Advertisement

- United States

- /

- Aerospace & Defense

- /

- NYSE:SPCE

Is Virgin Galactic Holdings (NYSE:SPCE) Weighed On By Its Debt Load?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Virgin Galactic Holdings, Inc. (NYSE:SPCE) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Virgin Galactic Holdings

What Is Virgin Galactic Holdings's Net Debt?

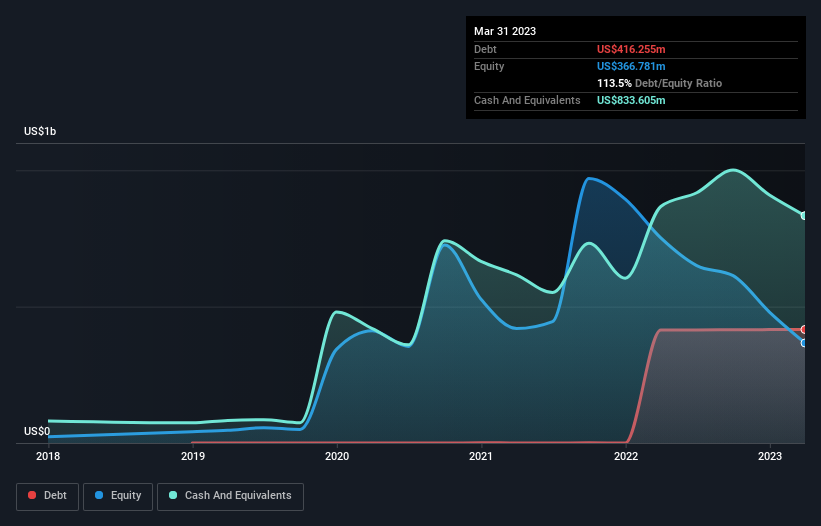

The chart below, which you can click on for greater detail, shows that Virgin Galactic Holdings had US$416.3m in debt in March 2023; about the same as the year before. But it also has US$833.6m in cash to offset that, meaning it has US$417.4m net cash.

How Strong Is Virgin Galactic Holdings' Balance Sheet?

The latest balance sheet data shows that Virgin Galactic Holdings had liabilities of US$190.8m due within a year, and liabilities of US$475.9m falling due after that. On the other hand, it had cash of US$833.6m and US$2.70m worth of receivables due within a year. So it can boast US$169.6m more liquid assets than total liabilities.

This excess liquidity suggests that Virgin Galactic Holdings is taking a careful approach to debt. Given it has easily adequate short term liquidity, we don't think it will have any issues with its lenders. Succinctly put, Virgin Galactic Holdings boasts net cash, so it's fair to say it does not have a heavy debt load! There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Virgin Galactic Holdings can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Over 12 months, Virgin Galactic Holdings made a loss at the EBIT level, and saw its revenue drop to US$2.4m, which is a fall of 34%. That makes us nervous, to say the least.

So How Risky Is Virgin Galactic Holdings?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And we do note that Virgin Galactic Holdings had an earnings before interest and tax (EBIT) loss, over the last year. Indeed, in that time it burnt through US$468m of cash and made a loss of US$566m. However, it has net cash of US$417.4m, so it has a bit of time before it will need more capital. Overall, its balance sheet doesn't seem overly risky, at the moment, but we're always cautious until we see the positive free cash flow. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example Virgin Galactic Holdings has 4 warning signs (and 1 which is significant) we think you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:SPCE

Virgin Galactic Holdings

An aerospace and space travel company, focuses on the development, manufacture, and operation of spaceships and related technologies.

High growth potential and good value.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor