Advertisement

- United States

- /

- Consumer Durables

- /

- NasdaqGM:LOVE

Should You Be Adding Lovesac (NASDAQ:LOVE) To Your Watchlist Today?

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. A loss-making company is yet to prove itself with profit, and eventually the inflow of external capital may dry up.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like Lovesac (NASDAQ:LOVE). While this doesn't necessarily speak to whether it's undervalued, the profitability of the business is enough to warrant some appreciation - especially if its growing.

View our latest analysis for Lovesac

Lovesac's Improving Profits

Lovesac has undergone a massive growth in earnings per share over the last three years. So much so that this three year growth rate wouldn't be a fair assessment of the company's future. As a result, we'll zoom in on growth over the last year, instead. Lovesac's EPS shot up from US$2.32 to US$2.92; a result that's bound to keep shareholders happy. That's a fantastic gain of 26%.

It's often helpful to take a look at earnings before interest and tax (EBIT) margins, as well as revenue growth, to get another take on the quality of the company's growth. While Lovesac did well to grow revenue over the last year, EBIT margins were dampened at the same time. So if EBIT margins can stabilize, this top-line growth should pay off for shareholders.

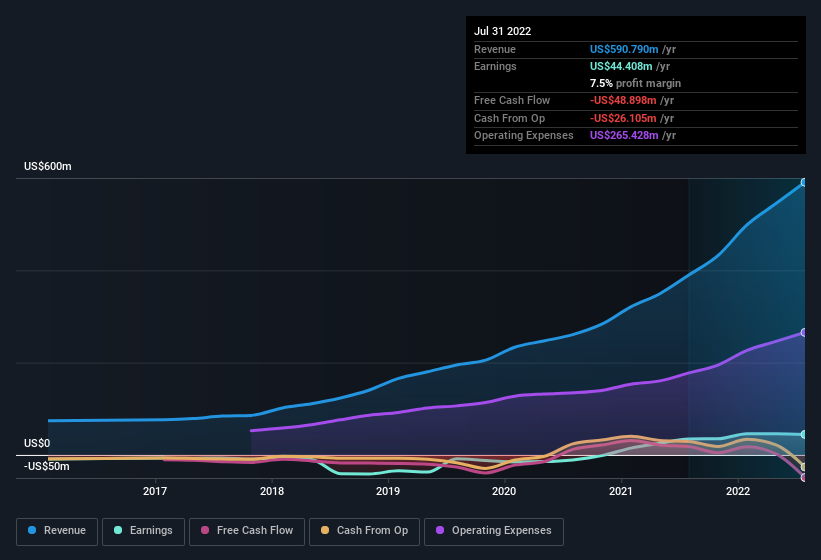

You can take a look at the company's revenue and earnings growth trend, in the chart below. To see the actual numbers, click on the chart.

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of Lovesac's forecast profits?

Are Lovesac Insiders Aligned With All Shareholders?

It should give investors a sense of security owning shares in a company if insiders also own shares, creating a close alignment their interests. So it is good to see that Lovesac insiders have a significant amount of capital invested in the stock. As a matter of fact, their holding is valued at US$14m. That's a lot of money, and no small incentive to work hard. Despite being just 4.3% of the company, the value of that investment is enough to show insiders have plenty riding on the venture.

While it's always good to see some strong conviction in the company from insiders through heavy investment, it's also important for shareholders to ask if management compensation policies are reasonable. Well, based on the CEO pay, you'd argue that they are indeed. The median total compensation for CEOs of companies similar in size to Lovesac, with market caps between US$200m and US$800m, is around US$2.8m.

Lovesac's CEO took home a total compensation package worth US$1.6m in the year leading up to January 2022. That seems pretty reasonable, especially given it's below the median for similar sized companies. CEO compensation is hardly the most important aspect of a company to consider, but when it's reasonable, that gives a little more confidence that leadership are looking out for shareholder interests. It can also be a sign of good governance, more generally.

Is Lovesac Worth Keeping An Eye On?

If you believe that share price follows earnings per share you should definitely be delving further into Lovesac's strong EPS growth. If that's not enough, consider also that the CEO pay is quite reasonable, and insiders are well-invested alongside other shareholders. This may only be a fast rundown, but the key takeaway is that Lovesac is worth keeping an eye on. It is worth noting though that we have found 2 warning signs for Lovesac (1 is concerning!) that you need to take into consideration.

There's always the possibility of doing well buying stocks that are not growing earnings and do not have insiders buying shares. But for those who consider these important metrics, we encourage you to check out companies that do have those features. You can access a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:LOVE

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|43.0% undervalued

JO

Community Contributor

Occidental Petroleum is set to achieve a 16% profit margin improvement

Fair Value US$55.05|21.5% undervalued

DZ

Community Contributor

Argan's Revenue Set to Soar with a 13.31% Growth in the Coming Decade

Fair Value US$284.68|23.4% undervalued

KE

Community Contributor

EU#1 - From German Startup to EU’s Biggest Company

Fair Value €248.62|7.6% overvalued

TO

Community Contributor