Advertisement

- United States

- /

- Commercial Services

- /

- NasdaqGS:MLKN

How MillerKnoll’s (MLKN) ESOP Share Offering Could Shape Its Investment Story

Simply Wall St

Reviewed by Sasha Jovanovic

- On October 17, 2025, MillerKnoll, Inc. filed a shelf registration for up to 3,400,000 shares of common stock valued at approximately US$56.92 million, specifically for its Employee Stock Ownership Plan (ESOP).

- This move signals a significant step in the company's approach to corporate finance and employee ownership, with potential implications for both capital structure and workforce engagement.

- We'll explore how the ESOP-related share offering could influence MillerKnoll's investment narrative and future business direction.

We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

MillerKnoll Investment Narrative Recap

To own MillerKnoll as a shareholder, you need to believe in the company’s ability to balance its recovery momentum, cost controls, and execution in a challenging macroeconomic setting. The recent ESOP-related shelf registration likely does not materially impact the short-term catalyst around improving retail segment performance or change the principal risk, which remains tied to macro pressures and ongoing asset impairments. Of all the recent company updates, MillerKnoll’s first-quarter FY2026 earnings showed encouraging year-on-year improvements in sales and net income, which aligns directly with the key catalyst of retail expansion and international market growth. However, the ESOP share offering does not shift the importance of stabilizing margins and sustaining profitability, especially as management focuses on margins amid tariffs and trade policy volatility. But what some investors are missing is that, while retail expansion signals growth, the persistent risks of asset impairments and margin pressures remain critical information that investors should be aware of...

Read the full narrative on MillerKnoll (it's free!)

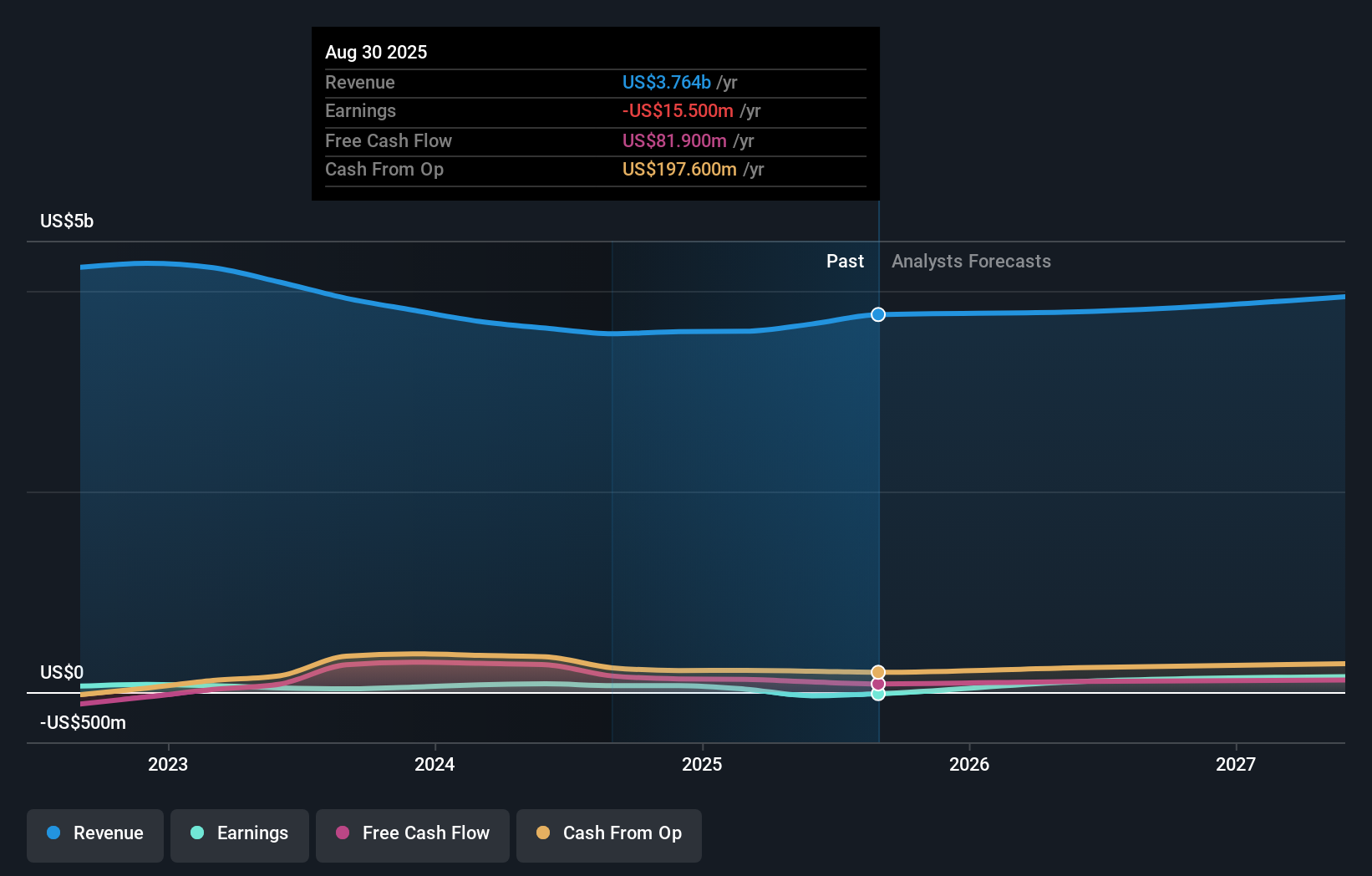

MillerKnoll's outlook foresees $4.0 billion in revenue and $293.0 million in earnings by 2028. This is based on a projected annual revenue growth rate of 3.2% and an earnings increase of $329.9 million from current earnings of -$36.9 million.

Uncover how MillerKnoll's forecasts yield a $35.00 fair value, a 108% upside to its current price.

Exploring Other Perspectives

The Simply Wall St Community offers 1 fair value estimate for MillerKnoll, all clustering at US$35 per share. While the outlook on retail segment recovery is positive, keep in mind that asset-related risks may shape future performance for those considering different scenarios.

Explore another fair value estimate on MillerKnoll - why the stock might be worth over 2x more than the current price!

Build Your Own MillerKnoll Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your MillerKnoll research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free MillerKnoll research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MillerKnoll's overall financial health at a glance.

Contemplating Other Strategies?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:MLKN

MillerKnoll

Researches, designs, manufactures, sells, and distributes interior furnishings worldwide.

Good value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|10.4% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|12.4% undervalued

AN

Based on Analyst Price Targets