Advertisement

- United States

- /

- Electrical

- /

- NYSE:VRT

Should You Reassess Vertiv After Its Rapid 52% Jump and AI Sector Buzz in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Vertiv Holdings Co is still a good value after its rapid rise? You are not alone. We break down what investors need to know.

- The stock has delivered a 51.9% gain so far this year, adding to a 1121.5% return over the past three years. However, it dipped 9.8% in the last month.

- Much of the recent excitement is due to Vertiv's prominent role in the AI infrastructure sector. Analysts and industry observers have highlighted its position as a key supplier for advanced data center power and cooling. News reports pointing to strong sector demand and strategic partnerships have also attracted investor attention and sparked discussions about the company's future growth prospects.

- If you review its value score, Vertiv comes in at just 1 out of 6 for undervaluation. This suggests there may be more to consider. We will look at how traditional valuation tools assess Vertiv and discuss an alternative way to evaluate value at the end of this article.

Vertiv Holdings Co scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Vertiv Holdings Co Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and discounting them back to their value today. This approach helps investors gauge if a stock is trading at a premium or a discount relative to its underlying financial potential.

For Vertiv Holdings Co, the analysis starts with its latest twelve months Free Cash Flow of $1.36 Billion. According to analyst forecasts, annual free cash flow is expected to rise steadily, reaching an estimated $4.02 Billion by 2029. In addition to the analyst-provided projections, further estimates extend out ten years using growth assumptions to capture long-term potential. These future values are then discounted to reflect their worth in today's dollars.

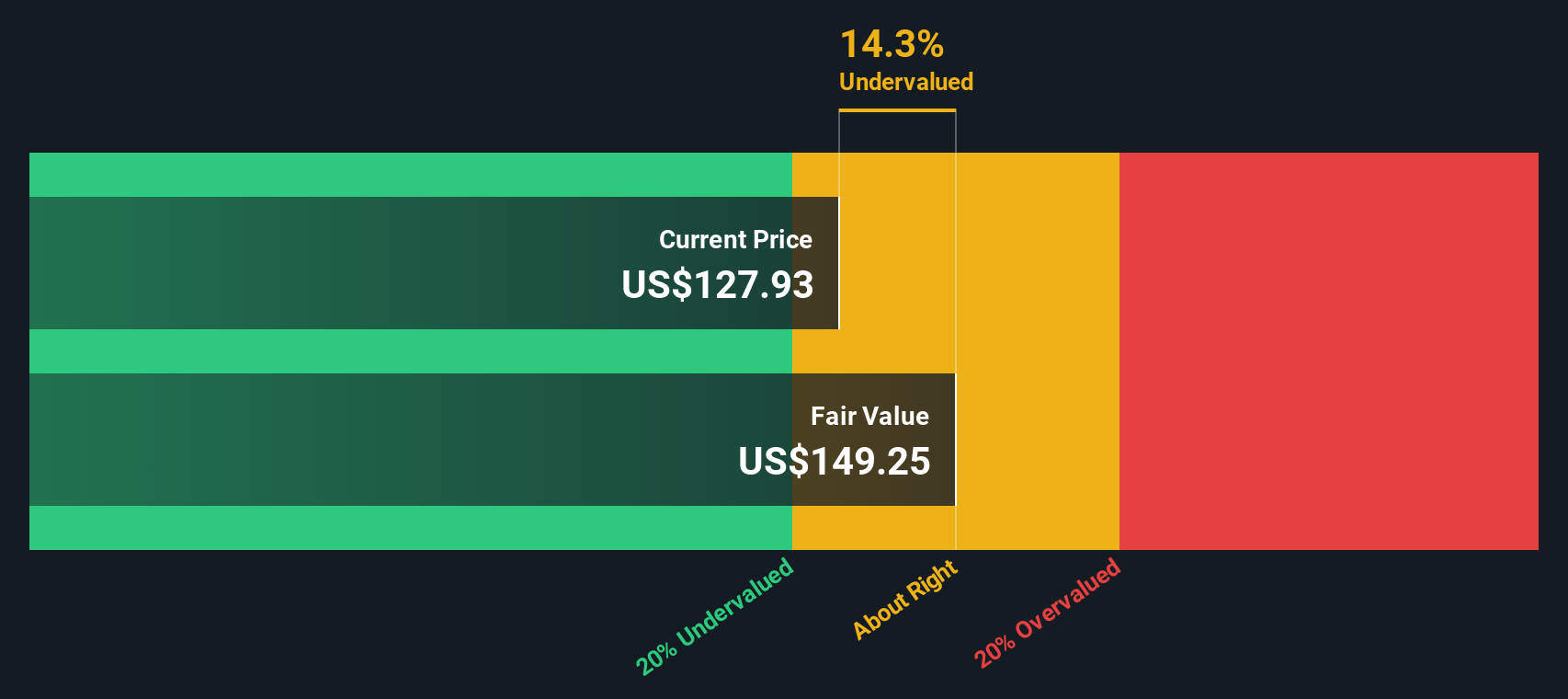

Based on this DCF model, Vertiv's intrinsic value is calculated at $215.55 per share. This suggests the stock is currently 16.6% undervalued compared to its market price, indicating potential for upside if the company meets or exceeds these cash flow projections.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Vertiv Holdings Co is undervalued by 16.6%. Track this in your watchlist or portfolio, or discover 920 more undervalued stocks based on cash flows.

Approach 2: Vertiv Holdings Co Price vs Earnings

The Price-to-Earnings (PE) ratio is a commonly used valuation metric for profitable companies because it allows investors to quickly assess how much they are paying for each dollar of current earnings. When a company demonstrates a strong track record of profitability, the PE ratio provides insight into how the market evaluates its growth potential compared to its risks.

Growth expectations and risk profile play a major role in determining what is considered a reasonable or "fair" PE ratio for a stock. Higher growth prospects can justify a higher PE, while increased risk or slower earnings growth typically results in a lower one. Comparing Vertiv Holdings Co's current valuation to relevant benchmarks helps clarify its market positioning.

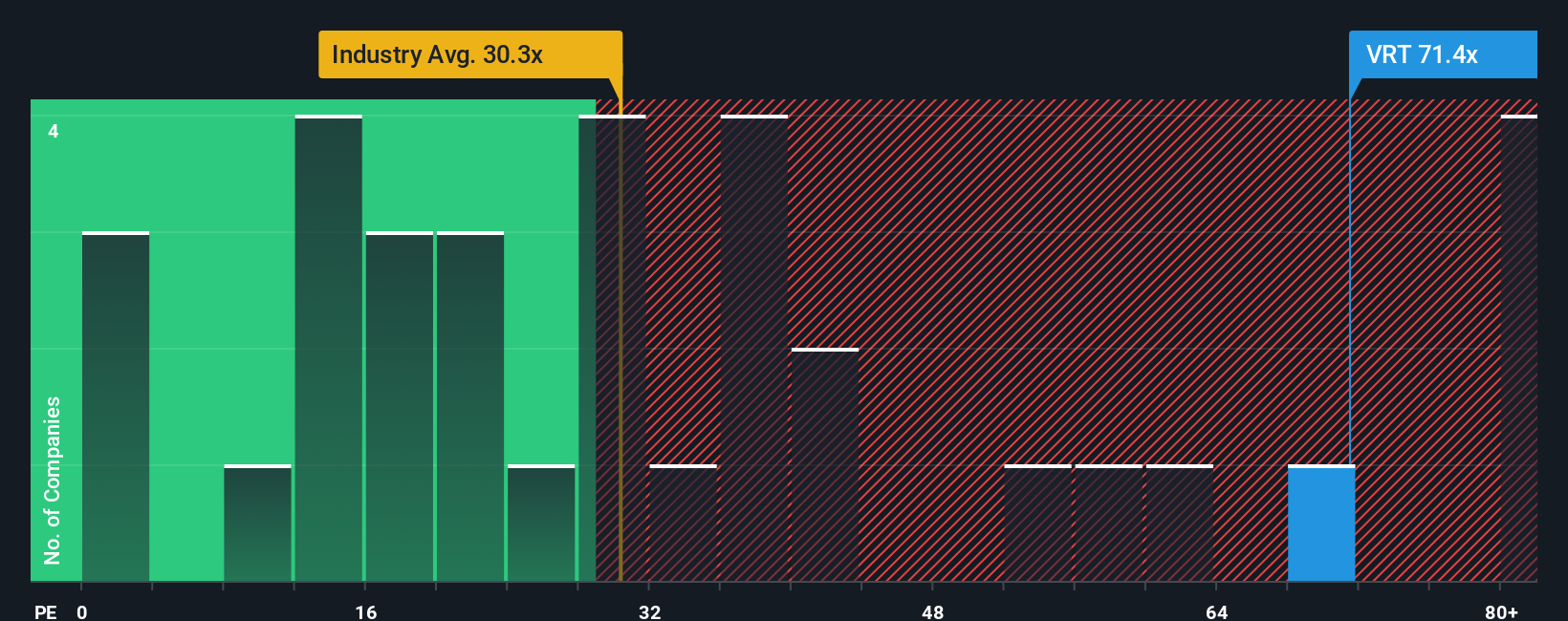

Vertiv currently trades at a PE ratio of 66.45x. In comparison, its industry average PE is 31.02x, and the average among close peers is 37.31x. At first glance, this suggests Vertiv is priced at a significant premium compared to both its industry and peers. However, Simply Wall St’s proprietary "Fair Ratio" for Vertiv is 62.73x, which aims to reflect what an informed investor might pay after considering Vertiv's earnings growth, business risks, profit margins, industry position, and market capitalization.

The Fair Ratio offers more insight than simply comparing to industry or peers, as it tailors expectations specifically for Vertiv. By accounting for its unique characteristics, such as higher expected growth and sector leadership, it provides a more personalized valuation benchmark. In this instance, Vertiv’s current PE of 66.45x is only slightly above its Fair Ratio of 62.73x, placing it well within a typical premium for the quality and growth profile associated with the company.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Vertiv Holdings Co Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is simply the story you tell about a company—your point of view about its business, why it will succeed or struggle, and what you expect from its future revenue, earnings, and profit margins. Unlike traditional financial metrics that offer a snapshot in time, Narratives connect your personal perspective to dynamic forecasts and translate them into a fair value for the stock.

Narratives make investing easy by guiding you from your story about Vertiv Holdings Co straight into numbers, right through to a Fair Value, so you always know if you think the stock is under- or overvalued at its current price. On Simply Wall St’s Community page, millions of investors are already building and updating their Narratives as new news drops or earnings get released, helping users keep their perspectives up to date.

This approach also shows how investors can arrive at very different conclusions. For example, one user’s Narrative projects a bullish fair value of $173 per share driven by surging AI-powered demand and expanding margins, while another’s more cautious Narrative sees fair value at just $119 due to ongoing supply chain risks and competitive threats.

Do you think there's more to the story for Vertiv Holdings Co? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:VRT

Vertiv Holdings Co

Designs, manufactures, and services critical digital infrastructure technologies and life cycle services for data centers, communication networks, and commercial and industrial environments in the Americas, the Asia Pacific, Europe, the Middle East, and Africa.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative