Advertisement

- United States

- /

- Machinery

- /

- NYSE:NPO

How Enpro's Above-Consensus Revenue and Upbeat Guidance Will Impact NPO Investors

Simply Wall St

Reviewed by Sasha Jovanovic

- Enpro recently reported quarterly revenues of US$286.6 million, marking a 9.9% year-on-year increase and surpassing analyst forecasts by 3.6%.

- Despite reporting solid sales growth and profitability alongside continued investment in key capabilities, the company maintained a positive outlook with EBITDA guidance slightly above consensus expectations.

- We'll explore how Enpro's above-consensus revenue growth and confident guidance may influence its longer-term investment narrative.

We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Enpro Investment Narrative Recap

To be a shareholder in Enpro today, one generally needs to believe in the company’s ability to capture long-term value through its focus on engineered solutions and growth in resilient end markets, despite exposure to cyclical industries and associated volatility. The recent revenue beat and confident EBITDA guidance modestly reinforce the company’s case, but do not fundamentally shift the biggest short-term catalyst, momentum in end-market demand, or the primary risk of ongoing margin pressure from elevated investment and operating costs.

The most relevant recent announcement is Enpro’s raised full-year revenue growth guidance, now set at 7%-8% for 2025. This uptick, pointing to contributions from acquisitions, aligns with the company’s ambitions in scaling its portfolio but also brings execution and integration risk to the forefront as growth initiatives ramp up. Yet, it is important for investors to consider that alongside this guidance, disciplined capital allocation and cost control remain critical in shaping whether these efforts translate to sustained margin improvement.

In contrast, the lingering challenge of margin pressure, particularly from rising corporate expenses and continued investment, is one issue that investors should be watching closely, especially as...

Read the full narrative on Enpro (it's free!)

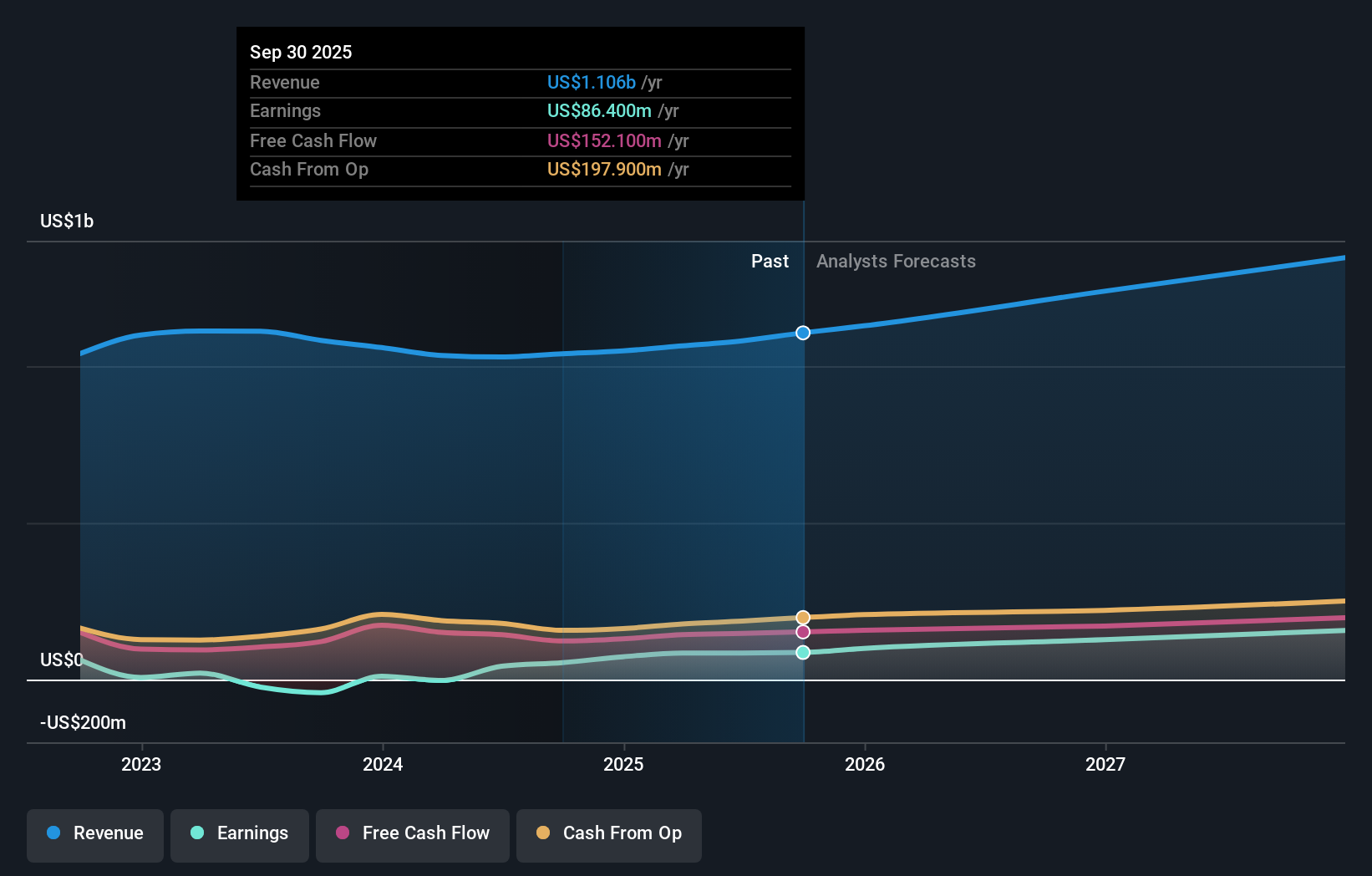

Enpro's narrative projects $1.3 billion in revenue and $176.2 million in earnings by 2028. This requires 5.7% yearly revenue growth and an earnings increase of $91.6 million from the current earnings of $84.6 million.

Uncover how Enpro's forecasts yield a $249.00 fair value, a 12% upside to its current price.

Exploring Other Perspectives

All Simply Wall St Community fair value estimates for Enpro cluster at US$249 per share, offering a single viewpoint based on member forecasts. While these perspectives are tightly grouped, the ongoing pressure from rising operating costs as Enpro expands remains a key issue that could influence future market sentiment; review other community insights for diverse takes.

Explore another fair value estimate on Enpro - why the stock might be worth as much as 12% more than the current price!

Build Your Own Enpro Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Enpro research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Enpro research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Enpro's overall financial health at a glance.

Searching For A Fresh Perspective?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 35 companies in the world exploring or producing it. Find the list for free.

- Outshine the giants: these 25 early-stage AI stocks could fund your retirement.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Enpro might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:NPO

Enpro

An industrial technology company, design, develops, manufactures, and markets proprietary, value-added products and solutions to safeguard critical environments in the United States, Europe, Asia Pacific, and internationally.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

930 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative