Advertisement

- United States

- /

- Aerospace & Defense

- /

- NYSE:GE

How Should Investors View GE After Pentagon Calls to Ramp Up Missile Production?

Simply Wall St

Reviewed by Bailey Pemberton

If you have been watching General Electric stock recently, you are not alone. With the closing price hovering around $299.45 and some jaw-dropping returns front and center, GE has surprised many investors. In the past week, it ticked up another 0.8%, stretched 8.7% higher over 30 days, and the year-to-date gain is an electric 77.6%. If you held shares for the last year, you have seen a 63.8% return, but over three and five years the numbers get downright dizzying, with gains of 637.7% and 825.0% respectively.

Most of that momentum has been powered by growing optimism around GE Aerospace, following several newsworthy developments. Defense spending has come into focus, as the Pentagon called for missile suppliers like GE to step up production and Defense Secretary Hegseth ordered an urgent gathering of military leaders. Add in GE’s fresh labor agreement with striking workers, and news that India is lining up a $1B order for GE’s jet engines, and the business case for long-term growth certainly seems compelling.

With all this excitement, though, is GE’s stock really undervalued? According to our six-point valuation check, GE scores 0 out of 6. This means it is not undervalued by any of our metrics. So should you hang on tight, cash out, or look for bargains elsewhere?

Let’s dig into the popular methods analysts use to assess a stock’s value. And stick around, because there may be an even smarter way to gauge what GE is really worth, coming up at the end.

General Electric scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

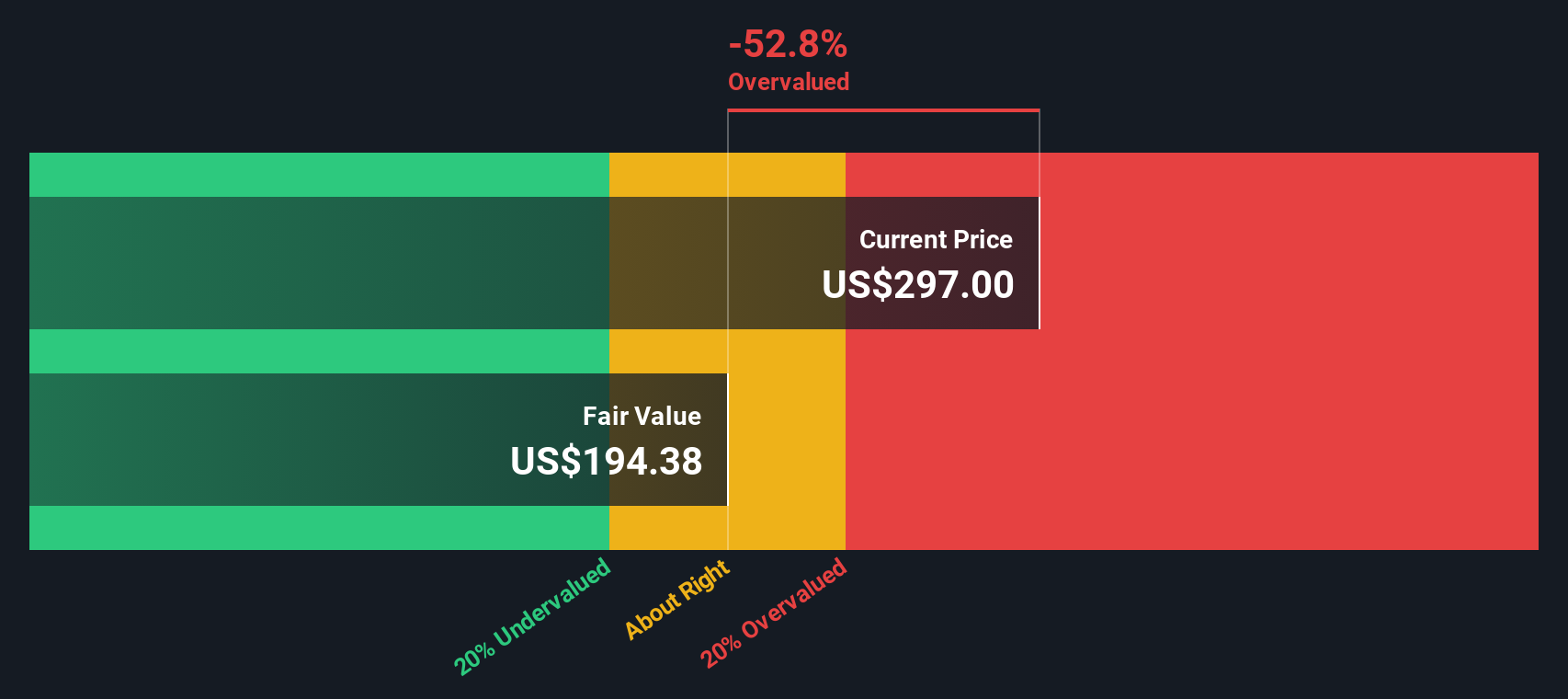

Approach 1: General Electric Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and discounting them back to today's dollars. This approach helps investors understand what the business might be worth, based on its ability to generate cash in the years ahead.

For General Electric, the most recent free cash flow stands at approximately $5.55 Billion. Analysts provide detailed forecasts up to five years, and further projections out to 2035 are extrapolated by Simply Wall St. According to these figures, GE’s cash flows are expected to steadily climb, reaching over $13.05 Billion by 2035. Notably, the forecast for 2029 shows a projected free cash flow of around $10.10 Billion.

Based on these projections and using the 2 Stage Free Cash Flow to Equity model, GE’s intrinsic value comes out to $194.88 per share. With the current market price at $299.45, this DCF assessment suggests that GE stock is about 53.7% overvalued.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests General Electric may be overvalued by 53.7%. Find undervalued stocks or create your own screener to find better value opportunities.

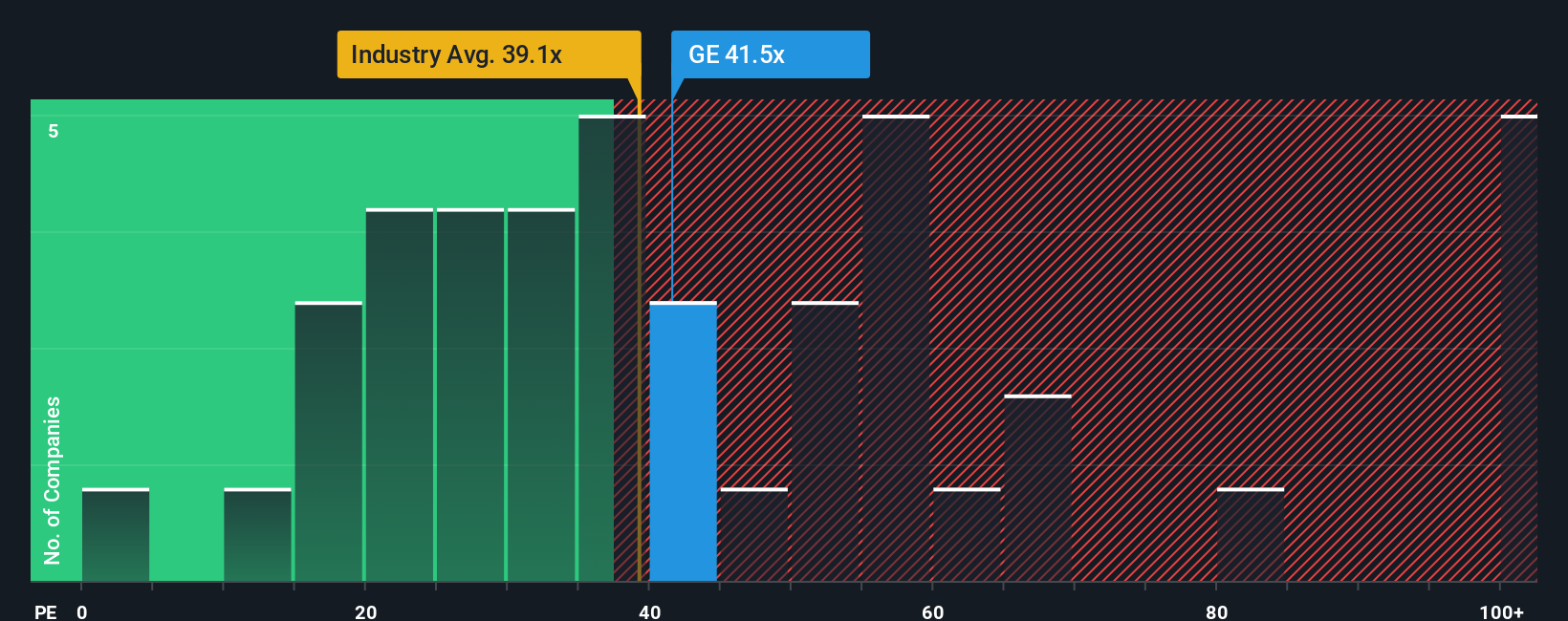

Approach 2: General Electric Price vs Earnings

The Price-to-Earnings (PE) ratio is one of the most common tools for valuing profitable companies like General Electric. It gives investors a sense of how much they are paying for each dollar of earnings, making it a useful metric for comparing similar businesses across an industry.

Growth expectations and risk both play a key role in what is considered a "normal" or "fair" PE ratio. Companies with strong earnings growth and lower risks typically justify higher PE multiples, while slower-growth or riskier firms are valued less generously by the market.

Currently, General Electric trades at a PE ratio of 41.87x. That is higher than the Aerospace & Defense industry average of 39.08x, and it also sits above the average for similar peers at 27.10x. On the surface, this suggests that GE is priced at a premium compared to broader benchmarks, which could raise valuation concerns for potential buyers.

However, Simply Wall St's proprietary "Fair Ratio" model gives us a more nuanced perspective. The Fair Ratio for GE is 35.23x, calculated by weighing company-specific factors such as expected earnings growth, profit margins, market capitalization, sector trends, and unique risks. This tailored approach goes beyond simple peer or industry comparison and produces a valuation multiple that is personalized for GE's real prospects and market realities.

With GE's actual PE ratio sitting notably above its Fair Ratio, the numbers point toward the stock being overvalued at today's price.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your General Electric Narrative

Earlier we mentioned that there's an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your personalized investment story, where you attach your outlook, assumptions, and expectations to a company’s future. This approach combines facts, forecasts, and your investment thesis into one actionable framework. Narratives link a company’s news and business story to concrete financial forecasts, like future revenue or profit margins, and then directly to a fair value. This empowers you to form your own opinion rather than relying only on the market consensus.

On Simply Wall St’s Community page, used by millions, Narratives are an easy, accessible tool that help you compare your Fair Value to the real-time share price, so you can quickly see if it may be time to buy, hold, or sell. They're updated automatically when new info arrives, so your view always reflects the latest news or results. For example, some investors believe GE’s next-gen engine programs, AI innovation, and rising defense orders will propel massive growth, setting a Narrative Fair Value as high as $343. Others, conscious of aviation cycles or margin pressures, land much lower, down to $266. Narratives make these perspectives clear, dynamic, and actionable.

Do you think there's more to the story for General Electric? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:GE

General Electric

General Electric Company, doing business as GE Aerospace, designs and produces commercial and defense aircraft engines, integrated engine components, electric power, and mechanical aircraft systems.

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.2% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|90.0% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.6% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|97.1% undervalued

AG

Community Contributor