Advertisement

- United States

- /

- Machinery

- /

- NYSE:AIN

Why Albany International (AIN) Is Down 15.8% After Withdrawing Guidance and Posting a Quarterly Loss

Simply Wall St

Reviewed by Sasha Jovanovic

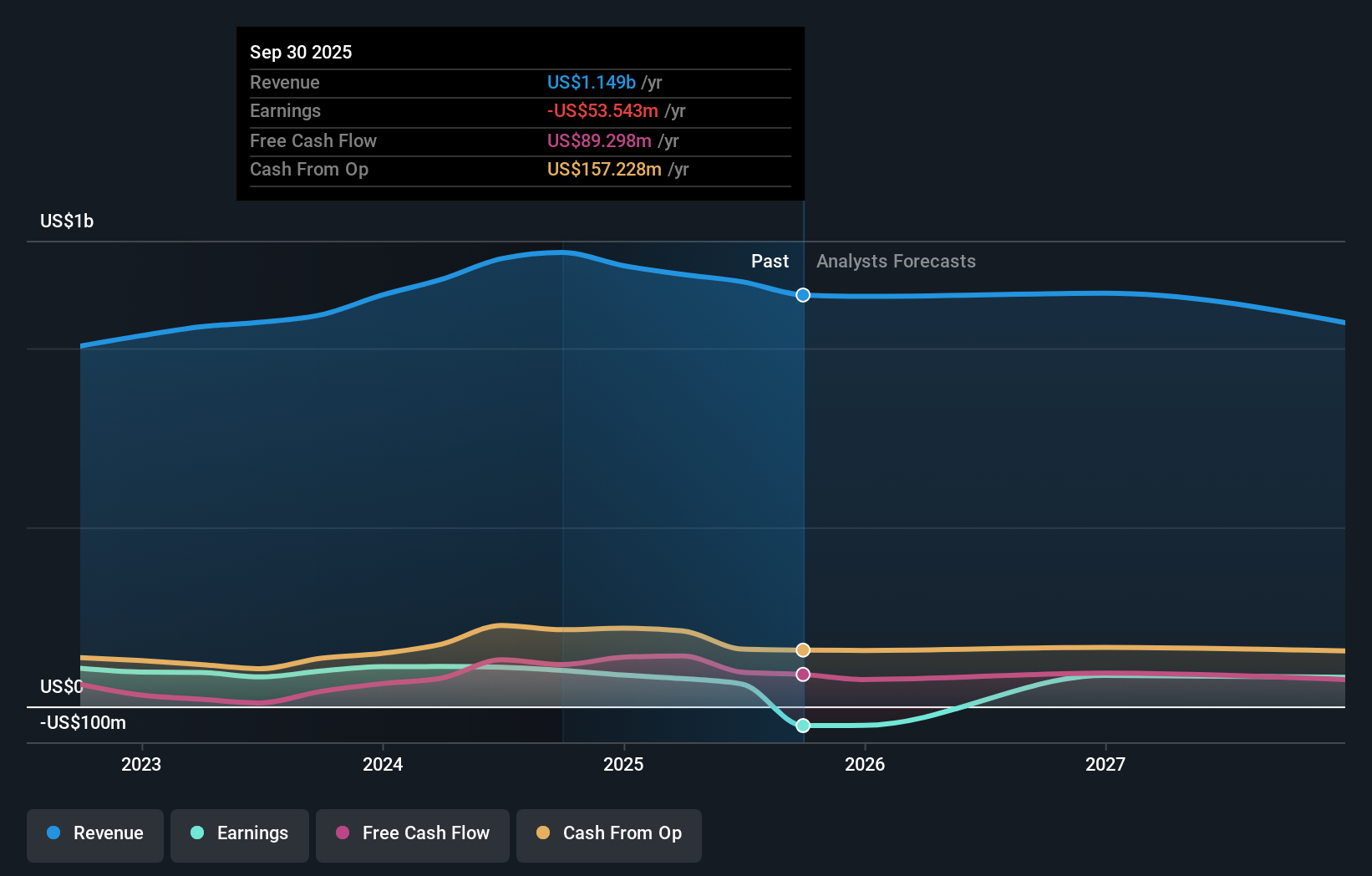

- Albany International reported third-quarter 2025 results showing sales falling to US$261.43 million and posting a net loss of US$97.76 million, a reversal from a net profit a year prior, and withdrew its full-year guidance amid an ongoing strategic review of its Structures business.

- This report follows a substantial share repurchase initiative, with over 2.32 million shares, about 7.7% of outstanding shares, bought back under the program announced earlier in the year.

- We'll examine how the withdrawal of full-year guidance could reshape Albany International's investment outlook and risk profile.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Albany International Investment Narrative Recap

To own shares in Albany International, I believe you have to see ongoing opportunities in advanced composites and eco-friendly fabrics, with confidence that the company can convert its technology edge into sustainable earnings. The withdrawal of full-year guidance following a substantial third-quarter loss directly impacts short-term visibility, raising uncertainty around the timing and scale of any recovery. At the same time, the biggest risk right now remains the company’s high reliance on specific aerospace programs, exposing it to volatility if customer demand or project timelines shift.

Among several recent announcements, the withdrawal of 2025 guidance stands out as most relevant, highlighting how the strategic review of the Structures business could influence forward-looking expectations. Until more clarity is provided, likely with the next results cycle, the unknowns around potential business changes may weigh on investment decision-making and overall risk tolerance. However, the deeper concern for investors to be aware of relates to concentration risk in key aerospace contracts, because if a major customer delays or renegotiates a program...

Read the full narrative on Albany International (it's free!)

Albany International's narrative projects $1.3 billion revenue and $181.1 million earnings by 2028. This requires 4.0% yearly revenue growth and a $118.9 million earnings increase from $62.2 million today.

Uncover how Albany International's forecasts yield a $59.25 fair value, a 29% upside to its current price.

Exploring Other Perspectives

Fair value estimates from the Simply Wall St Community have so far clustered at US$59.25, reflecting one analysis. As many investors weigh future earnings growth against the company’s high exposure to a handful of aerospace clients, your own perspective can add meaningful nuance to the ongoing discussion.

Explore another fair value estimate on Albany International - why the stock might be worth as much as 29% more than the current price!

Build Your Own Albany International Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Albany International research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Albany International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Albany International's overall financial health at a glance.

Contemplating Other Strategies?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've found 14 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:AIN

Albany International

Engages in the machine clothing and engineered composites businesses.

Good value average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor