Advertisement

- United States

- /

- Building

- /

- NYSE:SSD

We Discuss Why Simpson Manufacturing Co., Inc.'s (NYSE:SSD) CEO May Deserve A Higher Pay Packet

Key Insights

- Simpson Manufacturing will host its Annual General Meeting on 6th of May

- Salary of US$900.0k is part of CEO Mike Olosky's total remuneration

- Total compensation is 47% below industry average

- Simpson Manufacturing's total shareholder return over the past three years was 49% while its EPS grew by 7.7% over the past three years

Shareholders will probably not be disappointed by the robust results at Simpson Manufacturing Co., Inc. (NYSE:SSD) recently and they will be keeping this in mind as they go into the AGM on 6th of May. This would also be a chance for them to hear the board review the financial results, discuss future company strategy to further improve the business and vote on any resolutions such as executive remuneration. Here is our take on why we think CEO compensation is fair and may even warrant a raise.

See our latest analysis for Simpson Manufacturing

How Does Total Compensation For Mike Olosky Compare With Other Companies In The Industry?

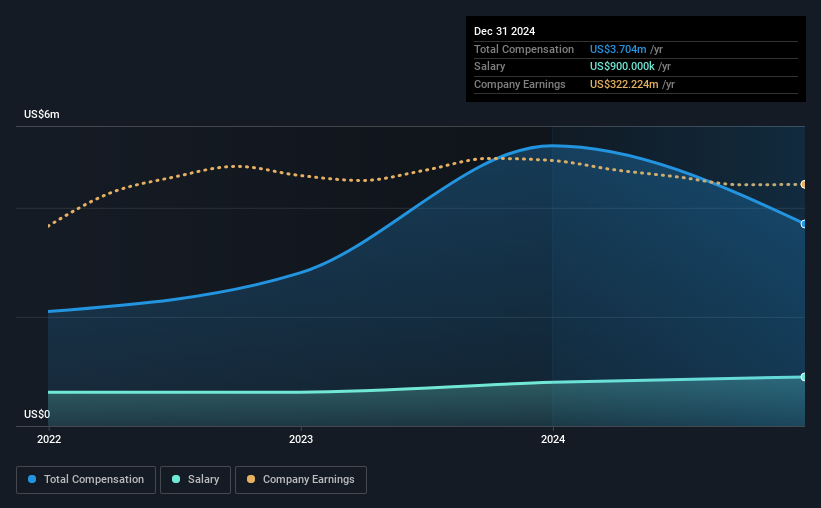

Our data indicates that Simpson Manufacturing Co., Inc. has a market capitalization of US$6.4b, and total annual CEO compensation was reported as US$3.7m for the year to December 2024. That's a notable decrease of 28% on last year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at US$900k.

On comparing similar companies from the American Building industry with market caps ranging from US$4.0b to US$12b, we found that the median CEO total compensation was US$7.0m. This suggests that Mike Olosky is paid below the industry median. Furthermore, Mike Olosky directly owns US$185k worth of shares in the company.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | US$900k | US$800k | 24% |

| Other | US$2.8m | US$4.3m | 76% |

| Total Compensation | US$3.7m | US$5.1m | 100% |

Speaking on an industry level, nearly 16% of total compensation represents salary, while the remainder of 84% is other remuneration. It's interesting to note that Simpson Manufacturing pays out a greater portion of remuneration through salary, compared to the industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

Simpson Manufacturing Co., Inc.'s Growth

Over the past three years, Simpson Manufacturing Co., Inc. has seen its earnings per share (EPS) grow by 7.7% per year. The trailing twelve months of revenue was pretty much the same as the prior period.

We'd prefer higher revenue growth, but the modest improvement in EPS is good. Considering these factors we'd say performance has been pretty decent, though not amazing. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Simpson Manufacturing Co., Inc. Been A Good Investment?

Most shareholders would probably be pleased with Simpson Manufacturing Co., Inc. for providing a total return of 49% over three years. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

In Summary...

The company's overall performance, while not bad, could be better. If it manages to keep up the current streak, CEO remuneration could well be one of shareholders' least concerns. Instead, investors might be more interested in discussions that would help manage their longer-term growth expectations such as company business strategies and future growth potential.

So you may want to check if insiders are buying Simpson Manufacturing shares with their own money (free access).

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:SSD

Simpson Manufacturing

Through its subsidiaries, designs, engineers, manufactures, and sells structural solutions for wood, concrete, and steel connections in North America, Europe, and the Asia Pacific.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor