Advertisement

- United States

- /

- Electrical

- /

- NasdaqGS:VICR

Vicor (VICR) Is Up 5.8% After Securing Sole-Supplier Status For Major Hyperscaler Contract

Simply Wall St

Reviewed by Sasha Jovanovic

- Vicor recently highlighted that it holds over US$1.00 billion of U.S. manufacturing capacity, about US$360 million in cash, and no debt, while revealing it was the only company meeting the requirements for a large hyperscaler contract expected to ramp earlier this year, with two OEM programs following later in the year.

- An additional boost to the outlook comes from Vicor’s high-margin licensing business, where management outlined a clear path to nearly doubling licensing revenue over the next two years alongside margin improvements from better factory utilization.

- We’ll now examine how being the sole qualified supplier for a major hyperscaler contract may reshape Vicor’s existing investment narrative.

These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Vicor Investment Narrative Recap

To own Vicor, you generally need to believe its power solutions can secure durable demand from data center and AI customers, and that its large U.S. manufacturing base can be profitably filled. The recent disclosure that Vicor is the sole qualified supplier for a large hyperscaler puts revenue execution front and center as the key near term catalyst, while lingering order volatility and backlog softness remain the biggest risk if those ramps slip or do not scale as expected.

Among recent developments, Vicor’s update on its high margin licensing business feels most connected to this new contract. Management has laid out a path to nearly doubling licensing revenue over two years, which, when combined with better factory utilization from hyperscaler and OEM ramps, could help offset some of the earnings lumpiness that comes from order swings and litigation related income, giving investors a clearer line of sight on profit quality if demand holds up.

Yet, against this upbeat contract story, investors should also be aware of the risk that...

Read the full narrative on Vicor (it's free!)

Vicor's narrative projects $523.8 million in revenue and $45.4 million in earnings by 2028. This requires 11.4% yearly revenue growth and an earnings decrease of about $20 million from $65.5 million today.

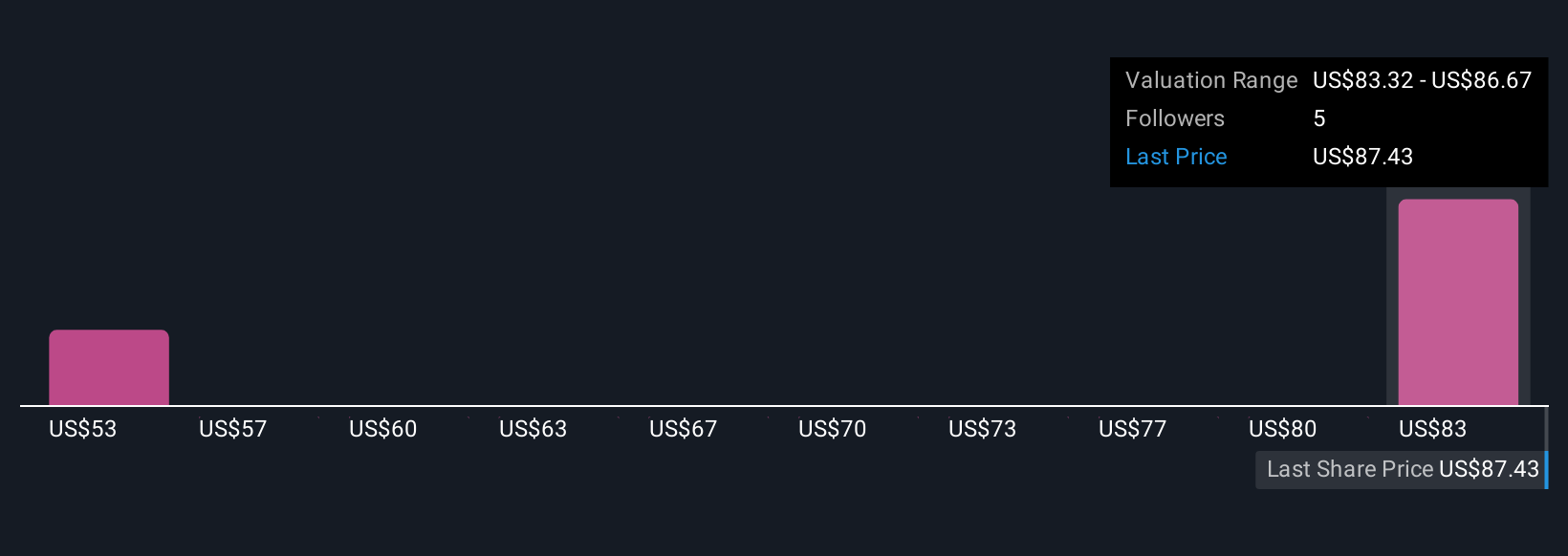

Uncover how Vicor's forecasts yield a $86.67 fair value, a 8% downside to its current price.

Exploring Other Perspectives

Simply Wall St Community members have produced 2 fair value estimates for Vicor, ranging from US$53.39 to US$86.67, underscoring how far opinions can diverge. When you set those views against Vicor’s role as the only qualified supplier on a major hyperscaler program, it becomes even more important to weigh how concentrated demand and order instability might affect future results before settling on your own stance.

Explore 2 other fair value estimates on Vicor - why the stock might be worth as much as $86.67!

Build Your Own Vicor Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Vicor research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Vicor research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vicor's overall financial health at a glance.

Seeking Other Investments?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:VICR

Vicor

Designs, develops, manufactures, and markets modular power components and power systems for converting electrical power for use in electrically-powered devices.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4729.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6410.8% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Alphabet ·

GOOGL: AI Platform Expansion And Cloud Demand Will Support Durable Performance Amid Competitive Pressures

Fair Value:US$323.70.8% undervalued

1342 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative