- United States

- /

- Electrical

- /

- NYSE:VRT

Vertiv Holdings Co (NYSE:VRT) Reports Strong Q1 2025 Earnings With Revenue Increase

Reviewed by Simply Wall St

Vertiv Holdings Co (NYSE:VRT) made headlines by collaborating with NVIDIA and iGenius on creating a sovereign AI data center in Italy, potentially contributing to a price surge of 20% last week. The company reported strong Q1 2025 earnings with enhanced revenue and a substantial net income turnaround. These developments aligned with the announcement to raise full-year sales guidance, adding positive sentiment. Despite a general market rise of 5.2% last week amid mixed economic signals like weak GDP reports, Vertiv's specific growth indicators and strategic initiatives seem to have provided additional lift to its shares.

We've identified 2 warning signs for Vertiv Holdings Co that you should be aware of.

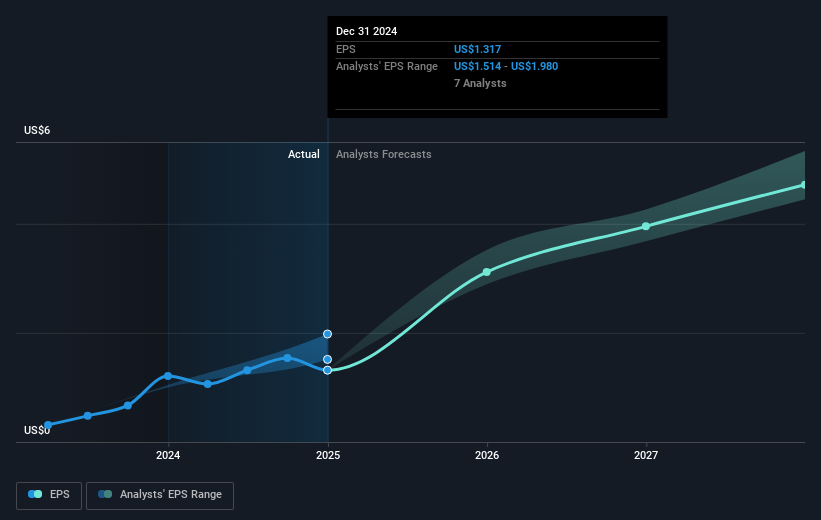

The recent collaboration between Vertiv Holdings Co, NVIDIA, and iGenius on producing a sovereign AI data center in Italy has implications beyond short-term share price fluctuations. This partnership aligns with Vertiv's efforts to drive long-term revenue growth through investments in AI infrastructure and advanced data center solutions. The initiatives might strengthen Vertiv's overall revenue and earnings forecasts, potentially contributing to an uplift in their projected financial performance. Analysts anticipate revenue growth of 11.2% annually, which may be supported further by strategic collaborations like this. If successfully executed, these projects could increase Vertiv's market share in the AI and data center sectors, reinforcing earnings growth expectations.

Over the past five years, Vertiv's total return, including share price and dividends, experienced a very large increase, highlighting the substantial value creation for shareholders during this period. Despite market or industry fluctuations, the company's strategic maneuvers have enabled it to outperform, growing significantly faster than the US Electrical industry's recent challenging environment and maintaining a strong return on equity of 24.99%. However, in the last year, Vertiv underperformed compared to the overall US market return of 9.9%, although it outpaced its specific industry, which posted a lower growth figure.

As of April 30, 2025, Vertiv's share price is US$71.82, positioned below the consensus price target of US$108.14. This indicates a potential upside of 36.0%, according to analysts, reflecting optimism in the company's growth trajectory and strategic initiatives. The potential for future enhancements in both Vertiv's operational performance and market positioning could help align the share price more closely with these projected targets. As always, investors should consider their own insights alongside these analyses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:VRT

Vertiv Holdings Co

Designs, manufactures, and services critical digital infrastructure technologies and life cycle services for data centers, communication networks, and commercial and industrial environments in the Americas, the Asia Pacific, Europe, the Middle East, and Africa.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Community Narratives