Advertisement

- United States

- /

- Commercial Services

- /

- NYSE:PBI

How Much Will Leadership Changes Shape Pitney Bowes' (PBI) Turnaround Ambitions?

Simply Wall St

Reviewed by Sasha Jovanovic

- Pitney Bowes announced that Brent Rosenthal has been elected as its new independent Chair of the Board, succeeding Milena Alberti-Perez, who stepped down to pursue opportunities in the media sector.

- Rosenthal’s extensive background in steering public companies through growth and transformation could shape boardroom priorities as Pitney Bowes continues its multi-year turnaround.

- With Rosenthal’s expertise in driving operational change, we will examine how this board transition could influence Pitney Bowes’ investment narrative.

The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Pitney Bowes Investment Narrative Recap

To be a shareholder in Pitney Bowes right now, you need to believe in the company’s ability to successfully pivot from its legacy mailing business to higher-growth shipping, logistics, and digital solutions. The appointment of Brent Rosenthal as independent Chair represents a commitment to strong governance and operational experience, though this board transition does not materially change short-term catalysts such as the growing SaaS shipping segment or the immediate risk of execution missteps amid ongoing leadership changes.

Of the recent announcements, the July share buyback stands out: Pitney Bowes repurchased over 11 million shares for US$115.25 million, underlining management’s focus on capital returns as they push forward on transformation efforts. This move, combined with new board leadership, reinforces the emphasis on driving shareholder value but puts even more pressure on the company to deliver on margin improvement and growth initiatives.

However, investors should be aware that, even with leadership changes and capital returns, persistent revenue declines in core mailing remain a risk if...

Read the full narrative on Pitney Bowes (it's free!)

Pitney Bowes' narrative projects $1.9 billion revenue and $348.2 million earnings by 2028. This requires a 2.1% annual revenue decline and a $202.3 million increase in earnings from $145.9 million today.

Uncover how Pitney Bowes' forecasts yield a $17.00 fair value, a 53% upside to its current price.

Exploring Other Perspectives

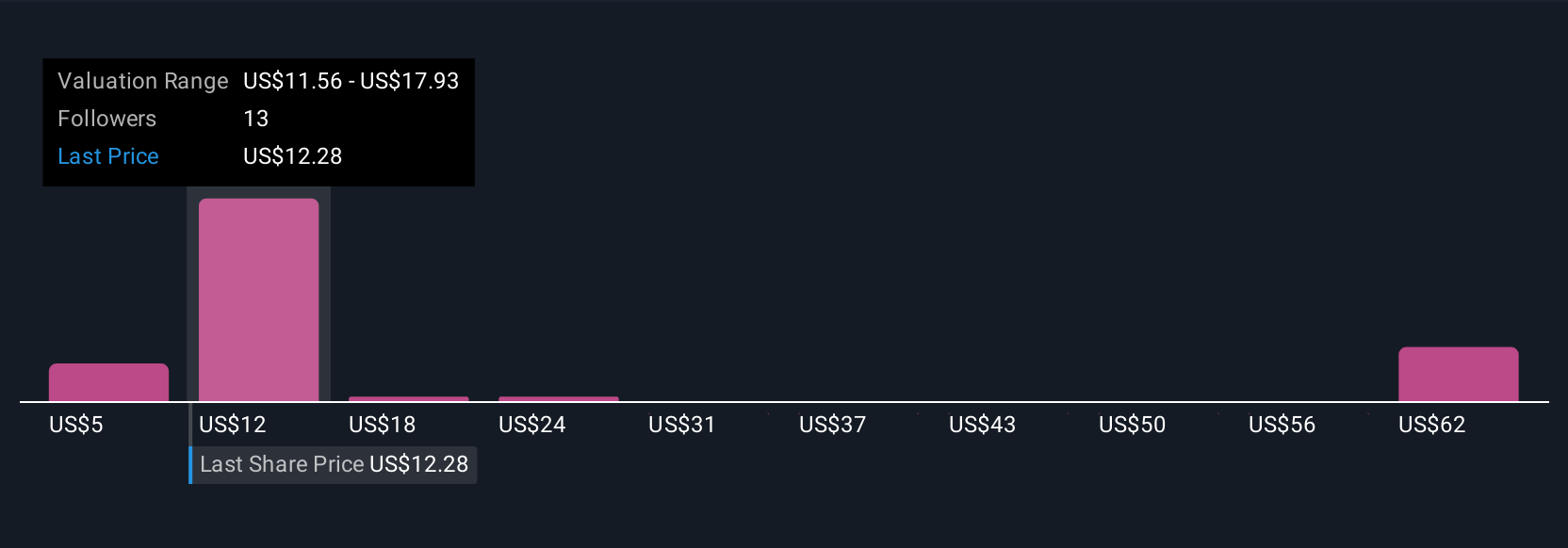

Simply Wall St Community members estimate Pitney Bowes’ fair value anywhere from US$5.20 to US$65.01, with 11 different perspectives contributing. Many are watching to see whether recent board realignment can overcome ongoing pressure as competition and digitization weigh on key revenue streams, highlighting how divergent investor views can be, and encouraging you to seek out a range of insights before considering your next move.

Explore 11 other fair value estimates on Pitney Bowes - why the stock might be worth less than half the current price!

Build Your Own Pitney Bowes Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Pitney Bowes research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Pitney Bowes research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Pitney Bowes' overall financial health at a glance.

Curious About Other Options?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Rare earth metals are the new gold rush. Find out which 35 stocks are leading the charge.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PBI

Pitney Bowes

Operates as a technology-driven company that provides SaaS shipping solutions, mailing innovation, and financial services to small businesses, large enterprises, and government entities around the world.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets