- United States

- /

- Machinery

- /

- NasdaqGM:SYM

Is It Too Late to Consider Symbotic After Its Huge 2025 Share Price Surge?

Reviewed by Bailey Pemberton

- If you are wondering whether Symbotic is still worth considering after its huge run, or if you are late to the party, this breakdown will help you figure out what the current price is really asking you to believe.

- The stock has climbed about 0.8% over the last week and 7.8% over the last month, but the real eye catchers are its 153.7% year to date and 145.6% 1 year returns, on top of a 408.8% gain over 3 years.

- Recent headlines have focused on Symbotic's expanding automation partnerships and its growing footprint in warehouse robotics, reinforcing the narrative that it is becoming a critical infrastructure player for big box and grocery logistics. These developments help explain why some investors are willing to pay up for potential future growth, even after such a strong share price rally.

- Even so, Symbotic currently scores just 2 out of 6 on our valuation checks. This means most traditional metrics do not flag it as obviously undervalued. Next we will walk through those valuation methods, then finish with a more holistic way to think about what the market might be missing.

Symbotic scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Symbotic Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a company is worth today by projecting its future cash flows and then discounting them back into present dollars. In Symbotic's case, the 2 Stage Free Cash Flow to Equity model starts with last twelve months free cash flow of about $804.5 Million and projects how that cash could grow as warehouse automation demand scales.

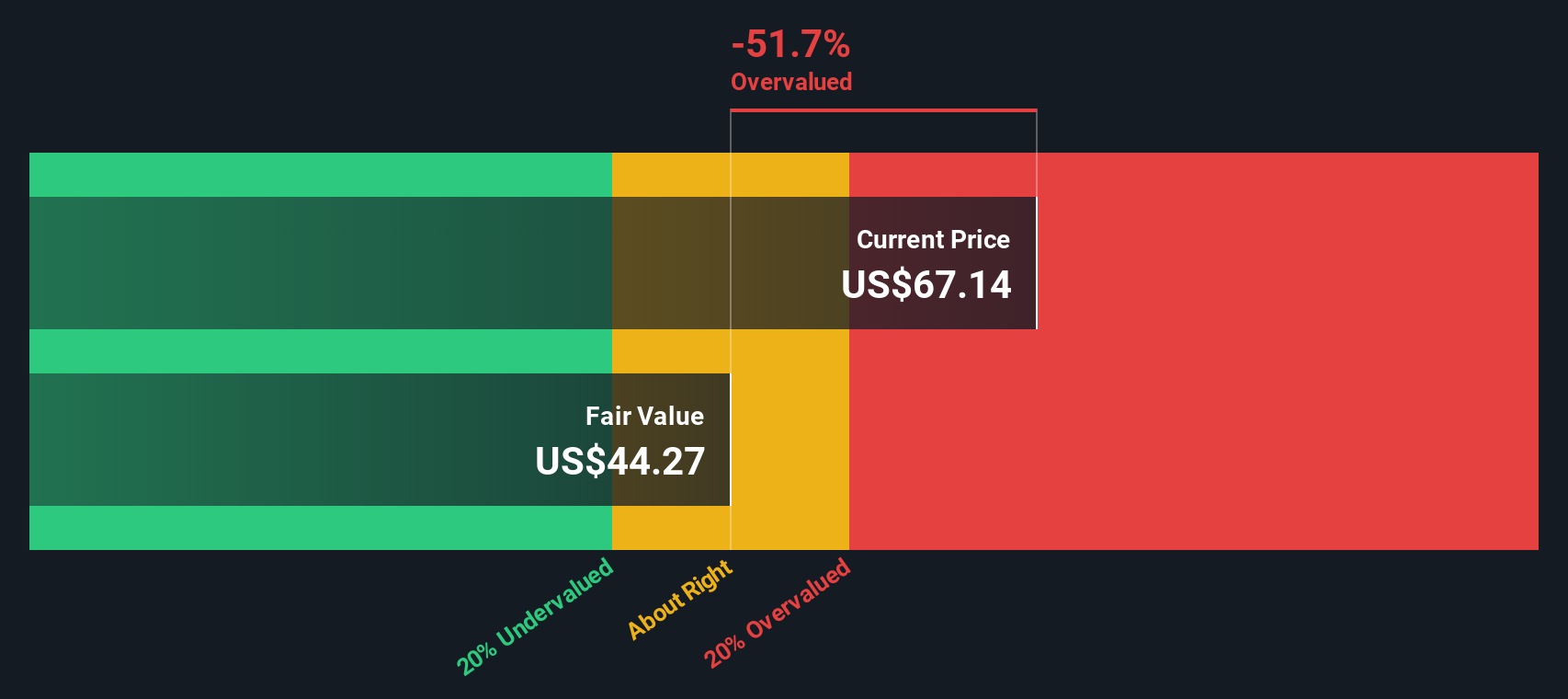

Analysts provide detailed forecasts for the next few years, and Simply Wall St extends these into longer term projections. By 2030, free cash flow is expected to reach roughly $1.76 Billion, with intermediate years stepping up from the hundreds of Millions into the low Billions as the business matures. All of these $ cash flows are discounted back to today to arrive at an estimated intrinsic value of about $46.27 per share.

Compared with the current share price, the DCF implies the stock is around 35.5% overvalued. This suggests the market is already baking in very strong growth and execution.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Symbotic may be overvalued by 35.5%. Discover 914 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Symbotic Price vs Sales

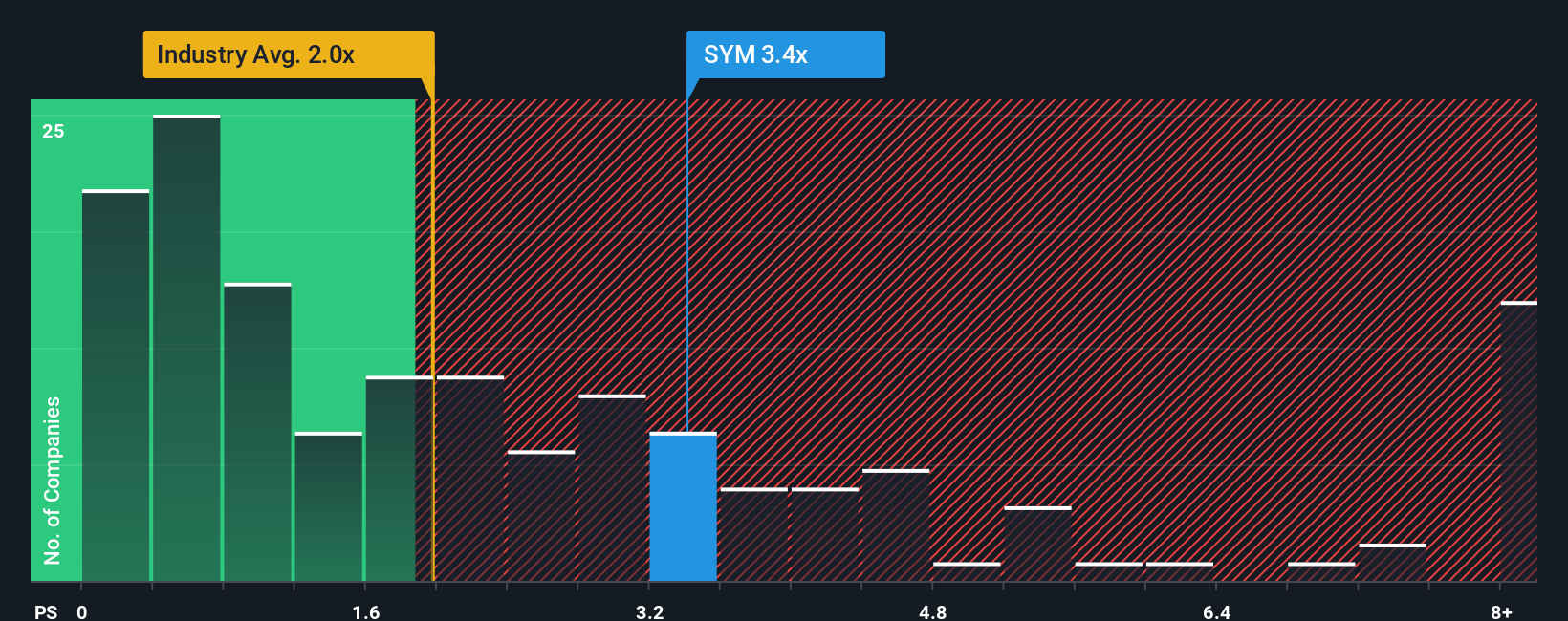

For a business like Symbotic that is investing heavily for scale, the price to sales ratio is a useful yardstick because it focuses on how much investors are paying for each dollar of current revenue, before the noise of near term profitability and accounting items.

In general, higher growth and lower risk justify a richer multiple, while slower or more uncertain growth usually means a lower, more conservative valuation is appropriate. Symbotic currently trades on a price to sales ratio of about 3.36x, which is above the broader Machinery industry average of roughly 2.06x, but slightly below its direct peer group at around 3.45x.

Simply Wall St also calculates a proprietary Fair Ratio of 4.24x. This reflects what would be reasonable for Symbotic given its specific growth outlook, margins, industry, market cap and risk profile. This is more tailored than a simple comparison with peers or industry averages, which can miss company specific strengths or weaknesses. With the Fair Ratio sitting meaningfully above the current 3.36x, this multiple based view points to Symbotic being undervalued relative to its fundamentals and growth potential.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1461 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Symbotic Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, a simple way to connect your view of Symbotic’s story with the numbers behind its future.

A Narrative is your own story for a company, where you spell out what you believe about its growth, margins and risks, and then translate that into a financial forecast and a fair value estimate instead of just staring at raw ratios.

On Simply Wall St, Narratives live in the Community page and are used by millions of investors as an easy, guided tool that links a company’s business story to revenue, earnings and margin assumptions, and then to a clear Fair Value you can compare against today’s share price.

Because Narratives on the platform update dynamically when new information such as earnings, guidance or news arrives, your Symbotic view automatically evolves with the facts. For example, a very bullish investor might see upside to around $62 per share, while a more cautious investor could anchor closer to $10, each with a transparent story explaining why.

Do you think there's more to the story for Symbotic? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:SYM

Symbotic

An automation technology company, develops technologies to enhance operating efficiencies in modern warehouses.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion