Advertisement

- United States

- /

- Luxury

- /

- NasdaqGS:LULU

Is lululemon Attractive After a 50% Share Price Slide and DCF Upside?

Simply Wall St

Reviewed by Bailey Pemberton

- If you are wondering whether lululemon athletica is finally starting to look like a bargain after its big slide, or if the market still has it right, this breakdown is for you.

- The stock is trading around $183.6, up 9.6% over the last month but still down 50.7% year to date and 54.1% over the past year. That tells you sentiment has shifted significantly, even as short-term buyers are beginning to step back in.

- Recent headlines have focused on questions about whether athleisure demand is normalizing and how competitive pressure from both premium and mass market brands could reshape lululemon's growth runway. At the same time, the company continues to invest in product innovation and international expansion, which the market is trying to reprice against those competitive and consumer headwinds.

- On our framework, lululemon currently earns a 5/6 valuation score, suggesting it screens as undervalued on most but not all of our checks. Next, we will walk through what different valuation methods indicate about that score, before finishing with a more intuitive way to think about what the stock may be worth.

Find out why lululemon athletica's -54.1% return over the last year is lagging behind its peers.

Approach 1: lululemon athletica Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth by projecting the cash it can generate in the future and then discounting those cash flows back to today in $ terms.

For lululemon athletica, the latest twelve month Free Cash Flow is about $1.16 billion. Analysts and internal estimates see this rising steadily, with projections pointing to roughly $1.60 billion of Free Cash Flow by 2030, based on a two stage Free Cash Flow to Equity approach. Near term forecasts rely on analyst estimates, while later years are extrapolated by Simply Wall St using gradually slowing growth assumptions.

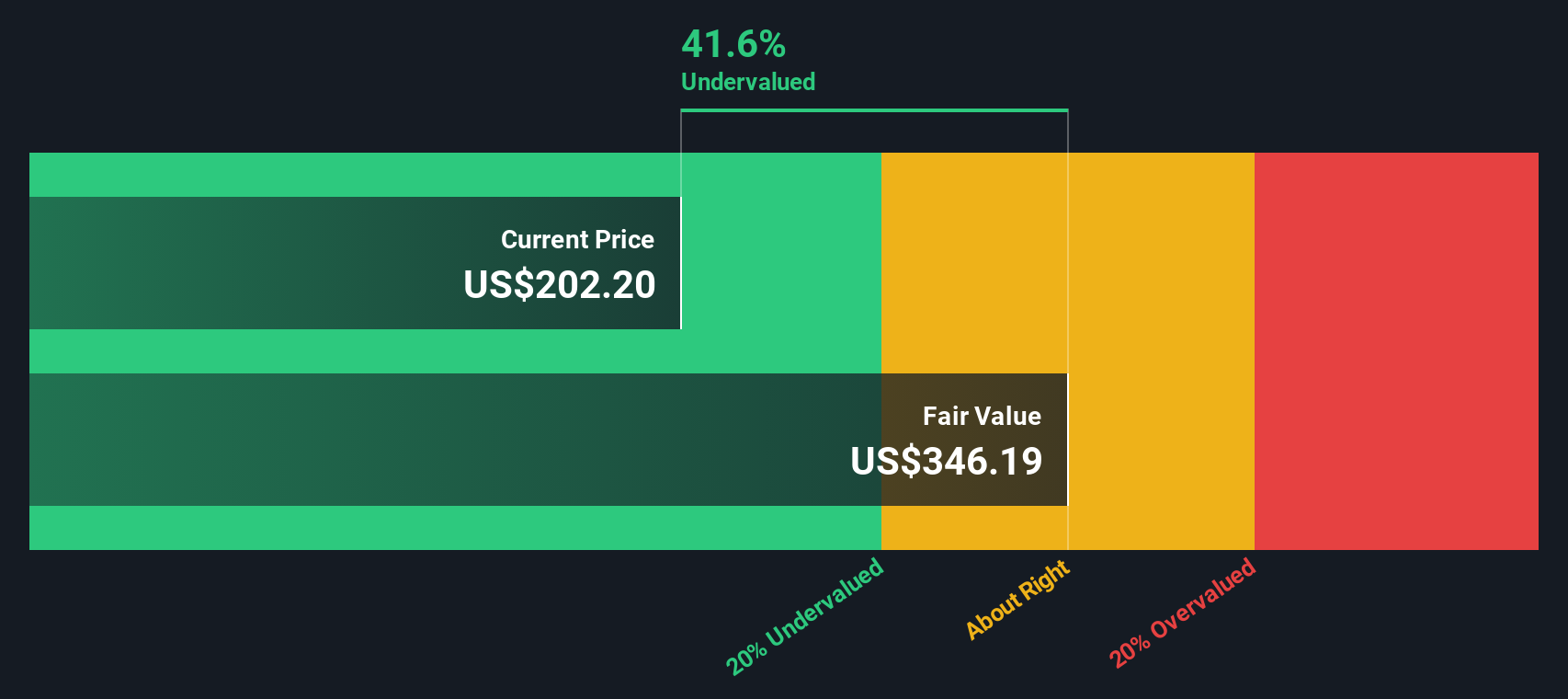

When those future cash flows are discounted back to the present, the model indicates an intrinsic value of about $253 per share. Versus the current share price around $184, the DCF implies the stock is roughly 27.5% undervalued. This suggests the market is pricing in a much weaker long term cash flow profile than this model assumes.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests lululemon athletica is undervalued by 27.5%. Track this in your watchlist or portfolio, or discover 912 more undervalued stocks based on cash flows.

Approach 2: lululemon athletica Price vs Earnings

The Price to Earnings ratio is a useful way to value profitable companies because it directly compares what investors are paying for each dollar of current earnings. In general, faster earnings growth and lower perceived risk justify a higher normal PE, while slower growth, more cyclicality or greater uncertainty typically warrant a lower one.

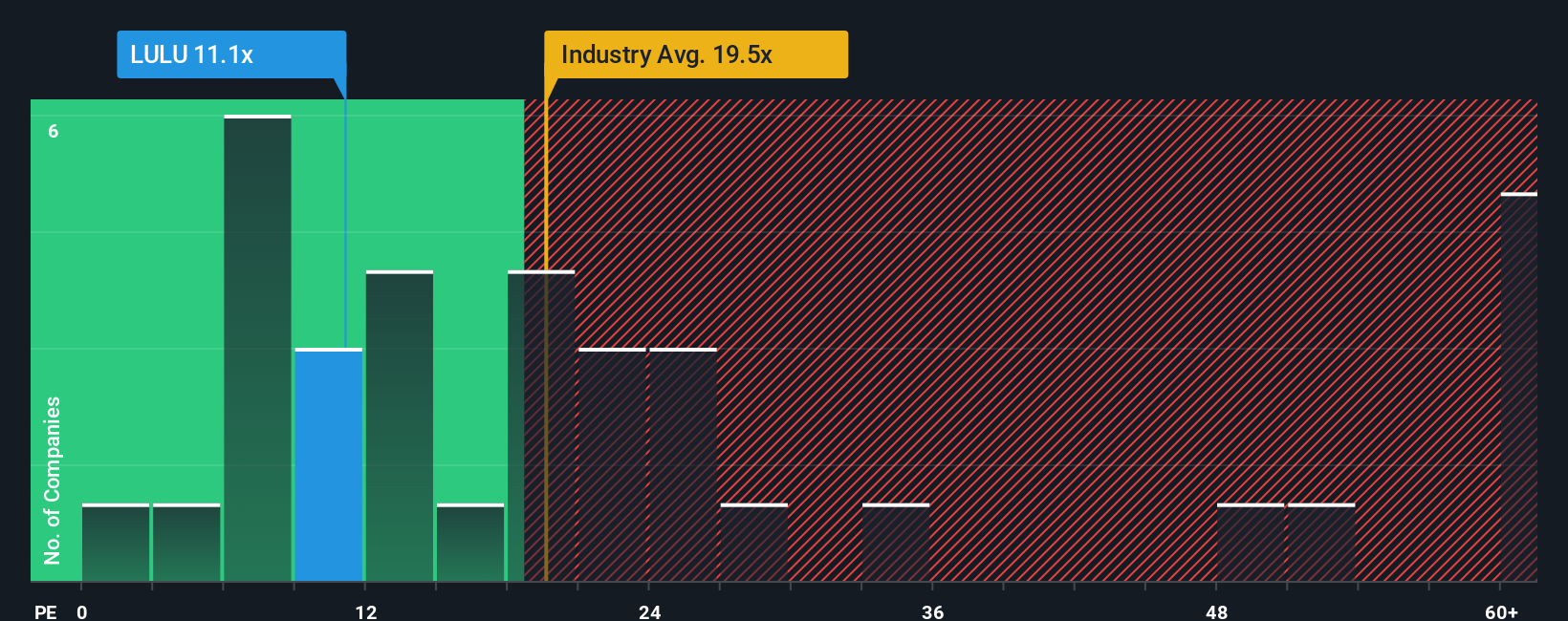

lululemon athletica currently trades on a PE of about 12.2x, which is well below both the Luxury industry average of roughly 21.0x and the broader peer group around 48.2x. On the surface that makes the stock look cheap, but simple comparisons can miss differences in growth prospects, profitability and risk.

To address this, Simply Wall St uses a proprietary Fair Ratio, which estimates what a reasonable PE should be given lululemon's earnings growth outlook, margins, industry, market cap and risk profile. For lululemon, this Fair Ratio is about 17.3x. This is more tailored than a straight peer or industry comparison because it explicitly adjusts for those fundamentals rather than assuming all companies deserve the same multiple.

Comparing the Fair Ratio of 17.3x to the current 12.2x suggests the market is assigning a discount to lululemon's earnings power relative to what its fundamentals might justify.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1440 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your lululemon athletica Narrative

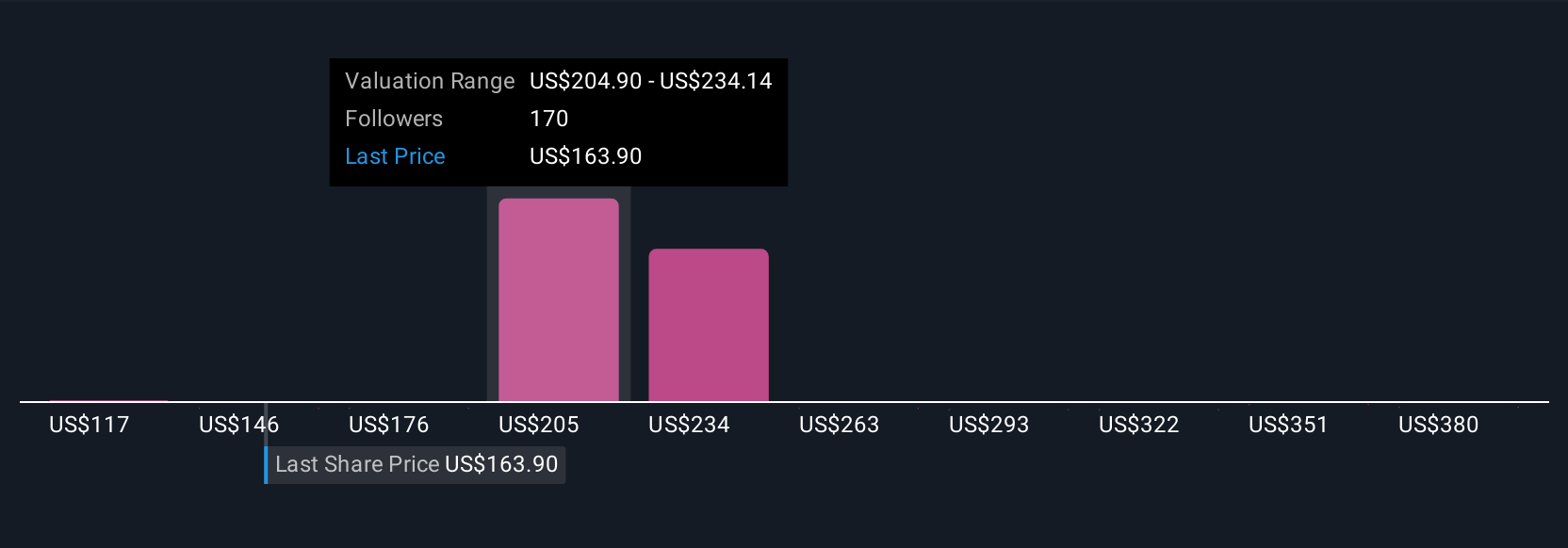

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives, an approach that lets you attach a clear story about lululemon athletica to the numbers you are assuming for its fair value, future revenue, earnings and margins. On Simply Wall St's Community page, Narratives help you link what you believe about the business, for example whether its brand will reaccelerate or stall, to a structured financial forecast and then to a single Fair Value that you can compare with the current share price to decide whether to buy, hold or sell. Because these Narratives are updated dynamically when new information like earnings, guidance changes or major news hits, they stay relevant as the facts change rather than locking you into a stale view. For lululemon athletica, one investor might build a Narrative with higher growth, stronger margins and a Fair Value near $226, while another uses more conservative assumptions and lands closer to $194. Seeing that range side by side can clarify which story you find more convincing and what needs to go right for the stock at today's price.

Do you think there's more to the story for lululemon athletica? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if lululemon athletica might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:LULU

lululemon athletica

Designs, distributes, and retails technical athletic apparel, footwear, and accessories for women and men under the lululemon brand in the United States, Canada, Mexico, China Mainland, Hong Kong, Taiwan, Macau, and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

49 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4729.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6410.8% overvalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.8% undervalued

956 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Alphabet ·

GOOGL: AI Platform Expansion And Cloud Demand Will Support Durable Performance Amid Competitive Pressures

Fair Value:US$323.71.9% undervalued

1342 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative