Advertisement

- United States

- /

- Machinery

- /

- NYSE:OTIS

What Otis Worldwide (OTIS)'s Strong Q3 Service Margin Growth Means For Shareholders

Simply Wall St

Reviewed by Sasha Jovanovic

- Otis Worldwide reported higher-than-expected Q3 earnings, with net sales rising 4% year-over-year and adjusted EPS growing 9.4%, surpassing analyst forecasts.

- This performance was driven by robust organic service sales and improvement in service operating profit margins, highlighting the company's expanding strength in its core service segment.

- We’ll explore how Otis Worldwide’s strong margin expansion in services may influence the company’s future growth narrative and outlook.

Find companies with promising cash flow potential yet trading below their fair value.

Otis Worldwide Investment Narrative Recap

To be comfortable as a shareholder in Otis Worldwide, you need to see long-term value in the company’s global installed base and its ability to generate recurring, high-margin service revenue despite ongoing sector pressures. While the recent Q3 results underscore continued margin expansion in services, the biggest short-term catalyst, modernization momentum, remains largely unchanged, and the main risk around declining new equipment demand in China is still a material concern.

Among recent developments, Otis’s launch of new Arise™ MOD Prime and MOD Plus modernization solutions in Europe stands out. This move supports the service margin momentum highlighted in the latest earnings and ties directly to the broader catalyst of aging infrastructure driving long-term growth in service and modernization revenue streams.

However, investors should keep in mind that despite margin progress, weakness in new equipment sales tied to China’s ongoing struggles remains a significant risk, especially if...

Read the full narrative on Otis Worldwide (it's free!)

Otis Worldwide's outlook anticipates $16.4 billion in revenue and $1.9 billion in earnings by 2028. This projection is based on a 5.0% annual revenue growth rate and a $0.4 billion increase in earnings from the current $1.5 billion.

Uncover how Otis Worldwide's forecasts yield a $102.29 fair value, a 13% upside to its current price.

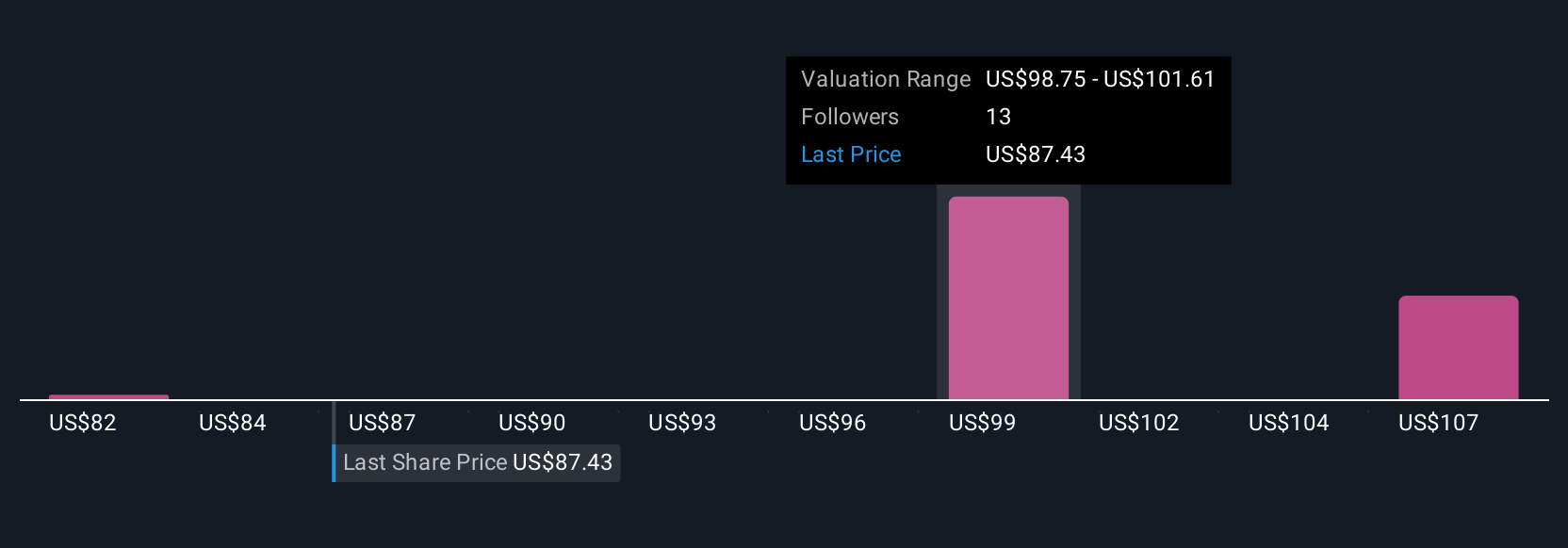

Exploring Other Perspectives

Five members of the Simply Wall St Community estimate Otis’s fair value between US$81.56 and US$109.62. While some anticipate strong upside driven by service and modernization growth, persistent headwinds in new installations still weigh on sentiment, making it important to consider several viewpoints before making up your mind.

Explore 5 other fair value estimates on Otis Worldwide - why the stock might be worth 10% less than the current price!

Build Your Own Otis Worldwide Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Otis Worldwide research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Otis Worldwide research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Otis Worldwide's overall financial health at a glance.

Curious About Other Options?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- These 15 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Outshine the giants: these 27 early-stage AI stocks could fund your retirement.

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:OTIS

Otis Worldwide

Engages in manufacturing, installation, and servicing of elevators and escalators in the United States, China, and internationally.

Fair value second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor