Advertisement

- United States

- /

- Luxury

- /

- NasdaqGS:LULU

Does Lululemon's (LULU) New Credit Facility Reflect Shifting Priorities in Global Growth Strategy?

Simply Wall St

Reviewed by Sasha Jovanovic

- On October 15, 2025, lululemon athletica and its subsidiaries announced they had entered into a Second Amended and Restated Credit Agreement with a US$600 million unsecured five-year revolving credit facility, with the option to increase commitments up to US$1 billion and maturity set for October 15, 2030.

- This development offers lululemon increased financial flexibility, positioning the company to execute its product revitalization and international growth ambitions while addressing near-term headwinds in its core U.S. market.

- We’ll examine how lululemon’s expanded credit facility could support its planned product innovation and market expansion efforts.

This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

lululemon athletica Investment Narrative Recap

To be a lululemon shareholder, you need confidence in the company’s ability to revitalize its U.S. business through faster product innovation and execute global expansion even as tariffs pressure margins. The recent US$600 million revolving credit facility does offer greater financial flexibility, but its impact on overcoming near-term U.S. demand softness, a key catalyst, is not significant on its own; the biggest risk remains whether new styles can reignite growth before competitive and macro factors drag on margins further.

Among recent company events, lululemon’s guidance revision for 2025 directly relates to this news: the company lowered its revenue and earnings expectations due to weaker U.S. trends and tariff impacts, underscoring how execution on product resets, rather than capital structure alone, is what could move the needle for investors tracking catalysts this year.

Yet, in contrast, investors should also be aware that stalling product innovation poses ongoing risks if new launches fail to resonate with core customers...

Read the full narrative on lululemon athletica (it's free!)

lululemon athletica's narrative projects $12.8 billion revenue and $1.9 billion earnings by 2028. This requires 5.4% yearly revenue growth and a $0.1 billion earnings increase from $1.8 billion currently.

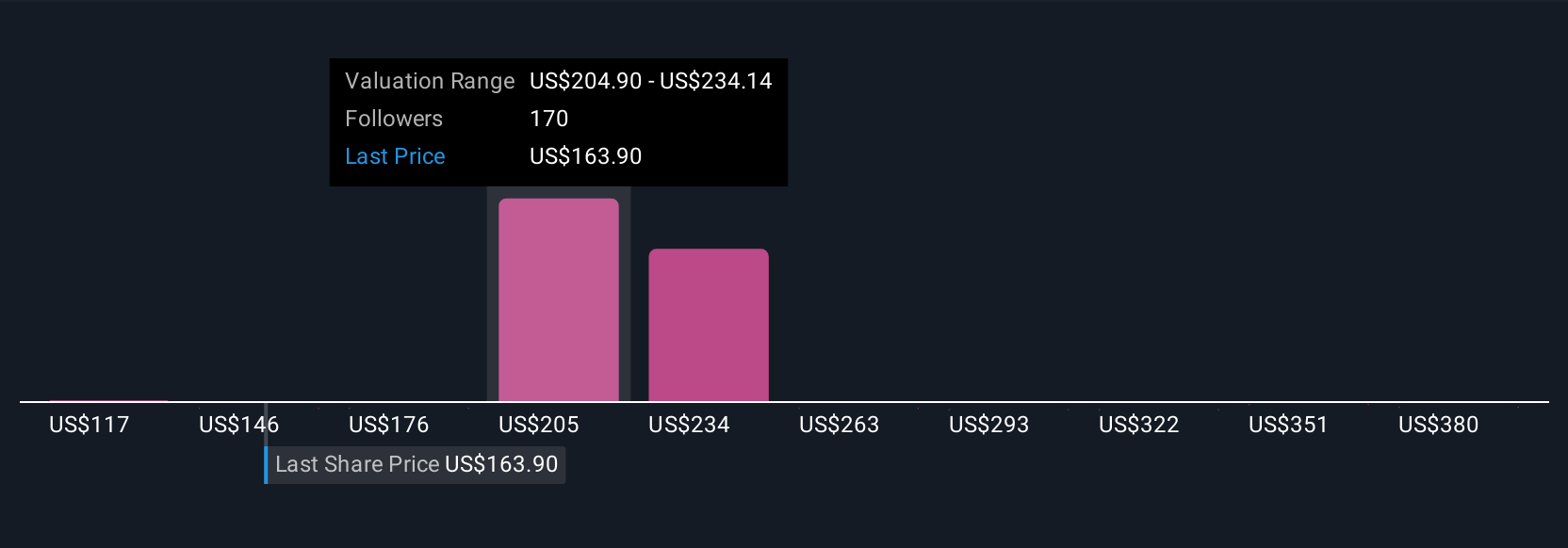

Uncover how lululemon athletica's forecasts yield a $195.84 fair value, a 10% upside to its current price.

Exploring Other Perspectives

The Simply Wall St Community’s 47 fair value estimates for lululemon range widely from US$117 to US$410 per share. With many contributors, opinions differ greatly, and as the U.S. business faces competitive pressures, it is worth considering how such a broad set of expectations could reflect uncertainty in the company’s recovery.

Explore 47 other fair value estimates on lululemon athletica - why the stock might be worth 34% less than the current price!

Build Your Own lululemon athletica Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your lululemon athletica research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free lululemon athletica research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate lululemon athletica's overall financial health at a glance.

Seeking Other Investments?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 36 best rare earth metal stocks of the very few that mine this essential strategic resource.

- We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if lululemon athletica might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:LULU

lululemon athletica

Designs, distributes, and retails technical athletic apparel, footwear, and accessories for women and men under the lululemon brand in the United States, Canada, Mexico, China Mainland, Hong Kong, Taiwan, Macau, and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.5% undervalued

GM

Community Contributor