Advertisement

- United States

- /

- Machinery

- /

- NYSE:CMI

Is Cummins Still a Bargain After 33.7% Share Price Surge in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

- Ever wondered if Cummins stock could be offering great value right now or if it's already priced for perfection? Let's dig into what really matters for investors looking for an edge.

- The share price has been on a tear this year, up 33.7% year-to-date and 31.1% over the past 12 months. This comes even after a modest pullback of -2.3% in the last week.

- What’s behind these big moves? Recent headlines have focused on Cummins’ push into clean energy solutions and new partnerships. These developments have investors buzzing about both its long-term growth story and how it stacks up against legacy competitors.

- The company's current valuation score is 3 out of 6, meaning it's seen as undervalued by half our standard checks. Next, we will break down how that score is calculated, but keep reading because we will also cover a fresh perspective on valuing Cummins that even the pros sometimes miss.

Approach 1: Cummins Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) analysis estimates a company's intrinsic value by projecting its future cash flows and discounting them back to today’s value. Essentially, it asks what Cummins’ future stream of cash is really worth in today’s dollars, giving investors a sense of whether the stock is a bargain or not.

For Cummins, the latest reported Free Cash Flow stands at $2.32 billion. According to analyst estimates, Free Cash Flow is projected to rise steadily over the next several years, topping $4.64 billion by the end of 2029. Beyond analyst forecasts, Simply Wall St extrapolates further, showing continued healthy growth and resilience over the next decade.

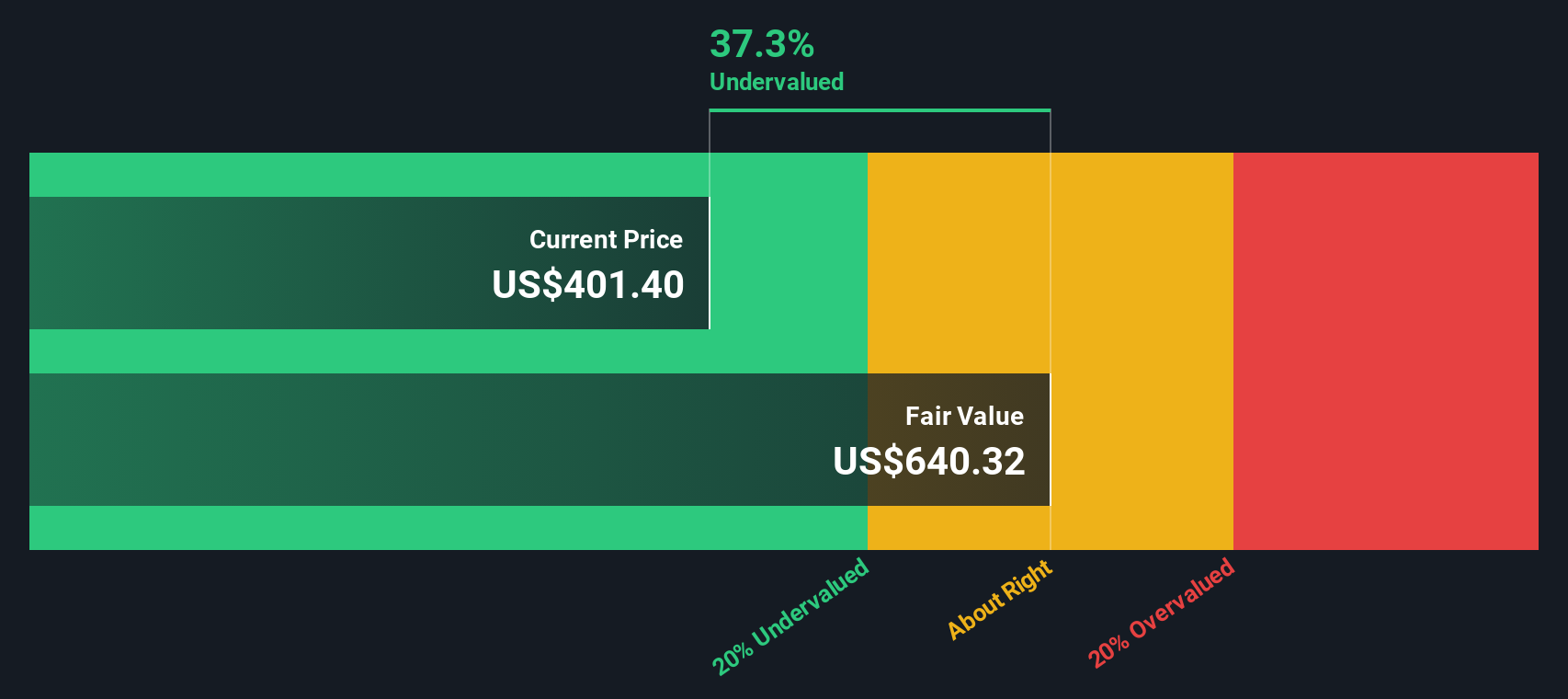

Factoring in these projections, the DCF model pegs Cummins’ estimated fair value at $637.98 per share. This figure suggests the stock is trading at a 27.1% discount compared to its intrinsic value. In plain terms, it is considered 27.1% undervalued right now by this method.

If you are confident that future cash flows will hold up, this DCF analysis points to meaningful potential upside for long-term investors who buy at the current market price.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Cummins is undervalued by 27.1%. Track this in your watchlist or portfolio, or discover 905 more undervalued stocks based on cash flows.

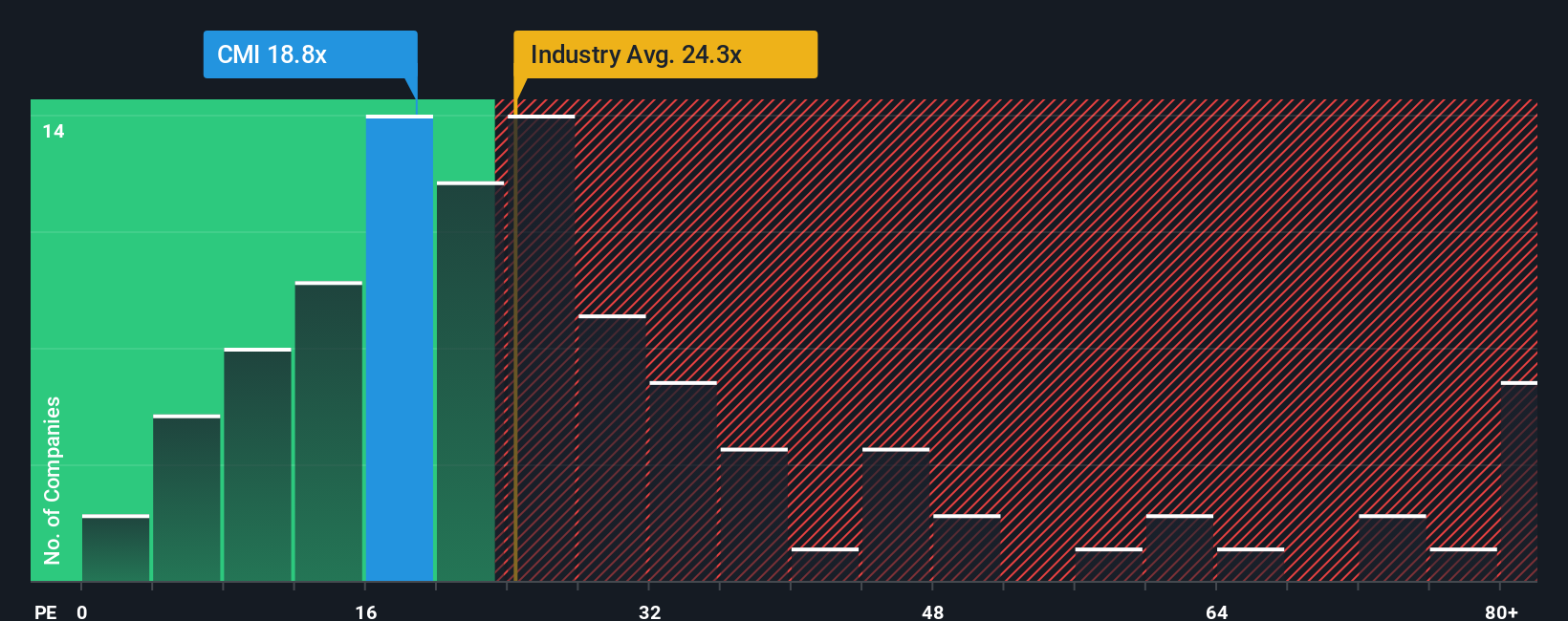

Approach 2: Cummins Price vs Earnings (P/E Ratio)

The Price-to-Earnings (P/E) ratio is a widely used valuation tool for profitable companies because it relates the market price of a stock to its earnings per share. For established businesses like Cummins, which has a consistent track record of profitability, the P/E ratio helps investors quickly compare relative value.

What’s considered a normal or fair P/E ratio is influenced by several factors, including growth expectations and risk levels. Companies growing earnings more rapidly often command higher P/Es, while increased risk or market uncertainty can have the opposite effect.

As of now, Cummins trades at a P/E ratio of 24.1x. This is just above the Machinery industry average of 23.2x and also sits higher than the average among its direct peers, which is 21.7x. On the surface, this might suggest Cummins is trading at a slight premium.

However, Simply Wall St’s proprietary “Fair Ratio” provides further insight. The Fair Ratio (33.5x) reflects what we would expect Cummins’ P/E to be when accounting for its specific growth outlook, industry landscape, profit margins, market cap, and company-specific risks. Unlike simple peer or industry comparisons, the Fair Ratio captures a wider set of company fundamentals and market drivers, giving a more complete picture of value.

Comparing the current 24.1x P/E to the Fair Ratio of 33.5x indicates that Cummins is trading well below its expected fair value based on these comprehensive factors. This suggests the market may be underestimating its prospects.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1416 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Cummins Narrative

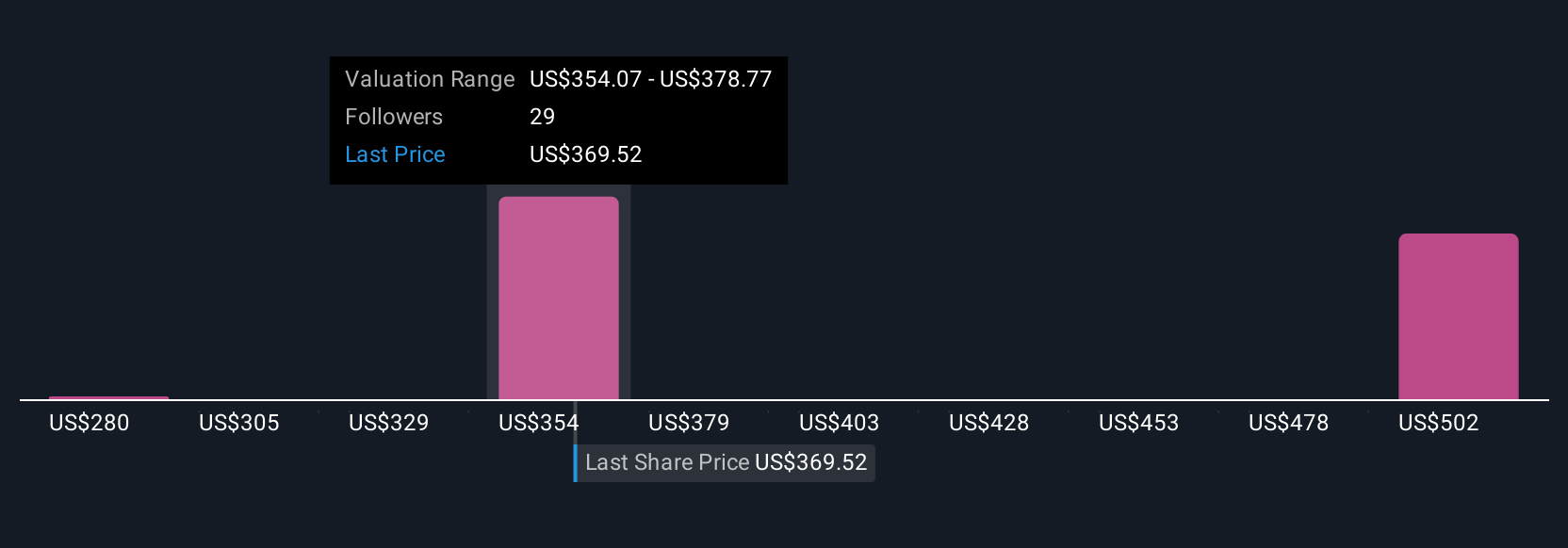

Earlier, we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your unique story about a company, where you connect your own expectations for Cummins’ future revenue, profit margins, or risks with a fair value estimate, giving genuine context to the numbers behind your investment decisions.

Instead of relying solely on traditional metrics, Narratives let you build a clear link between what you believe about a company and what that means for where its stock should trade. They are simple to try and available right now on Simply Wall St’s Community page, which is used by millions of investors looking to share and compare their views in real time.

By creating or following a Narrative, you can easily see how your financial outlook translates into a fair value and instantly compare that fair value with the current share price, helping you decide exactly when to buy or sell. Each Narrative automatically updates as new news or earnings are released, so your investment view stays fresh and relevant.

For Cummins, one investor might be bullish, using high future revenue and margin estimates to arrive at a fair value above $500, while another might be more cautious, expecting risks to drag fair value closer to $350.

Do you think there's more to the story for Cummins? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CMI

Outstanding track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor