Advertisement

- United States

- /

- Machinery

- /

- NYSE:GRC

How Record Sales and Debt Reduction Could Shape Gorman-Rupp's (GRC) Outlook for 2025

Simply Wall St

Reviewed by Simply Wall St

- Gorman-Rupp recently reported record second-quarter sales, earnings per share, and order levels, with growth driven by strong infrastructure spending and increased demand for flood control and storm water management solutions.

- The company also reduced its debt by US$30 million in the first half of 2025 and credits its primarily U.S.-based supply chain for mitigating tariff concerns.

- Let's explore how Gorman-Rupp's robust order trends and substantial debt reduction shape its investment narrative this year.

These 10 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

What Is Gorman-Rupp's Investment Narrative?

To see a case for Gorman-Rupp in 2025, you need to believe not just in steady industrial spending but in the stickiness of demand for flood and water infrastructure solutions. The company’s record Q2 results, which beat previous analysis, signal stronger momentum than the market had priced in, especially as robust order books and backlog help support near-term visibility. Debt reduction by US$30 million over six months improves financial flexibility, slightly reducing the risk profile that previously concerned some investors due to Gorman-Rupp’s high leverage. The market’s muted response (with recent price returns mostly flat except for a jump over 90 days) suggests expectations for continued growth may have already been rising. Short-term catalysts are now firmly tied to infrastructure spending and weather-driven demand, but risks remain around the speed of order conversion and the sustainability of those elevated order levels. The news event does shift the narrative: improved balance sheet health and order momentum make concerns over debt and revenue growth slowdown somewhat less immediate, but competition and industrial cyclicality are persistent factors. However, supply chain advantages do not entirely eliminate margin risks linked to global competition.

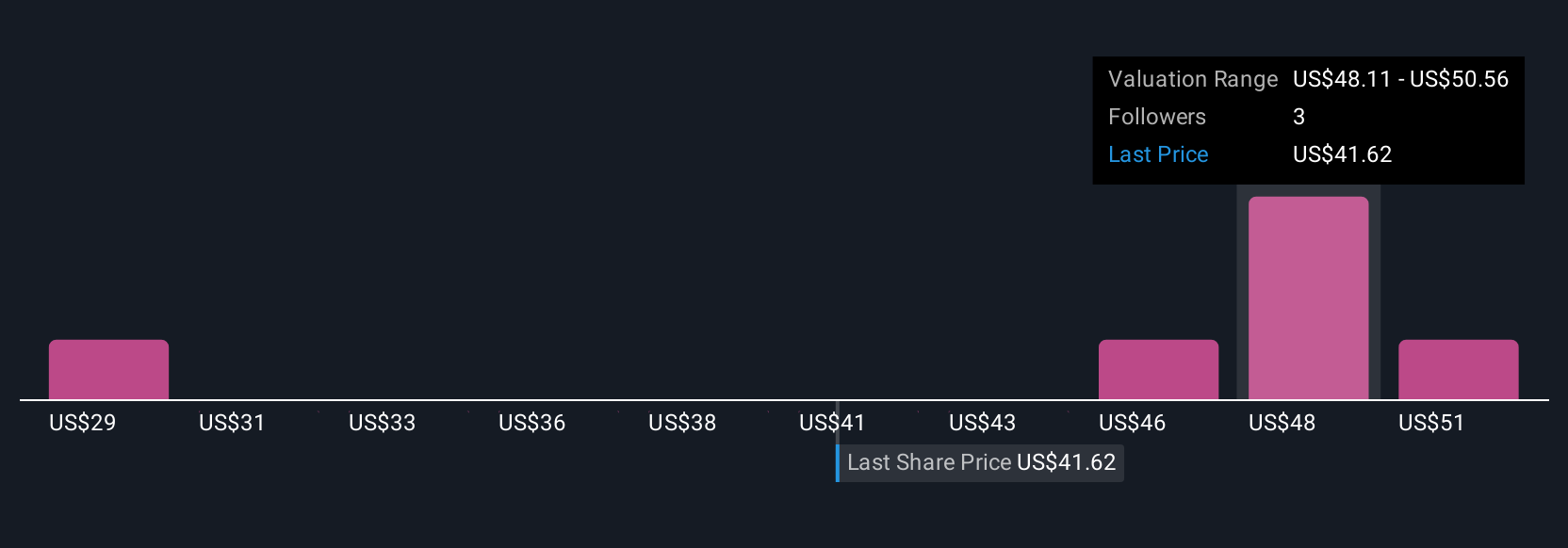

Despite retreating, Gorman-Rupp's shares might still be trading 9% above their fair value. Discover the potential downside here.Exploring Other Perspectives

Explore 4 other fair value estimates on Gorman-Rupp - why the stock might be worth as much as 23% more than the current price!

Build Your Own Gorman-Rupp Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Gorman-Rupp research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Gorman-Rupp research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Gorman-Rupp's overall financial health at a glance.

Ready For A Different Approach?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 29 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Explore 25 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:GRC

Gorman-Rupp

Designs, manufactures, and sells pumps and pump systems in the United States and internationally.

Solid track record established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|27.6% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|22.1% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|60.0% undervalued

ME

Community Contributor