Advertisement

- United States

- /

- Commercial Services

- /

- NasdaqGS:CWST

Casella Waste Systems (CWST): Valuation Revisited After Analyst Upside Call Spurs Renewed Investor Interest

Simply Wall St

Reviewed by Kshitija Bhandaru

Casella Waste Systems (CWST) shares climbed after Stifel resumed coverage with a Buy rating, highlighting the company’s ownership of landfills in regions where demand is high and its track record of strong revenue growth.

See our latest analysis for Casella Waste Systems.

After a tough three months marked by a notable dip, Casella Waste Systems’ share price has started to regain investor interest, thanks to renewed analyst optimism and robust sector-wide trends. While the share price has slipped this year, the company’s three-year total shareholder return of 28% shows longer-term holders have still enjoyed meaningful gains. This suggests momentum could build from here if growth takes hold.

If sector optimism has you wondering what else could be stirring up the market, this is the perfect opportunity to broaden your search and uncover fast growing stocks with high insider ownership

The question now facing investors is whether Casella’s recent pullback has unlocked hidden value, or if the market has already factored in the company’s growth prospects and left little room for upside from here.

Most Popular Narrative: 22.6% Undervalued

Casella Waste Systems is currently trading at $91.78, while the narrative’s fair value estimate stands at $118.51. This creates a notable price gap and spurs debate about future growth expectations. The current valuation depends on whether the company’s ambitious reinvestment and regional expansion strategies can deliver the anticipated operational improvements and profit growth.

Infrastructure investments, such as automation in fleet (with 55 new and mostly automated trucks coming in late 2025), upgraded ERP systems, and route optimization, are expected to unlock significant operational efficiencies. These measures are aimed at capturing previously delayed cost synergies in the Mid-Atlantic region, which could materially boost net margins and EBITDA starting in 2026.

Want the inside scoop on what’s driving this bullish target? The narrative’s thesis leans heavily on a bold turnaround in profitability and efficiency. The real surprise is just how steep the shift is projected to be. Curious about the financial forecasts that power this valuation? Unlock the full narrative to see the story behind the price.

Result: Fair Value of $118.51 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, ongoing integration delays in the Mid-Atlantic region and rising labor costs could quickly derail margin expansion and challenge the positive long-term outlook.

Find out about the key risks to this Casella Waste Systems narrative.

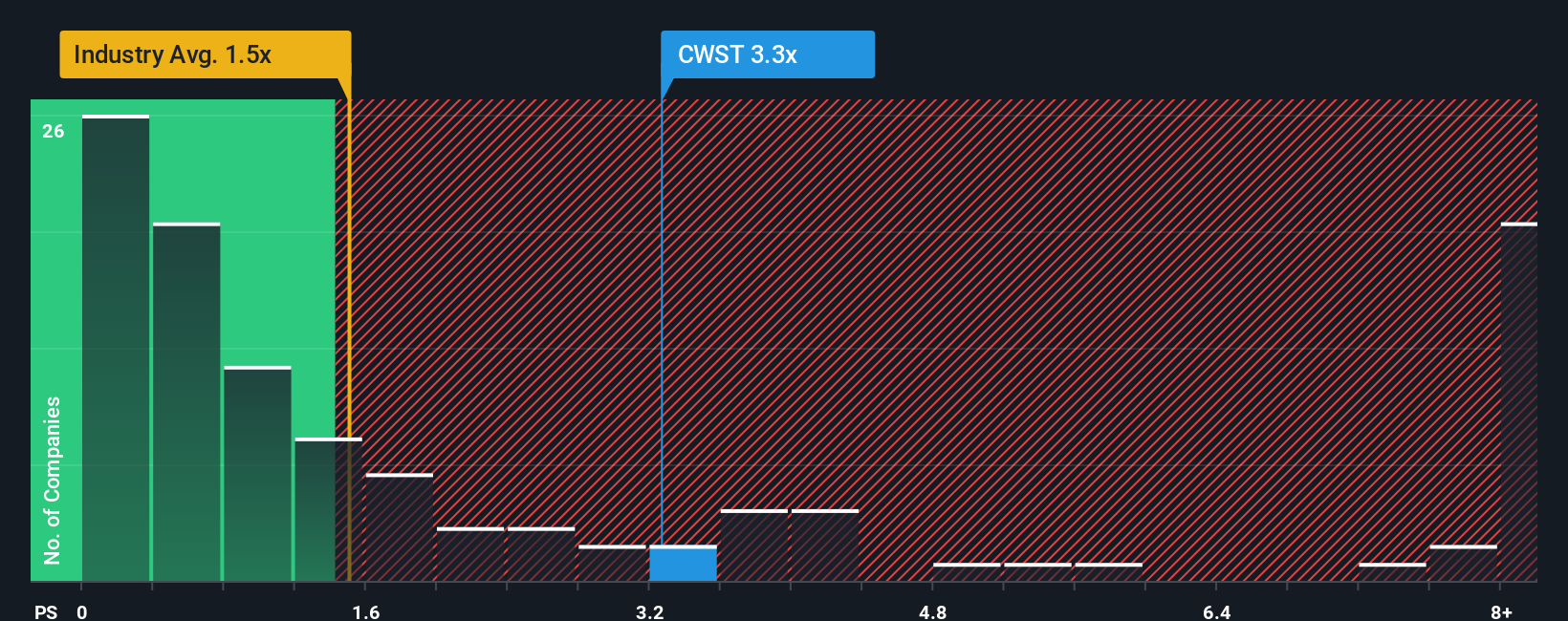

Another View: Multiples Signal a Caution

While the narrative’s fair value suggests Casella Waste Systems may be undervalued, a look at its price-to-sales ratio paints a different picture. At 3.4x, the company trades significantly higher than both the US Commercial Services industry average of 1.6x and the peer average of 1.8x. It is also well above the fair ratio of 1.8x. This means the current market price may be building in a premium that could vanish if expectations shift. Is this a sign of confidence or a warning for investors?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Casella Waste Systems Narrative

If you have a different perspective or prefer hands-on research, you can quickly shape your own Casella Waste Systems analysis in under three minutes with Do it your way.

A great starting point for your Casella Waste Systems research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t let your next great investment pass you by. Use the Simply Wall Street Screener to uncover compelling stocks others may be overlooking right now.

- Supercharge your search for strong passive income by uncovering these 19 dividend stocks with yields > 3% with reliable yields above 3% and resilient fundamentals.

- Anticipate industry transformation in medicine and care by tapping into these 31 healthcare AI stocks at the forefront of AI-driven healthcare innovation.

- Capitalize early on under-the-radar gems trading at attractive valuations with these 896 undervalued stocks based on cash flows that offer untapped potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CWST

Casella Waste Systems

Operates as a vertically integrated solid waste services company in the United States.

Moderate growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor