Advertisement

- United States

- /

- Trade Distributors

- /

- NYSE:WSO

Watsco's (NYSE:WSO) Shareholders Will Receive A Bigger Dividend Than Last Year

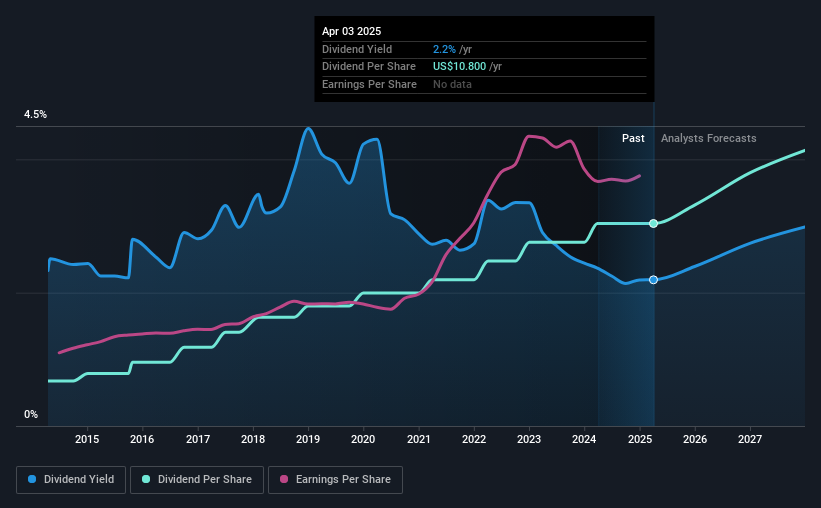

Watsco, Inc. (NYSE:WSO) has announced that it will be increasing its periodic dividend on the 30th of April to $3.00, which will be 11% higher than last year's comparable payment amount of $2.70. This makes the dividend yield 2.2%, which is above the industry average.

Watsco's Future Dividend Projections Appear Well Covered By Earnings

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Before this announcement, Watsco was paying out 79% of earnings, but a comparatively small 55% of free cash flows. In general, cash flows are more important than earnings, so we are comfortable that the dividend will be sustainable going forward, especially with so much cash left over for reinvestment.

The next year is set to see EPS grow by 36.0%. Assuming the dividend continues along the course it has been charting recently, our estimates show the payout ratio being 70% which brings it into quite a comfortable range.

See our latest analysis for Watsco

Watsco Has A Solid Track Record

Even over a long history of paying dividends, the company's distributions have been remarkably stable. Since 2015, the dividend has gone from $2.40 total annually to $10.80. This means that it has been growing its distributions at 16% per annum over that time. Rapidly growing dividends for a long time is a very valuable feature for an income stock.

Watsco Might Find It Hard To Grow Its Dividend

The company's investors will be pleased to have been receiving dividend income for some time. Watsco has seen EPS rising for the last five years, at 15% per annum. The payout ratio is very much on the higher end, which could mean that the growth rate will slow down in the future, and that could flow through to the dividend as well.

Our Thoughts On Watsco's Dividend

Overall, it's great to see the dividend being raised and that it is still in a sustainable range. The payments look pretty sustainable with good earnings coverage and a reasonable track record. Taking all of this into consideration, the dividend looks viable moving forward, but investors should be mindful that the company has pushed the boundaries of sustainability in the past and may do so again.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Companies that are growing earnings tend to be the best dividend stocks over the long term. See what the 15 analysts we track are forecasting for Watsco for free with public analyst estimates for the company . If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Watsco might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:WSO

Watsco

Engages in the distribution of air conditioning, heating, and refrigeration equipment, and related parts and supplies in the United States, Canada, Latin America, and the Caribbean.

Flawless balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor