Advertisement

- United States

- /

- Professional Services

- /

- NasdaqGS:ADP

Is ADP’s Recent Share Price Slump Creating a Long Term Opportunity in 2025?

Reviewed by Bailey Pemberton

- Wondering if Automatic Data Processing is quietly turning into a value opportunity, or if the market already baked in all the good news? Let us unpack what the current share price is really telling you.

- ADP last closed at $261.63, and while the stock is up 2.5% over the past week and 0.8% over the past month, it is still down 9.7% year to date and 12.3% over the last year, even after gaining 8.0% over three years and 66.2% over five years.

- Recent moves have come against a backdrop of steady interest in payroll automation and HR outsourcing, as employers look to streamline costs and reduce administrative risk. Alongside rising competition in human capital management tech and ongoing macro uncertainty, investors are reassessing what kind of long term growth multiple ADP really deserves.

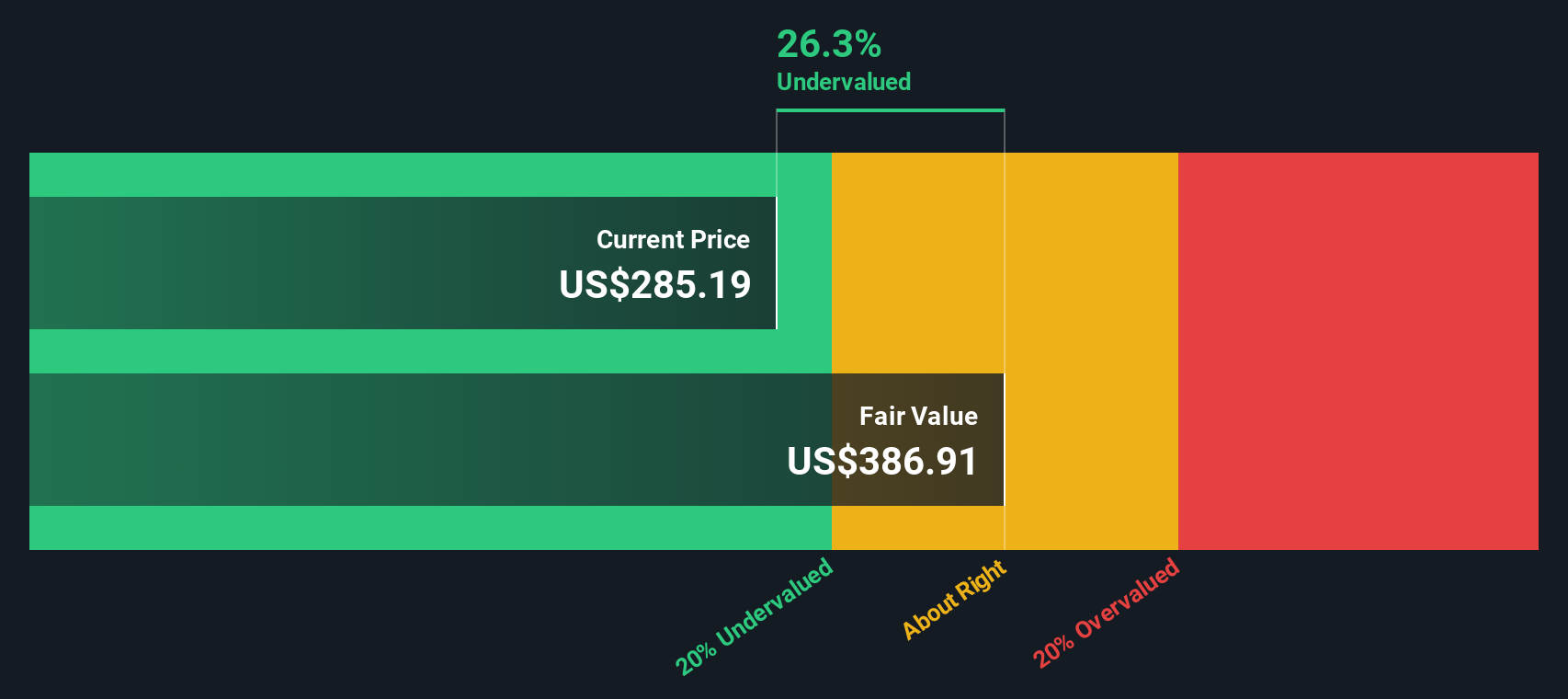

- On our checks, ADP scores a 3/6 valuation score. This suggests it is undervalued on some measures but not screamingly cheap across the board. We will walk through those methods next, before circling back to an even more intuitive way of thinking about its true value.

Approach 1: Automatic Data Processing Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth by projecting the cash it can generate in the future and then discounting those cash flows back to today in dollar terms.

For Automatic Data Processing, the 2 Stage Free Cash Flow to Equity model starts with last twelve months free cash flow of about $4.2 billion. It then uses analyst forecasts through 2028 and extrapolations beyond that. Analysts see free cash flow reaching roughly $5.6 billion by 2028, with Simply Wall St extending those projections out a further seven years using modest growth assumptions.

When all those projected cash flows are discounted back, the model arrives at an intrinsic value of about $319 per share. That is roughly 18.0% above the recent share price around $262, implying that the market is not fully crediting ADP for its future cash generation.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Automatic Data Processing is undervalued by 18.0%. Track this in your watchlist or portfolio, or discover 906 more undervalued stocks based on cash flows.

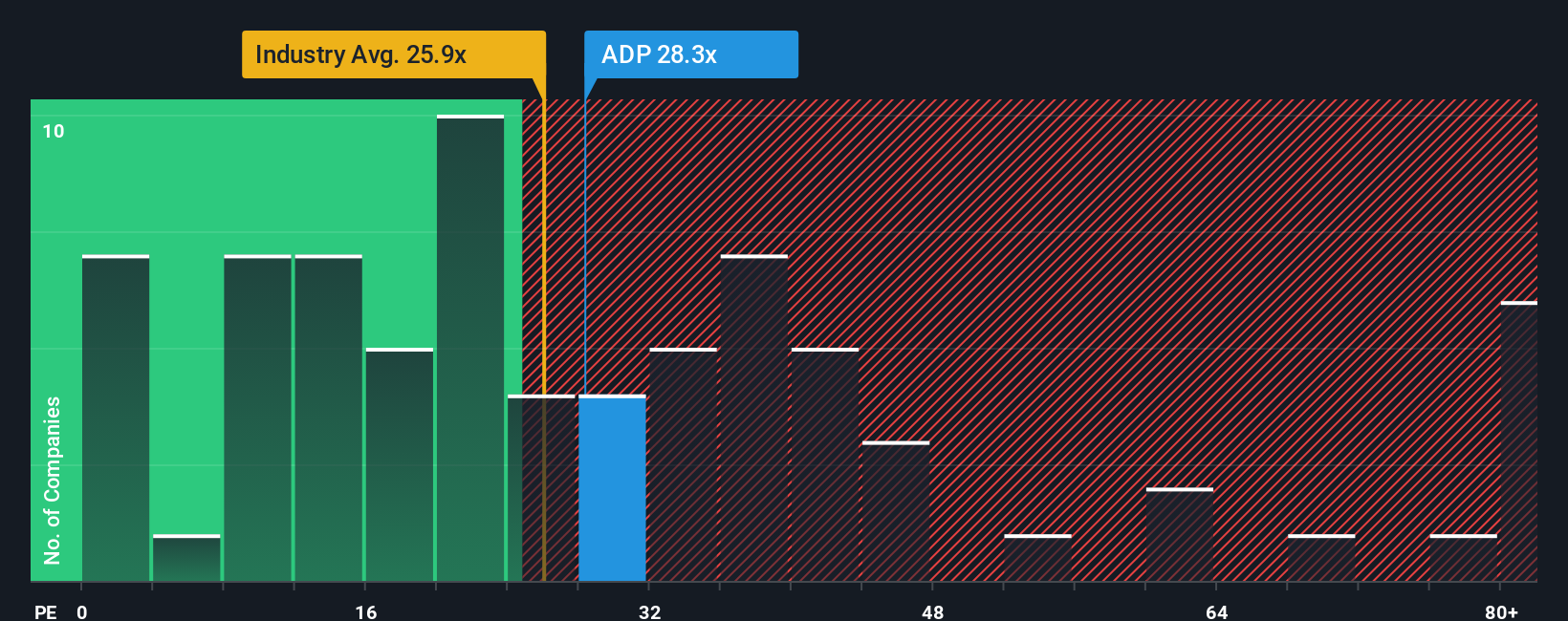

Approach 2: Automatic Data Processing Price vs Earnings

For a mature, consistently profitable business like Automatic Data Processing, the price to earnings multiple is a useful way to assess valuation because it directly links what investors pay today to the company’s current earnings power. In general, faster and more reliable earnings growth, combined with lower perceived risk, justifies a higher, or more generous, PE ratio, while slower or more volatile growth tends to cap the multiple investors are willing to pay.

ADP currently trades on a PE of about 25.6x, which sits slightly above the broader Professional Services industry average of roughly 24.9x but below the peer group average near 27.3x. Simply Wall St’s proprietary Fair Ratio framework goes a step further by estimating what PE the stock should trade on, given its earnings growth outlook, profit margins, industry positioning, size and risk profile. For ADP, that Fair Ratio comes out at around 32.8x. This indicates that the shares trade at a meaningful discount to the multiple that would normally be warranted by its fundamentals, even after accounting for industry context and company specific risks.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

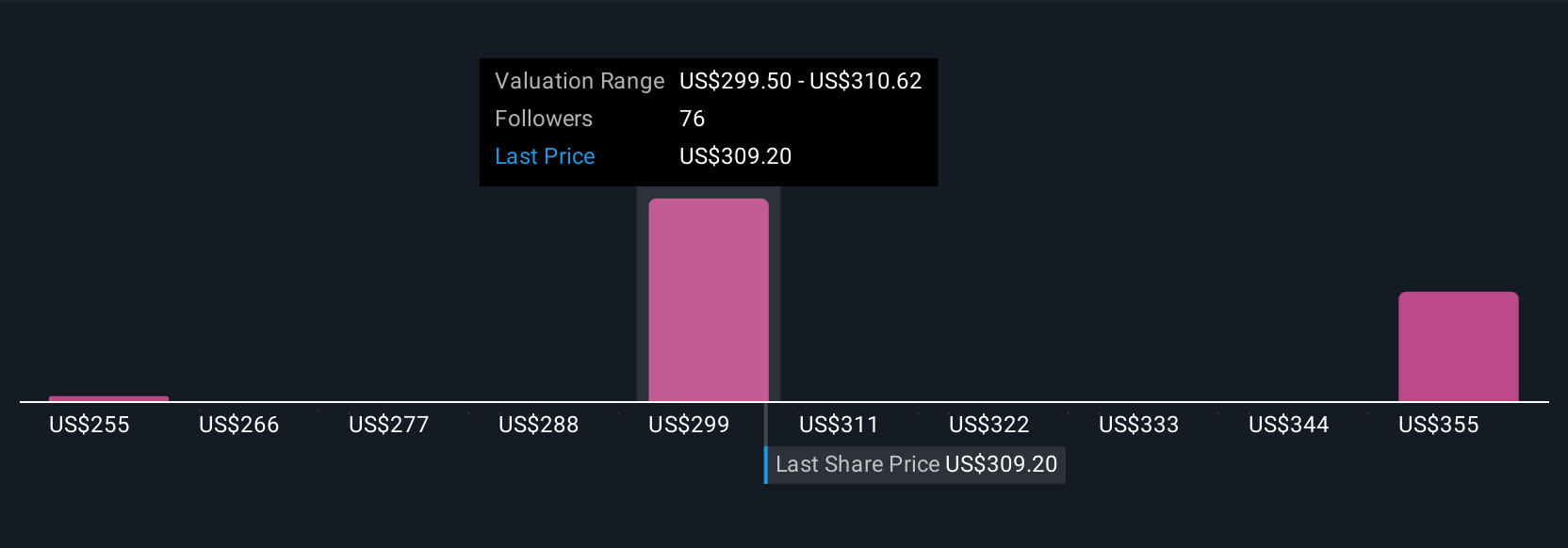

Upgrade Your Decision Making: Choose your Automatic Data Processing Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to attach a story, your view of a company’s future revenue, earnings and margins, to the numbers you see on screen.

A Narrative links three things together in one place: the business story, a quantified forecast, and a resulting fair value estimate, so you can see exactly how your expectations translate into a buy, hold or sell view.

On Simply Wall St, Narratives live in the Community page and are used by millions of investors as an easy, accessible tool to compare their own fair value to the current share price, helping them decide whether ADP looks attractively priced or too expensive.

Because Narratives are refreshed dynamically when new information emerges, such as earnings, product launches or macro news, your fair value view updates automatically instead of becoming stale.

For example, one ADP Narrative on the platform currently assumes a fair value near $388 per share based on faster AI led margin expansion. Another, more cautious view sees fair value closer to $293 based on slower growth and more competitive pressure, illustrating how different perspectives on the same company can still be grounded in clear, comparable numbers.

Do you think there's more to the story for Automatic Data Processing? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ADP

Automatic Data Processing

Provides cloud-based human capital management (HCM) solutions worldwide.

Undervalued with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Gain Therapeutics ·

The Market Is Sleeping on This Parkinson's Biotech - And I Think That's a Mistake

Fair Value:US$7.675.1% undervalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.235.6% undervalued

40 followersusers have followed this narrative

1 commentusers have commented on this narrative

16 likesusers have liked this narrative

TE

TechMegaTrends on Bambuser ·

Bambuser is today the only listed company in Europe that simultaneously possesses an 85% gross margin, proprietary AI infrastructure for the

Fair Value:SEK 238.2685.8% undervalued

27 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

HE

HedgeY on Constellium ·

Constellium jet another cyclical aluminum processor, or a mispriced aluminum platform?

Fair Value:US$3410.2% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

AV

avt on TROPHY GAMES Development ·

TROPHY GAMES Development Will See Revenue Rise by 22% in the Next 3 Years

Fair Value:DKK 21.0133.6% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.235.6% undervalued

40 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

RE

REElax on Volta Metals ·

Springer REE deposit valuation

Fair Value:CA$3.594.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3950.5% undervalued

45 followersusers have followed this narrative

3 commentsusers have commented on this narrative

42 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

38 followersusers have followed this narrative

11 commentsusers have commented on this narrative

32 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$587.3133.1% undervalued

1361 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative