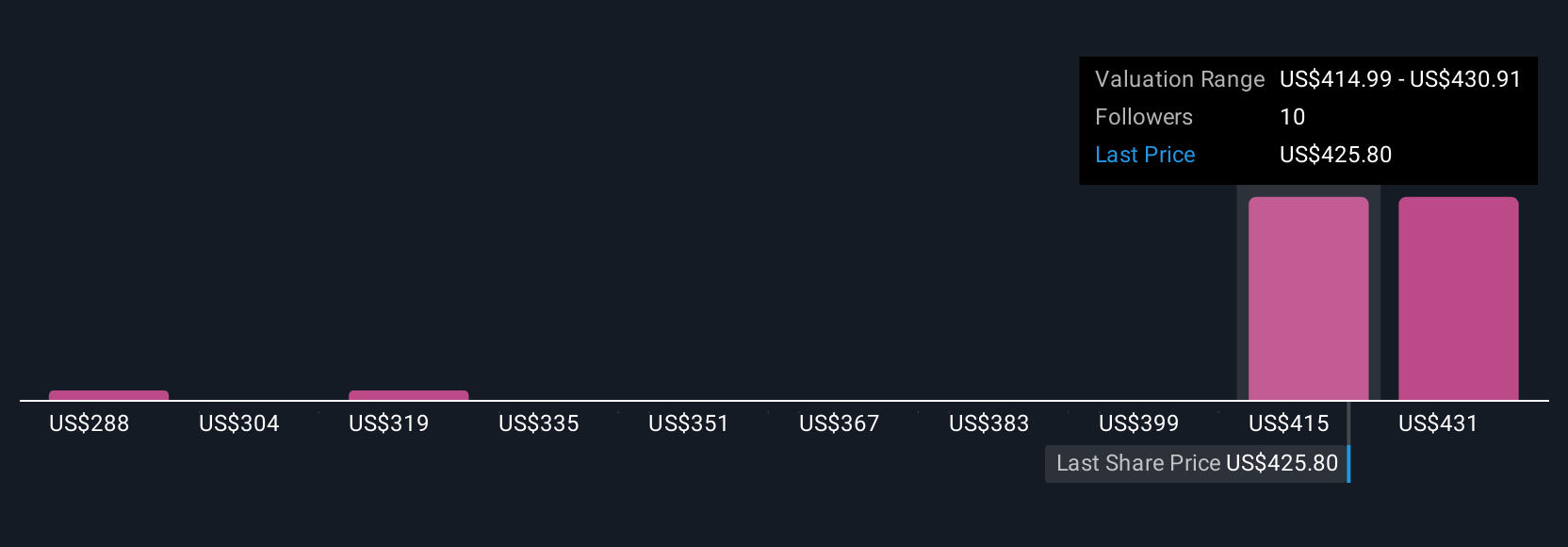

For example, right now the highest published analyst Narrative for TopBuild sets a fair value at $487 per share, while the lowest is at $370. This illustrates how different assumptions about growth, margins, and industry risks lead investors to agree or disagree on whether TopBuild is a bargain or overhyped.

Do you think there's more to the story for TopBuild? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TopBuild might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BLD

TopBuild

Engages in the installation and distribution of insulation and other building material products to the construction industry.

Mediocre balance sheet with limited growth.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

102 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative