Advertisement

- United States

- /

- Electrical

- /

- NYSE:BE

Will Bloom Energy's (BE) New Deal-Maker Shift Its Data Center Growth Trajectory?

Simply Wall St

Reviewed by Simply Wall St

- Earlier this month, Bloom Energy announced that Aaron Hoover, bringing more than 20 years of leadership experience in energy investment banking, has joined as head of business and corporate development, aiming to expand strategic partnerships and drive growth in clean energy markets, including data centers.

- Hoover’s expertise and connections across the energy sector, combined with Bloom’s ongoing push into scalable fuel cell solutions for AI-enabled data centers, may signal an intensified focus on capitalizing on evolving power demands in the technology sector.

- We’ll assess how the appointment of a proven energy dealmaker could alter Bloom’s growth outlook within the high-demand data center sector.

We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Bloom Energy Investment Narrative Recap

Bloom Energy’s investment case rests on the belief that its fuel cell technology can address the surging power needs of data centers and industrial clients, capitalizing on grid constraints and demand for resilient, low-carbon energy. The high-profile appointment of Aaron Hoover as head of business and corporate development may support Bloom’s efforts to forge large-scale partnerships, but in the near term, the biggest catalyst, rapid data center deals, remains most influenced by execution of recent contracts, while manufacturing expansion risk continues to cast a shadow. This leadership change is unlikely to substantially alter those drivers or risks in the short run.

Of Bloom's recent announcements, its July partnership to deploy fuel cell systems in Oracle Cloud Infrastructure data centers is most relevant. This aligns directly with the near-term catalyst: converting hyperscaler relationships into recurring revenue while accelerating entry into power-intensive, AI-driven markets.

On the other hand, investors should be aware of how quickly manufacturing expansion plans could pressure margins if demand falls short…

Read the full narrative on Bloom Energy (it's free!)

Bloom Energy's outlook anticipates $2.7 billion in revenue and $395.4 million in earnings by 2028. This is based on 19.0% annual revenue growth and a substantial $371.7 million increase in earnings from the current $23.7 million.

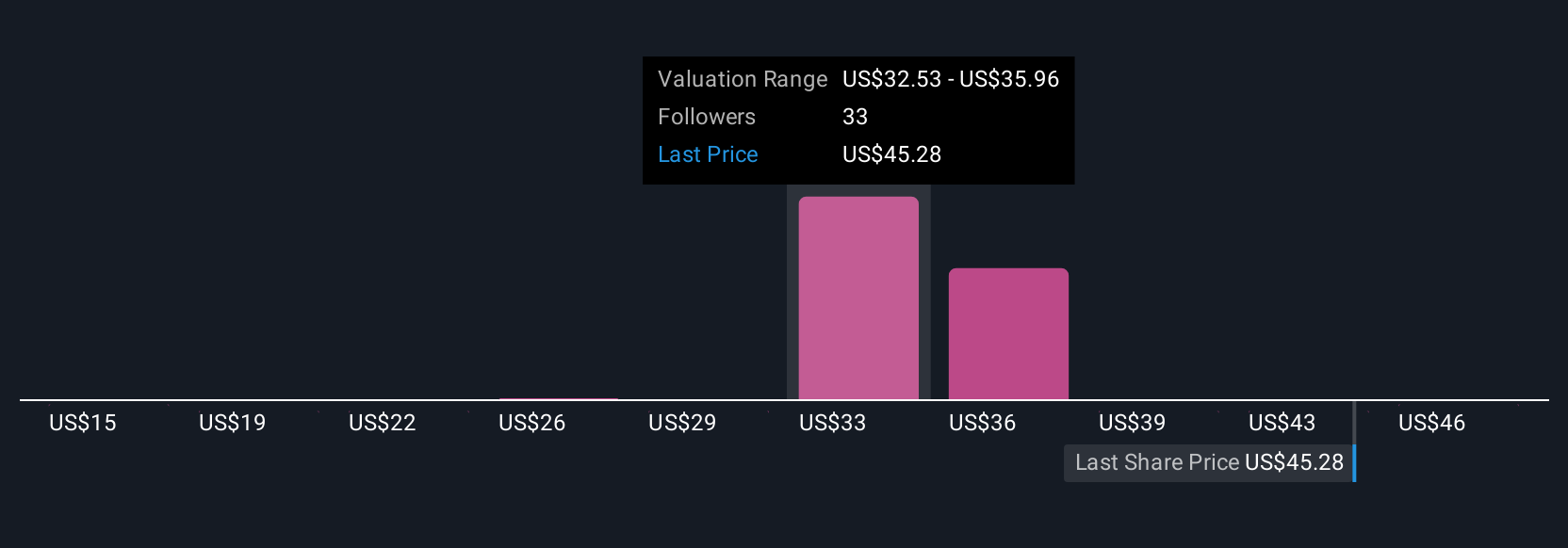

Uncover how Bloom Energy's forecasts yield a $34.57 fair value, a 37% downside to its current price.

Exploring Other Perspectives

Seven members of the Simply Wall St Community estimate Bloom Energy’s fair value between US$15.38 and US$49.68 per share. With such wide-ranging views, it’s important to keep in mind that execution on recent data center partnerships may significantly shape future business strength, reviewing several perspectives can help you understand the breadth of market opinion.

Explore 7 other fair value estimates on Bloom Energy - why the stock might be worth less than half the current price!

Build Your Own Bloom Energy Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Bloom Energy research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Bloom Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bloom Energy's overall financial health at a glance.

Curious About Other Options?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- AI is about to change healthcare. These 27 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 27 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bloom Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BE

Bloom Energy

Designs, manufactures, sells, and installs solid-oxide fuel cell systems for on-site power generation in the United States and internationally.

High growth potential with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|50.7% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|8.5% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|18.4% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|54.2% overvalued

RO

Community Contributor