Advertisement

- United States

- /

- Aerospace & Defense

- /

- NYSE:TDG

Is TransDigm Group’s Rising Leverage Reshaping Its Capital Allocation Story for TDG Investors?

Simply Wall St

Reviewed by Sasha Jovanovic

- In recent days, TransDigm Group saw analysts express caution following higher debt levels and rising interest expenses after its latest debt transactions and a substantial special dividend payout. While the company's overall business outlook remains favorable, analysts and investors are now closely examining its financial leverage and capital allocation decisions amid insider selling activity.

- TransDigm's recent capital moves highlight how its strong free cash flow and historic profitability may give it room to manage higher leverage, but also increase focus on how debt and shareholder returns could shape its long-term earnings trajectory.

- We'll explore how heightened attention to financial leverage and debt-related risks may influence the investment narrative for TransDigm Group.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

TransDigm Group Investment Narrative Recap

To be a shareholder in TransDigm Group, you generally need to believe in the durability of its proprietary aerospace parts business, driven by recurring aftermarket demand and disciplined capital allocation. The recent increase in debt tied to special dividends and the resulting analyst caution do not appear to change the short-term catalyst, which remains robust aerospace aftermarket activity; however, they do raise the profile of leverage as the most immediate risk to watch. For now, the focus remains on whether continued cash generation will comfortably offset higher interest expenses and support near-term earnings growth.

The Board's decision in August to authorize a special cash dividend of US$90.00 per share stands out as most relevant in light of increased leverage, linking current capital returns directly to the present risk of higher interest payments. This move has put greater scrutiny on the company's debt management and its potential impact on future shareholder value, aligning closely with the central catalyst investors are tracking: ongoing strength in aftermarket revenue as airlines keep fleets in service longer and parts demand remains elevated.

Yet, a key detail that could shift sentiment for investors is whether higher interest costs will ultimately...

Read the full narrative on TransDigm Group (it's free!)

TransDigm Group's outlook anticipates $10.8 billion in revenue and $2.5 billion in earnings by 2028. This implies an 8.0% annual revenue growth rate and an increase in earnings of $0.7 billion from the current $1.8 billion.

Uncover how TransDigm Group's forecasts yield a $1586 fair value, a 22% upside to its current price.

Exploring Other Perspectives

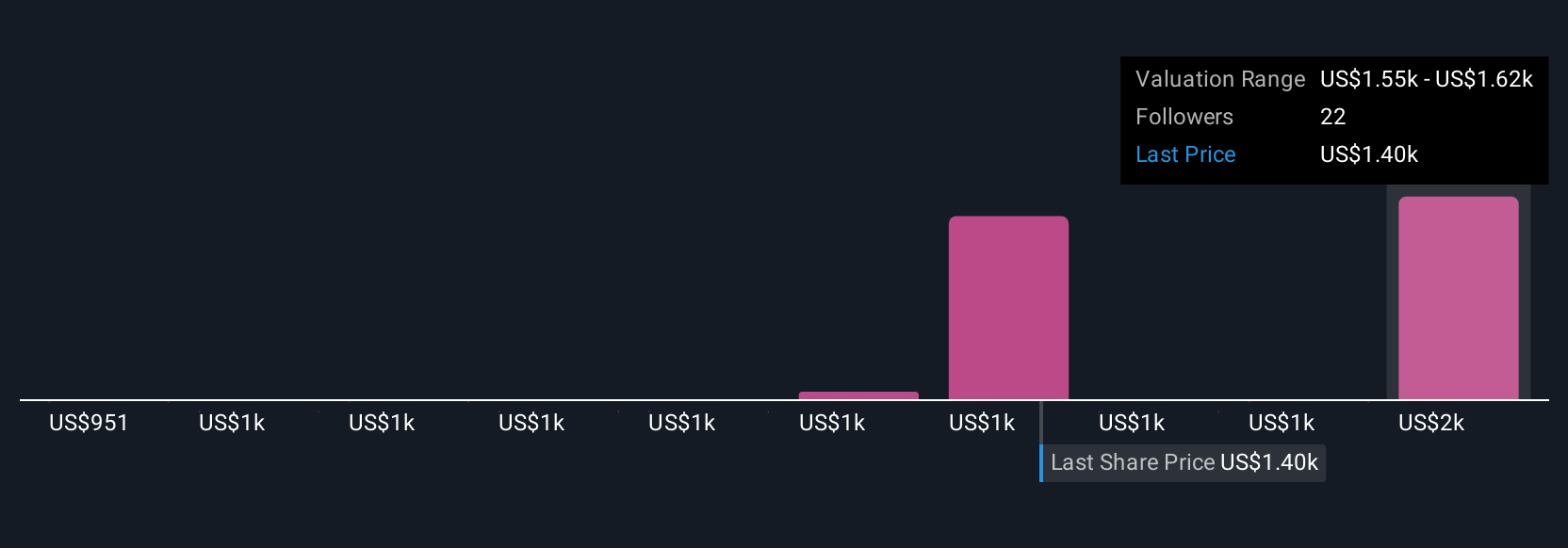

Six members of the Simply Wall St Community have valued TransDigm between US$951 and US$1,586 per share. With such varied outlooks, considering how increased debt and interest expense risk may affect long-term earnings could be critical, so it is worth reviewing these perspectives.

Explore 6 other fair value estimates on TransDigm Group - why the stock might be worth as much as 22% more than the current price!

Build Your Own TransDigm Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your TransDigm Group research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free TransDigm Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate TransDigm Group's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TransDigm Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TDG

TransDigm Group

Designs, produces, and supplies aircraft components in the United States and internationally.

Low risk with limited growth.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.7% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|93.3% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|18.7% undervalued

GM

Community Contributor