- United States

- /

- Leisure

- /

- NasdaqGS:HAS

Hasbro (HAS) Valuation Check as Digital Pivot and 2027 Game Delays Reshape Earnings Profile

Reviewed by Simply Wall St

Hasbro (HAS) has quietly turned into a very different business, and the stock is reacting. Strong Q3 gaming profits, plus the decision to delay Exodus and Dungeons & Dragons, Warlock to 2027, are giving investors a smoother earnings path.

See our latest analysis for Hasbro.

That shift toward higher margin gaming and digital, plus a steady stream of franchise tie ins from Marvel to Ghostbusters, has helped fuel a roughly mid 40s year to date share price return and a near 50 percent one year total shareholder return, signaling clear positive momentum rather than a one quarter pop.

If Hasbro’s pivot has your attention, this is also a good moment to explore other entertainment driven consumer names and see what stands out in fast growing stocks with high insider ownership.

With the stock up nearly 50 percent in a year and trading only modestly below analyst targets, the key question now is simple: are investors still underestimating Hasbro’s digital pivot, or is future growth already fully priced in?

Most Popular Narrative Narrative: 11% Undervalued

With Hasbro closing at $81.98 versus a narrative fair value near $92, the storyline leans toward upside as its transformation gathers pace.

Cost rationalization, supply chain diversification, and SKU optimization (cutting low margin or tariff hit products) post Entertainment One divestiture are enhancing operational efficiency and offsetting input cost headwinds. These initiatives are expected to structurally improve net margins and EBITDA over the next several years. Long term industry consolidation and Hasbro's strengthened position as an IP driven, multi channel entertainment company increase pricing power and cross licensing leverage. This combination should support higher gross margins and reduce volatility in earnings.

Curious how steady mid single digit growth plus a sharp swing into double digit margins can still point to meaningful upside from here? The full narrative unpacks the profit reset, the earnings run rate, and the valuation multiple that need to align for this price tag to make sense.

Result: Fair Value of $92.08 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, sustained weakness in traditional toys or a stumble in the digital rollout could quickly challenge today’s upbeat earnings and valuation assumptions.

Find out about the key risks to this Hasbro narrative.

Another Way to Look at Value

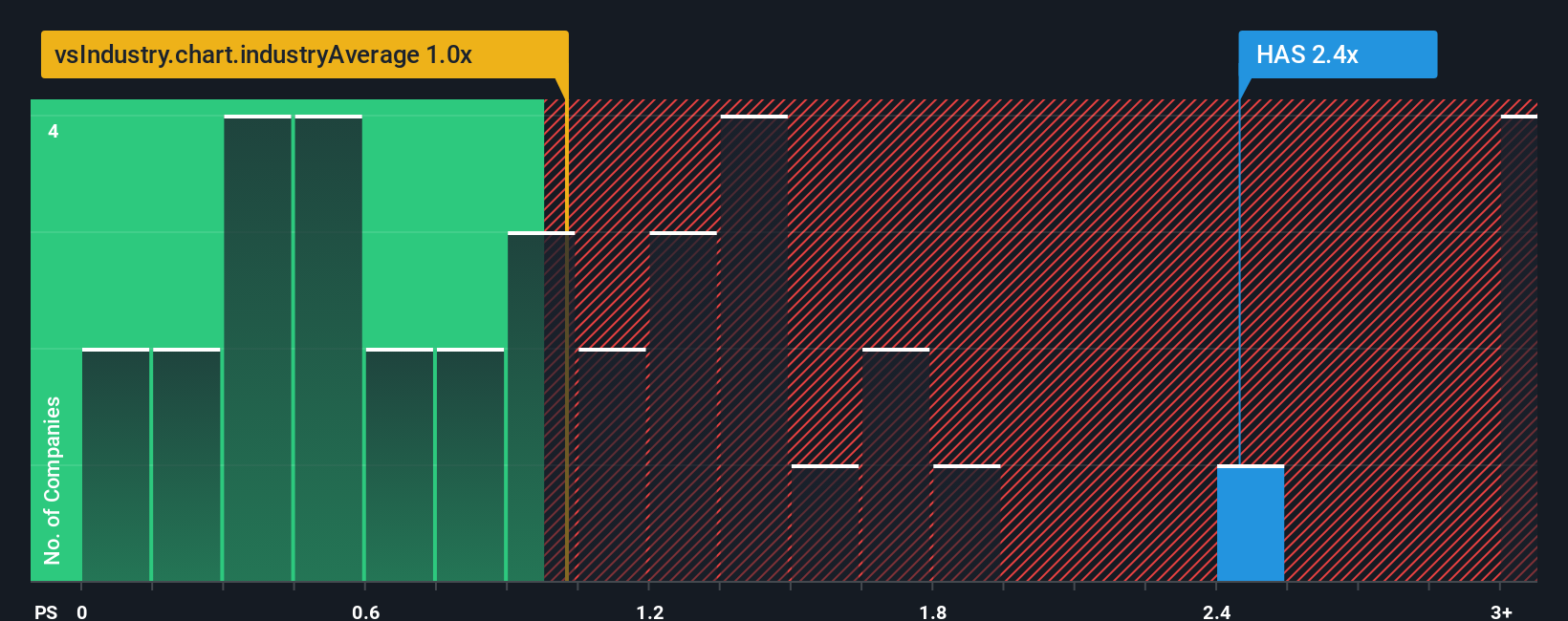

While the narrative fair value of about $92 suggests Hasbro is roughly 11% undervalued, its price to sales ratio of 2.6 times looks stretched against the US Leisure industry at 0.9 times and peers at 1.2 times, and even above a 2.2 times fair ratio. Is the market overpaying for the pivot story?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Hasbro Narrative

If this view does not fully match your own or you would rather dig into the numbers yourself, you can assemble a tailored narrative in just a few minutes, Do it your way.

A great starting point for your Hasbro research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If Hasbro has sharpened your appetite for opportunity, do not stop here, your next high conviction idea could be waiting in another corner of the market.

- Capture potential multibaggers early by scanning these 3634 penny stocks with strong financials with robust balance sheets and room to scale before the crowd notices.

- Capitalize on transformative automation and data trends by targeting these 24 AI penny stocks positioned at the crossroads of software, infrastructure, and real world adoption.

- Lock in value opportunities others overlook by focusing on these 914 undervalued stocks based on cash flows where strong cash flows contrast sharply with modest market expectations.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Hasbro might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:HAS

Hasbro

Operates as a toy and game company in the United States, Europe, Canada, Mexico, Latin America, Australia, China, and Hong Kong.

Reasonable growth potential average dividend payer.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion