Advertisement

- United States

- /

- Aerospace & Defense

- /

- NasdaqGS:WWD

What Woodward (WWD)'s Strong Results and $1.8 Billion Buyback Mean for Shareholders

Simply Wall St

Reviewed by Sasha Jovanovic

- In November 2025, Woodward, Inc. announced strong fourth quarter and full-year 2025 results, introduced a new US$1.8 billion share repurchase program, and confirmed it is exploring mergers and acquisitions to further strengthen its business.

- Alongside rising sales and earnings, Woodward highlighted new investments in automation technology and completion of its Spartanburg, South Carolina facility to support future growth.

- Next, we’ll examine how Woodward’s disciplined capital allocation and automation initiatives may impact its outlook and investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

Woodward Investment Narrative Recap

To be a shareholder in Woodward, you need to believe in the company’s ability to leverage automation and disciplined capital allocation in highly technical aerospace and industrial markets. The recent strong earnings and introduction of a US$1.8 billion share repurchase program reinforce Woodward’s focus on returning value, but do not materially offset the key short-term catalyst, which is successful execution of ongoing automation projects, nor the greatest risk, potential pressure on free cash flow from concentrated capital investments.

Among recent announcements, the launch of the new share buyback program is particularly relevant. It demonstrates Woodward's confidence in its financial position and ongoing cash generation, aligning with management’s emphasis on capital discipline and supporting the company’s investment case as it continues pursuing automation and efficiency gains. However, this focus also heightens the potential impact of capital expenditure risk on near-term performance, especially as new manufacturing initiatives ramp up.

By contrast, the pressure that heavy, concentrated capital commitments could place on free cash flow is something investors should be aware of...

Read the full narrative on Woodward (it's free!)

Woodward's narrative projects $4.1 billion in revenue and $561.5 million in earnings by 2028. This requires 6.5% yearly revenue growth and a $173.7 million earnings increase from the current earnings of $387.8 million.

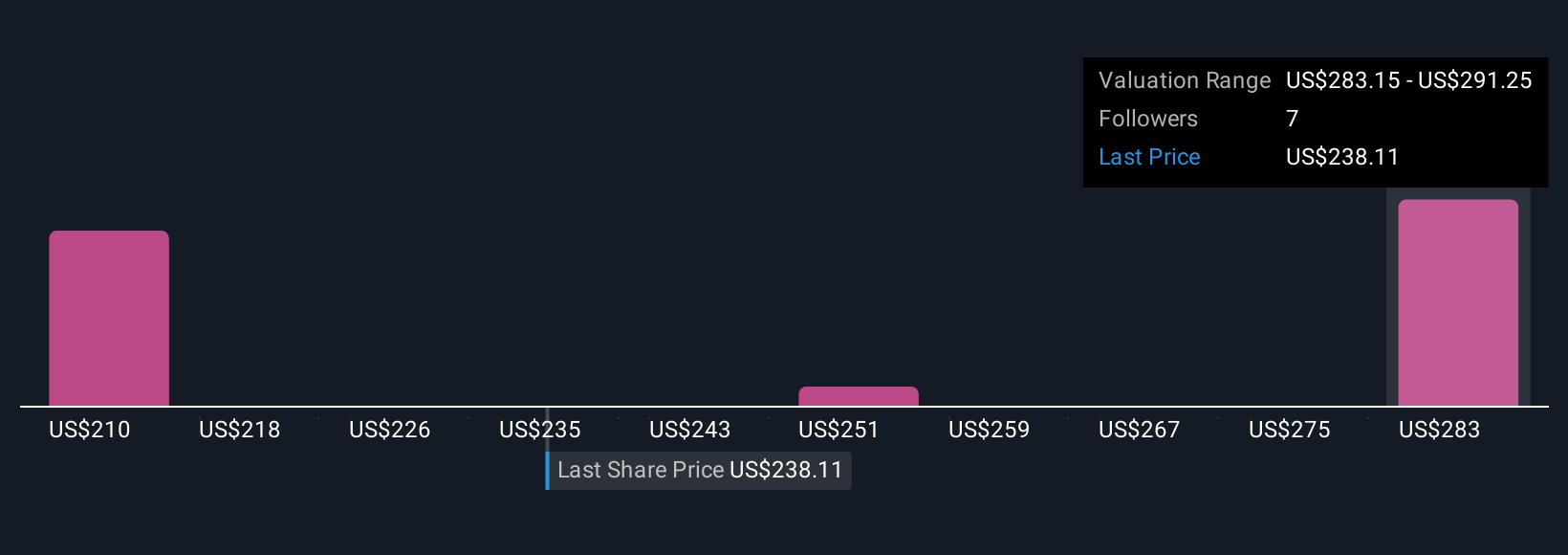

Uncover how Woodward's forecasts yield a $317.12 fair value, a 6% upside to its current price.

Exploring Other Perspectives

Four fair value estimates from the Simply Wall St Community span US$258 to US$317 per share, reflecting wide-ranging expectations for Woodward’s future. Your view may differ, particularly as recent automation investments could materially affect efficiency, growth, and returns over time.

Explore 4 other fair value estimates on Woodward - why the stock might be worth as much as 6% more than the current price!

Build Your Own Woodward Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Woodward research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Woodward research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Woodward's overall financial health at a glance.

Searching For A Fresh Perspective?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Woodward might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:WWD

Woodward

Designs, manufactures, and services control solutions for the aerospace and industrial markets worldwide.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

FA

FAI on Arabian Internet and Communication Services ·

Solutions by stc: 34% Upside in Saudi's Digital Transformation Leader

Fair Value:ر.س342.2335.5% undervalued

10 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

RO

RobertoAllende on NVIDIA ·

The AI Infrastructure Giant Grows Into Its Valuation

Fair Value:US$345.0747.9% undervalued

28 followersusers have followed this narrative

28 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Recently Updated Narratives

TA

Talos on NVIDIA ·

Not a Bubble, But the "Industrial Revolution 4.0" Engine

Fair Value:US$294.9239.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Advanced Micro Devices ·

The "David vs. Goliath" AI Trade – Why Second Place is Worth Billions

Fair Value:US$416.4647.2% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on PayPal Holdings ·

The "Sleeping Giant" Wakes Up – Efficiency & Monetization

Fair Value:US$174.9264.2% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

111 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.1% undervalued

945 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.4% undervalued

146 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative