Advertisement

- United States

- /

- Luxury

- /

- NasdaqGM:PLBY

These Analysts Just Made An Incredible Downgrade To Their PLBY Group, Inc. (NASDAQ:PLBY) EPS Forecasts

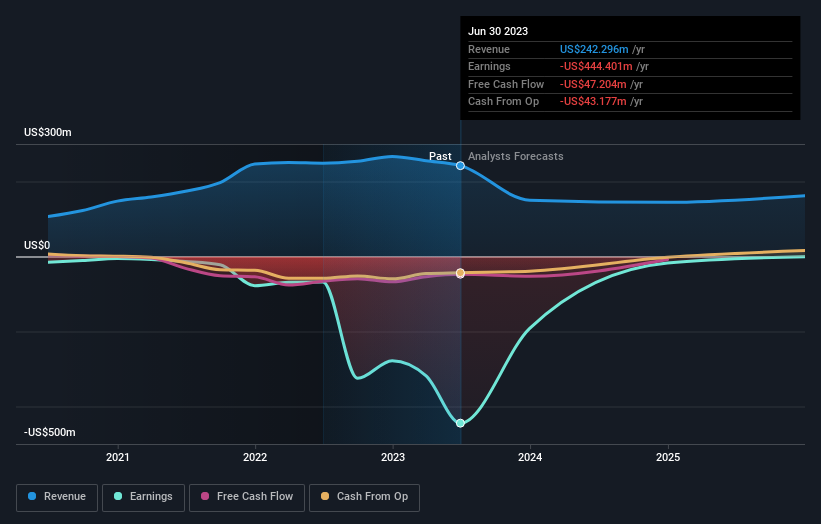

The analysts covering PLBY Group, Inc. (NASDAQ:PLBY) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for this year. Revenue and earnings per share (EPS) forecasts were both revised downwards, with analysts seeing grey clouds on the horizon.

Following the latest downgrade, the six analysts covering PLBY Group provided consensus estimates of US$150m revenue in 2023, which would reflect a painful 38% decline on its sales over the past 12 months. Losses are predicted to fall substantially, shrinking 56% to US$2.68 per share. Yet before this consensus update, the analysts had been forecasting revenues of US$200m and losses of US$0.90 per share in 2023. So there's been quite a change-up of views after the recent consensus updates, with the analysts making a serious cut to their revenue forecasts while also expecting losses per share to increase.

See our latest analysis for PLBY Group

The consensus price target fell 7.2% to US$3.23, implicitly signalling that lower earnings per share are a leading indicator for PLBY Group's valuation.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 62% by the end of 2023. This indicates a significant reduction from annual growth of 26% over the last three years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 7.7% per year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - PLBY Group is expected to lag the wider industry.

The Bottom Line

The most important thing to note from this downgrade is that the consensus increased its forecast losses this year, suggesting all may not be well at PLBY Group. Unfortunately analysts also downgraded their revenue estimates, and industry data suggests that PLBY Group's revenues are expected to grow slower than the wider market. With a serious cut to this year's expectations and a falling price target, we wouldn't be surprised if investors were becoming wary of PLBY Group.

As you can see, the analysts clearly aren't bullish, and there might be good reason for that. We've identified some potential issues with PLBY Group's financials, such as major dilution from new stock issuance in the past year. Learn more, and discover the 3 other risks we've identified, for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:PLBY

Playboy

PLBY Group, Inc. operates as a pleasure and leisure company in the United States, Australia, China, the United Kingdom, and internationally.

Slight and overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor