Advertisement

- United States

- /

- Electrical

- /

- NasdaqGS:POWL

Powell Industries (POWL) Is Up 9.8% After Upward Earnings Revisions and Strong Analyst Endorsement

Simply Wall St

Reviewed by Sasha Jovanovic

- Earlier this week, Powell Industries drew new investor interest following upward revisions to earnings estimates and a strong analyst rating, highlighting expectations of continued revenue growth for the current and next fiscal years despite a prior quarter revenue miss.

- An intriguing element is Powell’s repeated outperformance of earnings per share estimates, which signals underlying operational momentum even as consensus remains optimistic.

- We'll now explore how ongoing analyst optimism about Powell's positive earnings trends could influence the company's future investment narrative.

Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

Powell Industries Investment Narrative Recap

To be a shareholder in Powell Industries right now, you need confidence in the company's ability to maintain robust order momentum and revenue visibility, fueled by secular electrification and infrastructure demand, while balancing expectations for continued margin strength. This week's earnings estimate upgrades and positive analyst sentiment reinforce that operational momentum remains a near-term catalyst, but the most meaningful risk is that current gross margin levels, lifted by one-time project closeouts, may not persist going forward; the latest news does not substantially diminish these risks or catalysts.

Among Powell’s recent developments, the $12.4 million capacity expansion at its Jacintoport facility, announced in August, underscores the company’s commitment to supporting organic growth and capturing new business across oil and gas, utilities, and other key end markets. This investment aligns with the optimism around backlog conversion and market tailwinds, yet it also highlights how management is positioning the business for evolving demand cycles that may shift the near-term order mix and margin profile.

However, investors should also keep in mind the possibility, in contrast to upbeat headlines, that future project margins could revert closer to historic norms as ...

Read the full narrative on Powell Industries (it's free!)

Powell Industries' outlook anticipates $1.3 billion in revenue and $169.4 million in earnings by 2028. This scenario is based on a 5.7% annual revenue growth rate but implies a decrease in earnings of $6 million from the current $175.4 million.

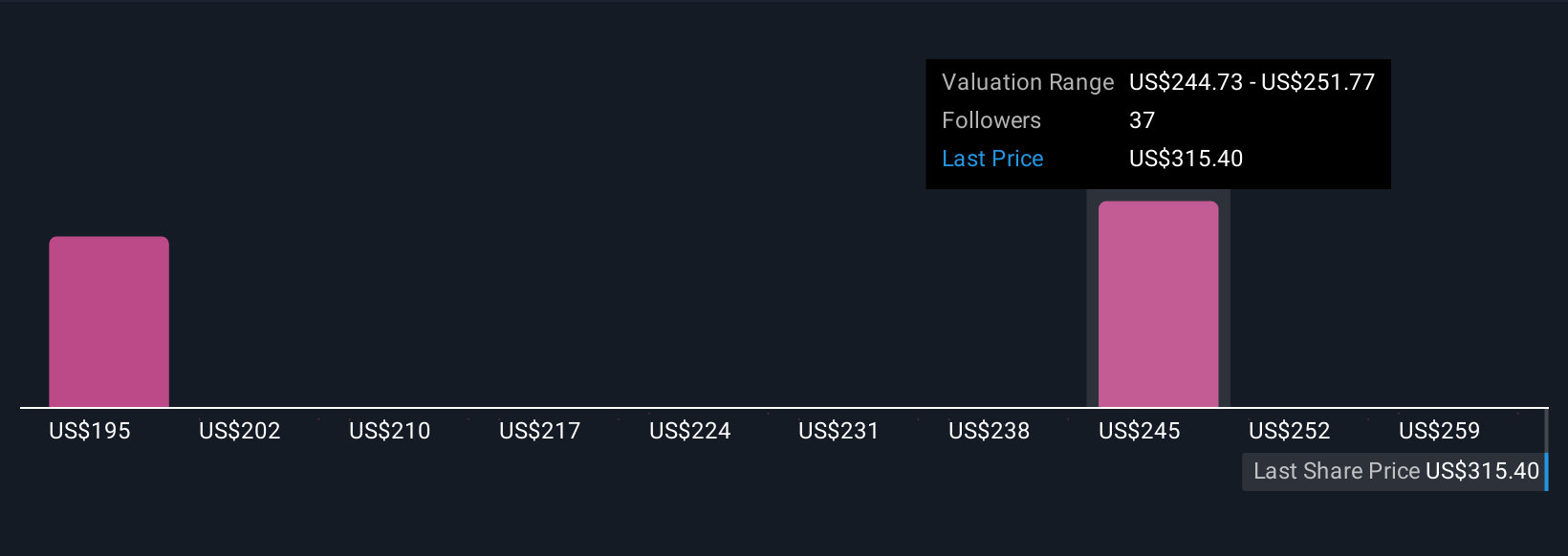

Uncover how Powell Industries' forecasts yield a $269.26 fair value, a 23% downside to its current price.

Exploring Other Perspectives

Four members of the Simply Wall St Community estimate Powell’s fair value per share between US$192.13 and US$269.26. While some see upside, many analysts caution these views must be weighed against the risk that recent margin gains might not be sustained in future quarters.

Explore 4 other fair value estimates on Powell Industries - why the stock might be worth 45% less than the current price!

Build Your Own Powell Industries Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Powell Industries research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Powell Industries research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Powell Industries' overall financial health at a glance.

Curious About Other Options?

Our top stock finds are flying under the radar-for now. Get in early:

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 37 companies in the world exploring or producing it. Find the list for free.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:POWL

Powell Industries

Designs, develops, manufactures, sells, and services custom-engineered equipment and systems.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|7.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|93.3% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.4% undervalued

GM

Community Contributor