Advertisement

- United States

- /

- Electrical

- /

- NYSE:VRT

Is Vertiv Still Attractive After Its 1290% Surge on AI Data Center Optimism?

Simply Wall St

Reviewed by Bailey Pemberton

- If you are wondering whether Vertiv Holdings Co is still a smart buy after its huge run, or if the easy money has already been made, you are not alone and that is exactly what we are going to unpack here.

- The stock has gained an eye catching 1290.2% over the past 3 years and is still up 59.8% year to date, even after a small 0.9% dip over the last month and a 5.2% rebound in the past week.

- A big part of the story has been growing enthusiasm around Vertiv as a picks and shovels player for data centers and AI infrastructure, with investors focusing on its role in power and thermal management. At the same time, headlines about capacity expansion plans and broader AI capex spending have kept expectations and volatility elevated.

- Despite all that excitement, Vertiv currently scores just 1 out of 6 on our valuation checks. This suggests it only screens as undervalued on one of our methods. Next we will walk through those different valuation approaches and then finish with an even more practical way to judge whether the stock still deserves a spot in your portfolio.

Vertiv Holdings Co scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Vertiv Holdings Co Discounted Cash Flow (DCF) Analysis

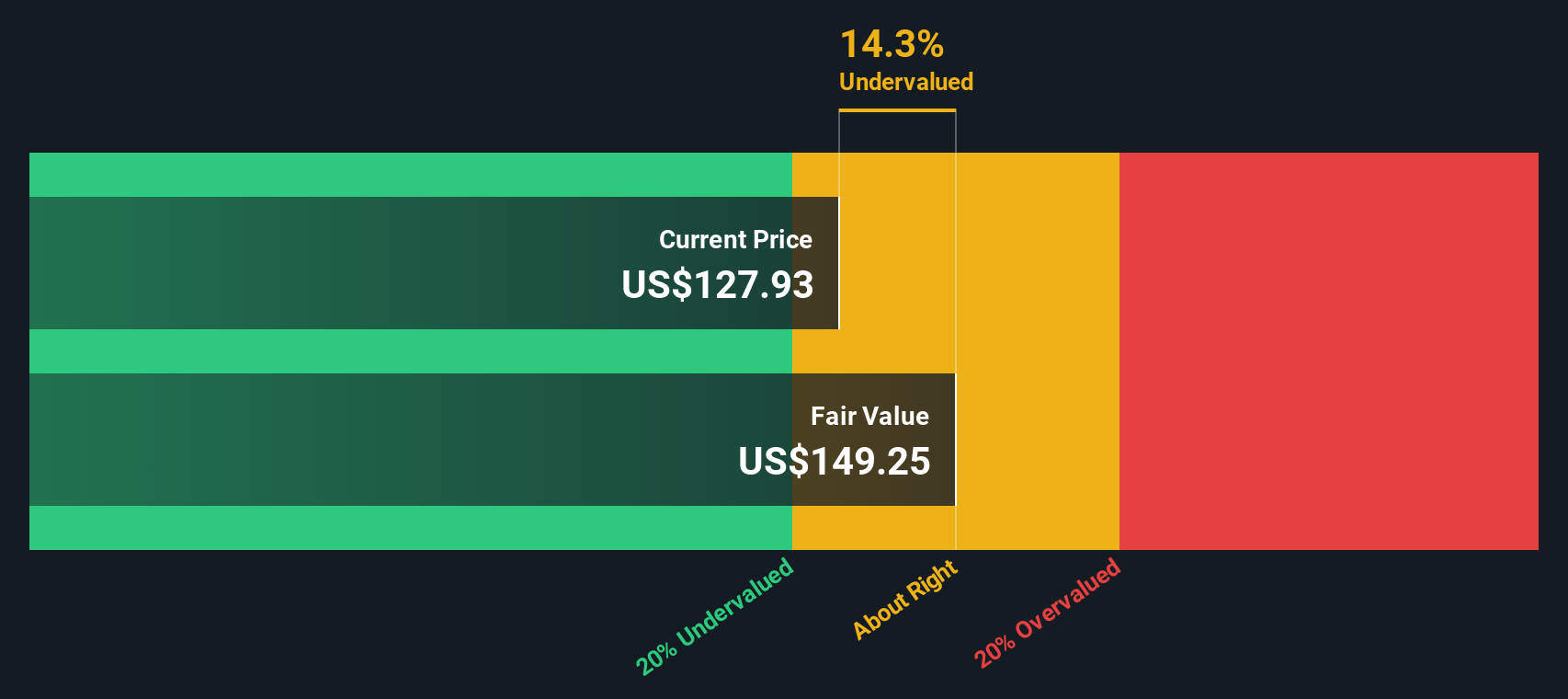

A Discounted Cash Flow model estimates what a company is worth by projecting its future cash flows and discounting them back to today in dollar terms. For Vertiv Holdings Co, the model used is a 2 Stage Free Cash Flow to Equity approach, starting from last twelve months free cash flow of about $1.36 billion.

Analysts and internal estimates expect this free cash flow to rise steadily, with projections reaching roughly $4.03 billion by 2029 and continuing to grow thereafter, supported by strong demand for data center and AI infrastructure. Simply Wall St uses analyst forecasts for the next few years, then extrapolates growth further out to build a 10 year cash flow profile before applying a discount rate to reflect risk and the time value of money.

On this basis, the intrinsic value for Vertiv comes out at around $214.13 per share, implying the stock trades at about an 11.7% discount to its estimated fair value. In other words, the DCF suggests Vertiv is moderately undervalued rather than fully priced.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Vertiv Holdings Co is undervalued by 11.7%. Track this in your watchlist or portfolio, or discover 906 more undervalued stocks based on cash flows.

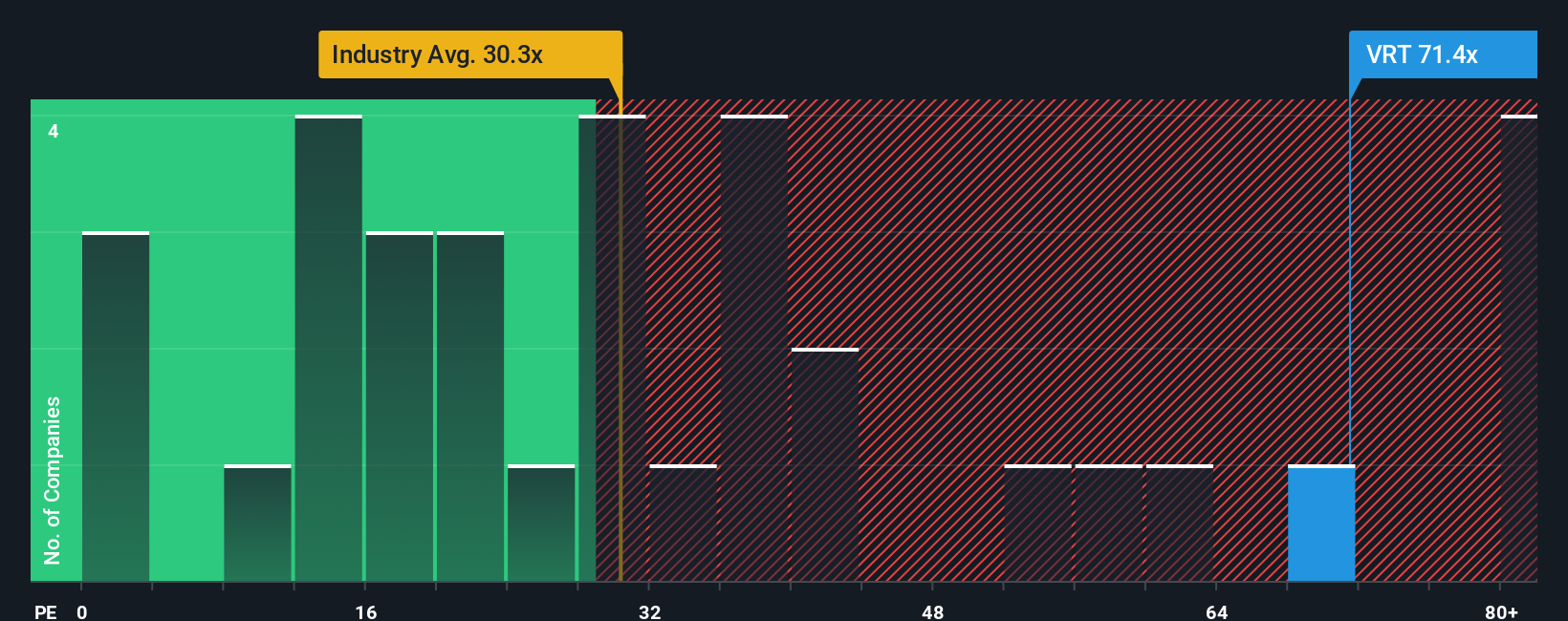

Approach 2: Vertiv Holdings Co Price vs Earnings

For profitable companies like Vertiv, the price to earnings ratio is often the most intuitive yardstick, because it links what investors pay today directly to the profits the business is already generating. A higher growth outlook and lower perceived risk usually justify a higher PE, while slower or more uncertain growth tends to cap what the market is willing to pay.

Vertiv currently trades on a PE of about 69.88x, which is more than double the Electrical industry average of roughly 31.31x and also well above the peer group average of around 37.71x. On the surface, that kind of premium suggests the market is already baking in very strong growth and relatively low risk.

To put that into better context, Simply Wall St uses a proprietary Fair Ratio, which estimates the PE a company should trade on after accounting for its earnings growth profile, margins, industry, market cap and specific risks. In Vertiv’s case, the Fair PE Ratio is 57.96x. This means the current multiple sits notably above what those fundamentals would justify and points to a degree of overvaluation on this measure.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Vertiv Holdings Co Narrative

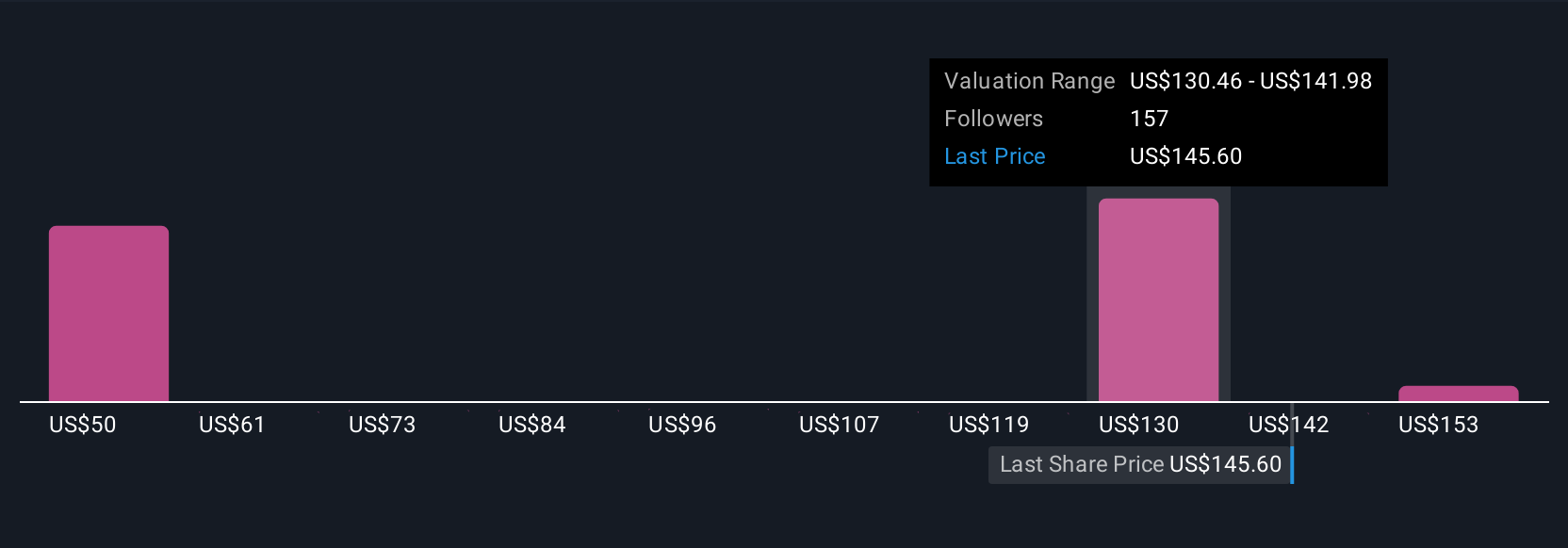

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple framework on Simply Wall St’s Community page where you connect your view of Vertiv’s story to concrete forecasts for its future revenue, earnings and margins. You can then link those forecasts to a Fair Value you can compare with today’s price to decide whether to buy, hold or sell. The platform keeps your Narrative updated as new news or earnings arrive. One investor might build a bullish Vertiv Narrative that assumes faster revenue growth, improving margins and a higher future PE in order to justify a Fair Value closer to the upper analyst range around $173 or the latest Fair Value estimate of $194.63. A more cautious investor might plug in slower growth, more margin pressure and a lower future PE that supports a Fair Value nearer the most conservative target of $119. Both perspectives can be valid as long as the story, the numbers and the resulting Fair Value stay logically linked.

Do you think there's more to the story for Vertiv Holdings Co? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:VRT

Vertiv Holdings Co

Designs, manufactures, and services critical digital infrastructure technologies and life cycle services for data centers, communication networks, and commercial and industrial environments in the Americas, the Asia Pacific, Europe, the Middle East, and Africa.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

53 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15081.9% undervalued

47 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4727.3% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

53 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative