Advertisement

- United States

- /

- Commercial Services

- /

- NYSE:WCN

Is Waste Connections’ (WCN) Dividend Hike and New Acquisitions Redefining Its Long-Term Growth Approach?

Simply Wall St

Reviewed by Sasha Jovanovic

- In the past week, Waste Connections reported third quarter revenue that topped expectations, while adjusted earnings per share missed forecasts, and announced an 11.1% rise in its quarterly dividend alongside share buybacks equal to about 1% of its shares. The company also disclosed that year-to-date, it has completed or secured formal agreements on acquisitions totalling approximately US$300 million in annual revenue.

- Alongside updated financial results, Waste Connections is highlighting its ongoing commitment to shareholder returns and continued growth through acquisition activity.

- We'll examine how the recent dividend hike and fresh acquisition agreements shape Waste Connections' long-term investment narrative and outlook.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Waste Connections Investment Narrative Recap

To be a shareholder in Waste Connections, you need to believe in the company’s multi-pronged growth model: consistent pricing power, disciplined acquisition, and steady returns to shareholders. The recent quarterly results, highlighting above-forecast revenues but earnings slightly below expectations and an increased dividend, do not materially shift the focus from acquisition execution as the most important catalyst or from integration risk as the main near-term concern.

The headline announcement of an 11.1% dividend increase stands out for investors. This step underscores Waste Connections’ commitment to rewarding shareholders even as acquisition activity continues. The dividend hike signals confidence, but reliable long-term returns remain closely tied to successful integration of new businesses, a recurring theme in the company’s outlook.

However, investors should also keep in mind that, despite increased shareholder returns, potential challenges can arise if new acquisitions do not deliver the expected synergies and...

Read the full narrative on Waste Connections (it's free!)

Waste Connections' outlook anticipates $11.3 billion in revenue and $1.7 billion in earnings by 2028. Achieving these targets would mean annual revenue growth of 7.1% and an earnings increase of $1.06 billion from the current $643.8 million.

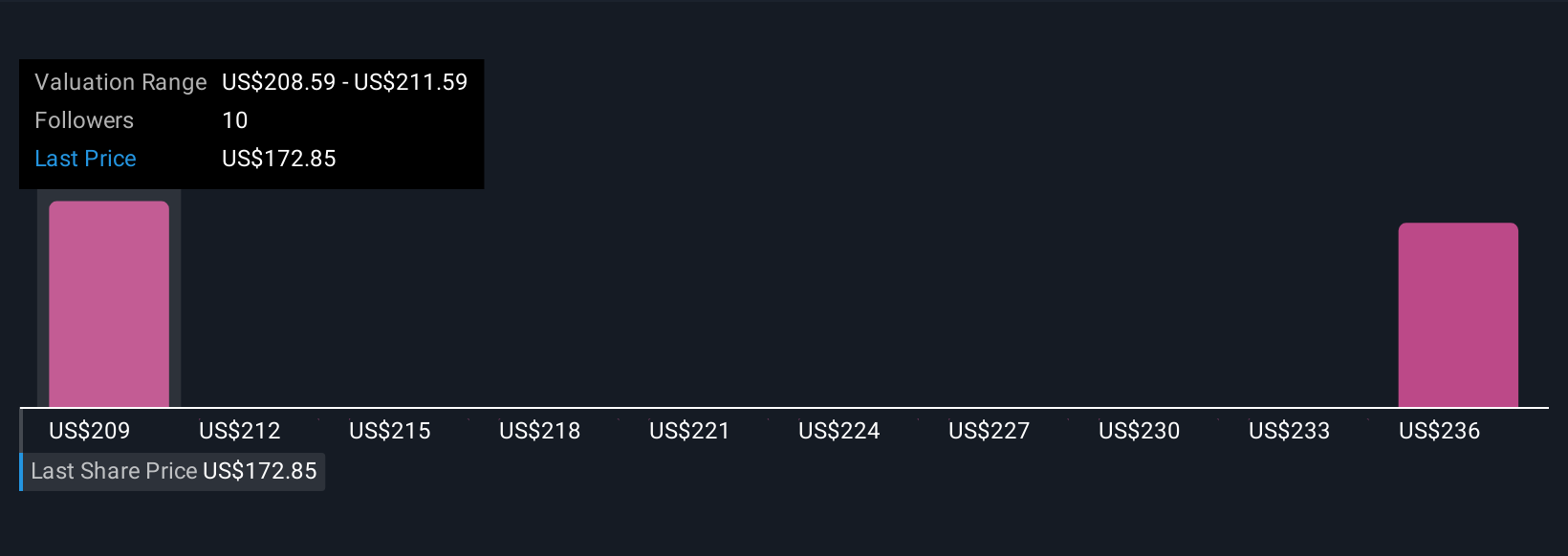

Uncover how Waste Connections' forecasts yield a $205.36 fair value, a 22% upside to its current price.

Exploring Other Perspectives

Two Simply Wall St Community members estimate Waste Connections' fair value between US$205.36 and US$246.09 per share. Many community participants watch margins closely, since acquisition integration could affect both near-term profits and the company's ability to sustain dividend growth.

Explore 2 other fair value estimates on Waste Connections - why the stock might be worth just $205.36!

Build Your Own Waste Connections Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Waste Connections research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Waste Connections research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Waste Connections' overall financial health at a glance.

Want Some Alternatives?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- We've found 14 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 37 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Waste Connections might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WCN

Waste Connections

Provides non-hazardous waste collection, transfer, disposal, and resource recovery services in the United States and Canada.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor