Advertisement

- United States

- /

- Trade Distributors

- /

- NYSE:QXO

QXO (QXO): Exploring Valuation After Analyst Initiations and High-Profile Endorsement Boost Interest

Simply Wall St

Reviewed by Kshitija Bhandaru

QXO (QXO) has quickly become a topic of conversation, as recent major analyst initiations and a public endorsement from a well-known commentator have put the company’s strategy and leadership in the spotlight.

See our latest analysis for QXO.

After surging into focus with analyst upgrades and a high-profile endorsement, QXO’s momentum appears to be building. The company’s latest share price sits at $20.23, with a year-to-date share price return of 0.32%. Looking at the bigger picture, the stock has delivered a 1-year total shareholder return of 0.45%. This is a solid start as investors weigh its strategy and sector position.

If you’re interested in what other industry leaders are doing, now’s the perfect moment to broaden your perspective and discover fast growing stocks with high insider ownership

With analyst targets suggesting significant upside, QXO’s recent muted gains raise a key question: Is the market underestimating the company’s true value, or has future growth already been fully priced in?

Price-to-Sales Ratio of 7x: Is it justified?

At $20.23 per share, QXO trades at a price-to-sales ratio of 7x, noticeably higher than its industry and peer averages. This valuation points to investors having lofty expectations for future growth.

The price-to-sales ratio is a metric that compares a company’s market capitalization to its total revenues. It offers insight into how much investors are willing to pay for every dollar of sales. This is particularly relevant for companies like QXO that are not yet profitable, as it removes the impact of negative earnings.

QXO’s significant premium to both the US Trade Distributors industry average of 1.1x and the peer average of 3x signals the market may already be pricing in robust growth or unique strategic advantages. However, the estimated fair price-to-sales ratio stands at 5.7x. This means the current price implies expectations that are even higher than this baseline level, and the stock may face pressure if growth targets are missed.

Explore the SWS fair ratio for QXO

Result: Price-to-Sales of 7x (OVERVALUED)

However, it is important to note that slowing revenue growth or persistent losses could quickly dampen investor enthusiasm and challenge current lofty valuations.

Find out about the key risks to this QXO narrative.

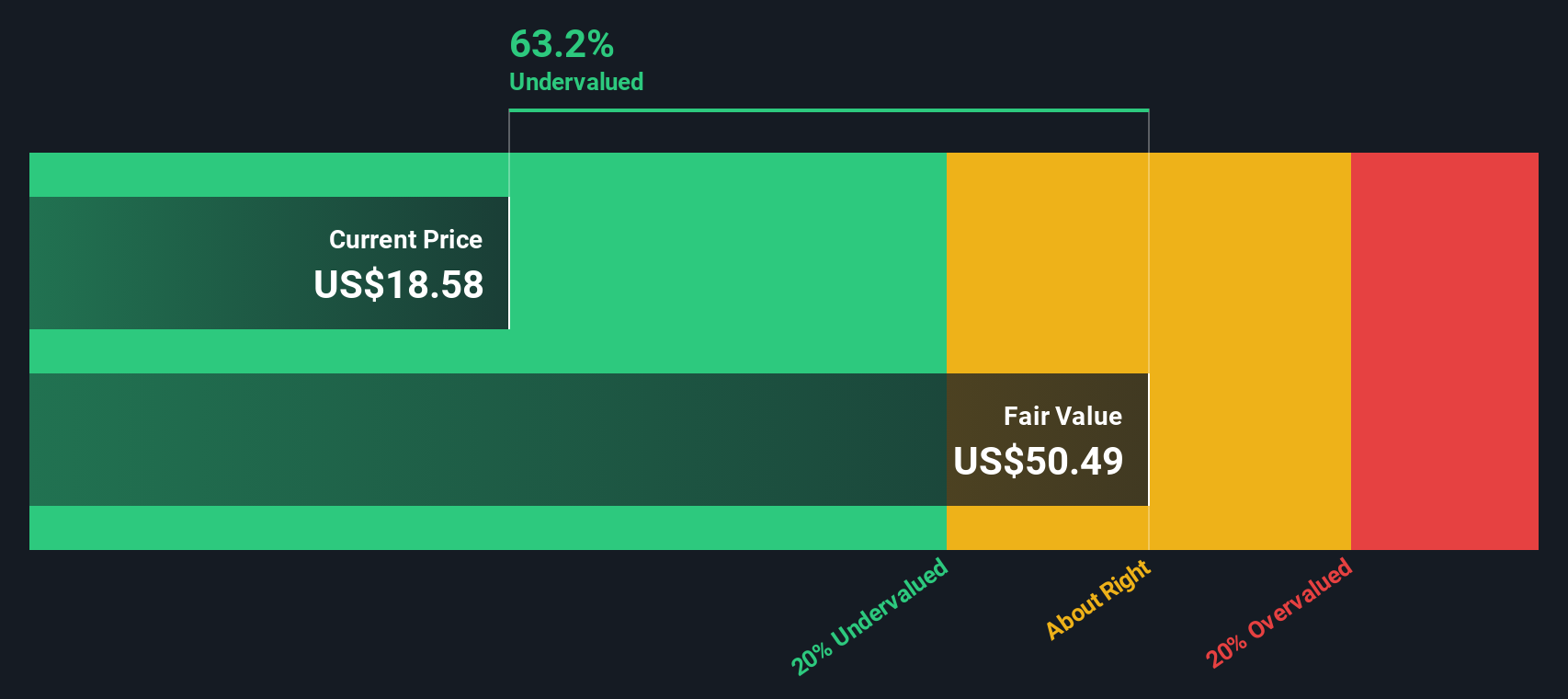

Another View: Discounted Cash Flow Shows Upside

While the price-to-sales ratio suggests QXO is expensive compared to peers, our DCF model offers a different perspective. On this measure, the current share price of $20.23 is actually 61.8% below the estimated fair value of $52.95, indicating a significant potential upside. Can these divergent signals both be correct?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out QXO for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own QXO Narrative

If you see opportunity where others don’t, or prefer a hands-on approach to research, you can dive in and build your own narrative in just minutes. Do it your way.

A great starting point for your QXO research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Make sure you don’t miss out on market opportunities. Let Simply Wall Street’s powerful screeners help you target your next winning investment before others catch on.

- Tap into future trends by uncovering these 24 AI penny stocks at the forefront of artificial intelligence innovation and real-world adoption across industries.

- Boost your passive income strategy by accessing these 19 dividend stocks with yields > 3% that offer attractive yields and the potential for steady returns over time.

- Stay ahead of the curve and spark your portfolio’s growth with these 3567 penny stocks with strong financials that combine solid fundamentals and high upside potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if QXO might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:QXO

QXO

Distributes roofing, waterproofing, and other building products in the United States.

High growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor